PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1915210

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1915210

Fleet Telematics Market by Vehicle Type (LCV, HCV), Package Type (Entry Level, Mid Tier, Advanced), Vendor Type (OEMs, Aftermarket), Solution Type (Embedded, Portable, Smartphone/Cellular), and Region - Global Forecast to 2032

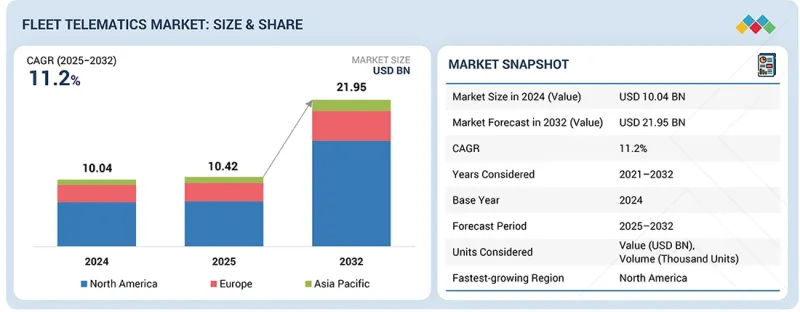

The fleet telematics market is projected to grow from USD 10.42 billion in 2025 to USD 21.95 billion by 2032 at a CAGR of 11.2%. The adoption of telematics packages for commercial vehicles is moving steadily toward advanced tiers as fleets seek deeper operational intelligence, including real-time component health insights, load cycle analytics, multi-asset visibility, and automated compliance workflows. Smartphone/cellular telematics continues to gain a significant share among small and subcontracted fleets due to its zero installation model.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Package type, Solution Type, Vehicle Type, Vendor Type (OEMS, Aftermarket) |

| Regions covered | Asia Pacific, Europe, and North America |

At the same time, portable devices remain essential for rental, leasing, and vocational segments where assets regularly shift between operators. Adoption patterns are also diverging by vehicle class. For example, LCV fleets are prioritizing delivery performance, trip level utilization, and workflow digitization, whereas HCV fleets demand stress cycle monitoring, maintenance interval optimization, and cargo condition visibility.

"The aftermarket segment is projected to dominate the fleet telematics market during the forecast period."

By vendor type, the aftermarket segment is projected to lead the fleet telematics market, as most fleets operate vehicles of different ages, brands, and configurations, and aftermarket systems can connect all of them through retrofit devices or OEM data integrations. Unlike OEM portals tied to specific brands, aftermarket platforms offer broader compatibility, stronger analytics, richer reporting, and frequent over-the-air feature updates. They also give fleets a single, standardized interface, reducing the need to manage multiple OEM systems. In many regions, including India and other emerging markets, OEM-installed telematics adoption in the existing vehicle base is still low, making aftermarket solutions the only practical way to digitize older or legacy vehicles. Interoperability challenges and fragmented OEM standards further propel the demand for aftermarket aggregators that can combine data from different vehicle platforms into one dashboard.

Aftermarket leaders are rapidly integrating OEM-embedded data. For instance, Geotab integrates OEM telematics data from a wide range of vehicle manufacturers, including Ford, General Motors (OnStar), Mercedes-Benz, Volvo Cars, Stellantis brands, BMW Group, Renault, and the Volkswagen Group, enabling fleets to consolidate factory-installed and retrofit telematics data on a single platform for unified management.

"The advanced segment is projected to grow at the highest rate during the forecast period."

By package type, the advanced segment is projected to grow at the highest rate in the fleet telematics market during the forecast period. These telematics deliver high-value capabilities, such as remote diagnostics, predictive maintenance, crash detection, compliance monitoring, and real-time video and event analytics, all of which help fleets reduce costs and improve operational performance. Rising safety, fuel, and regulatory demands are pushing operators to adopt systems that enable driver coaching, proactive maintenance workflows, and continuous compliance management. As fleets transition toward software-defined and data-centric operations, they require uninterrupted, high-quality data streams that advanced solutions are built to provide. Increasing operational complexity across mixed and high utilization fleets further accelerates the demand for platforms that consolidate diagnostics, sensor data, driver behavior insights, and maintenance information into a single management view. As a result, many players are undertaking strategies to capture this demand. For example, Samsara's 2025 AI Safety Suite demonstrated crash rate reductions of nearly 75% using automated video analysis and real-time driver coaching. Likewise, Daimler Truck's global Truck Data Center (TDC) enabled factory-level remote diagnostics and OTA updates as standard on new models. Similarly, ZF's TX-CONNECT platform integrated predictive maintenance and advanced sensor data across trucks and trailers. Many other players are undertaking similar developments for long-term advantages, such as low operating costs, strong safety performance, reduced downtime, and better regulatory alignment.

"Asia Pacific is projected to grow at a significant rate during the forecast period."

Asia Pacific is projected to be the fastest-growing regional market during the forecast period. The growth of the region can be attributed to China's advanced connectivity infrastructure, strong 4G/5G penetration, and nationwide digital transport systems. Government mandates for safety, hazardous goods tracking, and Beidou-based positioning continue to drive the adoption of telematics across trucks, buses, and LCVs, while leading logistics operators, such as JD Logistics, SF Express, and Alibaba Cainiao, depend on advanced routing, cold chain, and real-time freight-visibility tools. Rapid expansion of autonomous driving pilots, ADAS integration, and OEM-connected platforms is pushing the demand for higher-value telematics packages.

Chinese OEMs, including Foton, Dongfeng, SAIC, and BYD, are standardizing embedded connectivity in new commercial vehicles, accelerating market penetration. In September 2025, the Chinese government announced that China had established a complete industrial chain system for key intelligent connected vehicle technologies, covering smart cockpits, autonomous driving, cloud connectivity, and vehicle control. China's long-term auto roadmap targets over 80% penetration of new energy and connected vehicles by 2040. It expects to reinforce continued growth for connected and telematics-enabled commercial fleets.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 32%, Tier 1 - 48%, and Tier 2 - 20%

- By Designation: CXOs - 31%, Managers - 53%, and Executives - 16%

- By Region: North America - 43%, Asia Pacific - 24%, Europe - 33%

The fleet telematics market is dominated by major players, such as Geotab Inc. (Canada), Verizon (US), Trimble Inc. (US), Samsara Inc. (US), and Powerfleet (US). These companies have adopted a mix of organic and inorganic growth strategies, such as product launches, strategic partnerships, joint ventures, mergers & acquisitions, and expansion of production facilities, to strengthen their international footprint and capture a larger market share. Through these strategies, they have expanded across regions by offering differentiated telematics portfolios tailored to specific fleet segments, including advanced safety and compliance modules, multi-asset visibility solutions, industry-specific workflows, and integrated platforms that connect vehicles, trailers, and operational systems into a unified ecosystem.

Research Coverage

This research report categorizes the fleet telematics market by Vehicle Type (Light Commercial Vehicle, Heavy Commercial Vehicle), Package Type (Entry Level, Mid Tier, Advanced), Vendor Type (OEMs, Aftermarket), Solution Type (Embedded, Portable, Smartphone/Cellular), and Region. It covers the competitive landscape and profiles of the major players of the fleet telematics market. Further, the study includes an in-depth competitive analysis of the key market players, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall fleet telematics market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (Increasing demand for intelligent fleet operations; focus on fuel efficiency and reducing vehicle downtime, technology-driven transformation in fleet management) restraints (Connectivity limitations in remote areas and developing markets, integration complexity with legacy fleet systems and multi-brand vehicles), opportunities (Convergence of V2X communication and autonomous mobility; digital transformation through AI and smart infrastructure, expanding opportunities in logistics and transportation, cross-platform integration and API-driven ecosystems), and challenges (Escalating cost of ownership (TCO), challenges in user adoption, lack of standardization)

- Product Development/Innovation: Detailed insights into upcoming technologies and research & development activities in the fleet telematics market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the fleet telematics market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players, such as Geotab Inc. (Canada), Verizon (US), Trimble Inc. (US), Samsara Inc. (US), and Powerfleet (US), in the fleet telematics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING FLEET TELEMATICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLEET TELEMATICS MARKET

- 3.2 FLEET TELEMATICS MARKET, BY VENDOR TYPE

- 3.3 FLEET TELEMATICS MARKET, BY VEHICLE TYPE

- 3.4 FLEET TELEMATICS MARKET, BY PACKAGE TYPE

- 3.5 FLEET TELEMATICS MARKET, BY SOLUTION TYPE

- 3.6 FLEET TELEMATICS MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for intelligent fleet operations

- 4.2.1.2 Focus on fuel efficiency and reducing vehicle downtime

- 4.2.1.3 Technology-driven transformation in fleet management

- 4.2.1.4 Need for strengthening compliance and safety standards

- 4.2.2 RESTRAINTS

- 4.2.2.1 Connectivity limitations in remote areas and developing markets

- 4.2.2.2 Integration complexity with legacy fleet systems and multi-brand vehicles

- 4.2.2.3 Data security and user trust issues

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Convergence of V2X communication and autonomous mobility

- 4.2.3.2 Digital transformation through AI and smart infrastructure

- 4.2.3.3 Expanding opportunities in logistics and transportation

- 4.2.3.4 Cross-platform integration and API-driven ecosystems

- 4.2.4 CHALLENGES

- 4.2.4.1 Escalating TCO (total cost of ownership)

- 4.2.4.2 User adoption challenges

- 4.2.4.3 Lack of standardization

- 4.2.5 IMPACT OF MARKET DYNAMICS ON FLEET TELEMATICS MARKET

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN FLEET TELEMATICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/-2/-3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/-2/-3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMICS INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL COMMERCIAL VEHICLE INDUSTRY

- 5.1.4 TRENDS IN GLOBAL FLEET INDUSTRY

- 5.2 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3 PRICING ANALYSIS

- 5.3.1 AVERAGE SELLING PRICE OF FLEET TELEMATICS PACKAGE TYPES, BY KEY PLAYER

- 5.3.2 AVERAGE SELLING PRICE TREND OF FLEET TELEMATICS, BY PACKAGE TYPE

- 5.3.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 UNLOCKING FLEET ELECTRIFICATION POTENTIAL THROUGH DATA-DRIVEN EV SUITABILITY ANALYSIS

- 5.6.2 SCHLUMBERGER ADOPTED POWERFLEET'S MIX TO IMPROVE OPERATIONAL EFFICIENCY

- 5.6.3 OMV PETROM IMPLEMENTED POWERFLEET'S MIX TO IMPROVE FLEET EFFICIENCY AND PRODUCTIVITY

- 5.6.4 ATWELL ADOPTED GEOTAB'S FLEET MANAGEMENT PLATFORM TO ENHANCE FLEET SAFETY AND IMPROVE VEHICLE UTILIZATION

- 5.7 INVESTMENT & FUNDING SCENARIO

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO

- 5.8.2 EXPORT SCENARIO

- 5.9 KEY CONFERENCES & EVENTS, 2026-2027

- 5.10 DECISION-MAKING PROCESS

- 5.11 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 BUYING CRITERIA

- 5.12 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 5.13 MARKET PROFITABILITY

- 5.13.1 REVENUE POTENTIAL

- 5.13.2 COST DYNAMICS

- 5.13.3 MARGIN OPPORTUNITIES, BY APPLICATION

- 5.14 REGULATORY LANDSCAPE AND COMPLIANCE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 INDUSTRY STANDARDS

- 5.15 SUSTAINABILITY INITIATIVES

- 5.15.1 TRANSITION TOWARD ELECTRIFIED AND HYBRID FLEETS

- 5.15.2 REAL-TIME EMISSION AND ENERGY MONITORING

- 5.15.3 INTEGRATION WITH GREEN LOGISTICS AND SMART CITY SYSTEMS

- 5.15.4 FUEL EFFICIENCY OPTIMIZATION THROUGH DATA-DRIVEN INSIGHTS

- 5.16 PATENT ANALYSIS

- 5.17 IMPACT OF GENERATIVE AI ON FLEET TELEMATICS MARKET

- 5.17.1 PREDICTIVE AND GENERATIVE MAINTENANCE MODELING

- 5.17.2 INTELLIGENT ROUTE AND BEHAVIOR OPTIMIZATION

- 5.17.3 AUTOMATED FLEET INSIGHTS AND REPORTING

- 5.17.4 DIGITAL TWIN AND SIMULATION CAPABILITIES

- 5.18 KEY EMERGING TECHNOLOGIES

- 5.18.1 EDGE COMPUTING

- 5.18.2 5G CONNECTIVITY

- 5.18.3 DIGITAL TWINS

- 5.18.4 AI-DRIVEN VIDEO TELEMATICS

- 5.18.5 BIG DATA ANALYTICS

- 5.19 COMPLEMENTARY TECHNOLOGIES

- 5.19.1 V2X COMMUNICATION (VEHICLE-TO-EVERYTHING)

- 5.19.2 CLOUD COMPUTING PLATFORMS

- 5.19.3 AR/VR INTERFACES FOR FLEET TRAINING

- 5.19.4 SMART CITY INFRASTRUCTURE INTEGRATION

- 5.19.5 BIOMETRIC VEHICLE ACCESS SYSTEM

- 5.20 TECHNOLOGY/PRODUCT ROADMAP

- 5.20.1 SHORT TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 5.20.2 MID TERM (2028-2030) | EXPANSION & STANDARDIZATION

- 5.20.3 LONG TERM (2031-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 5.21 IMPACT OF VEHICLE TELEMATICS ON COST SAVINGS OF KEY PLAYERS

- 5.21.1 COST SAVING ANALYSIS FOR KEY PLAYERS

- 5.21.1.1 Webfleet

- 5.21.1.2 Geotab Inc.

- 5.21.2 COST ANALYSIS OF FLEET TELEMATICS SOLUTIONS

- 5.21.1 COST SAVING ANALYSIS FOR KEY PLAYERS

- 5.22 INSIGHTS INTO FLEET TELEMATICS DATA PLANS, BY OEM

- 5.23 INSIGHTS INTO COMMERCIAL VEHICLE TELEMATICS ARCHITECTURE

- 5.23.1 SHIFT FROM HARDWARE-CENTRIC TO SOFTWARE-DEFINED ARCHITECTURE

- 5.23.2 LAYERED AND MODULAR SYSTEM DESIGN

- 5.23.3 EDGE-CLOUD COLLABORATION FOR DATA PROCESSING

- 5.23.4 INTEGRATION WITH VEHICLE DOMAIN CONTROLLERS AND ADAS SYSTEMS

- 5.23.5 CYBERSECURITY AND FUNCTIONAL SAFETY EMBEDDED BY DESIGN

- 5.24 FLEET TELEMATICS MARKET ECOSYSTEM: FUTURE APPLICATIONS

- 5.24.1 AUTONOMOUS FLEET OPERATIONS AND REMOTE DRIVING

- 5.24.2 PREDICTIVE AND GENERATIVE MAINTENANCE PLATFORMS

- 5.24.3 DYNAMIC INSURANCE AND USAGE-BASED BUSINESS MODELS

- 5.24.4 INTEGRATED SMART LOGISTICS AND SUPPLY CHAIN NETWORKS

- 5.24.5 GREEN FLEET MANAGEMENT AND CARBON INTELLIGENCE

6 FLEET TELEMATICS MARKET, BY PACKAGE TYPE

- 6.1 INTRODUCTION

- 6.2 ENTRY LEVEL

- 6.2.1 INCREASING ADOPTION OF TELEMATICS BY SMALL AND MEDIUM-SIZED FLEETS TO PROPEL GROWTH

- 6.3 MID TIER

- 6.3.1 RISING DEMAND FOR ADVANCED ANALYTICS, PREDICTIVE MAINTENANCE, AND ABILITY TO EXPAND FLEETS TO BOOST MARKET

- 6.4 ADVANCED

- 6.4.1 NEED FOR CUSTOMIZABLE SOLUTIONS FOR COMPLEX FLEET MANAGEMENT CHALLENGES TO FUEL SEGMENT GROWTH

- 6.5 KEY PRIMARY INSIGHTS

7 FLEET TELEMATICS MARKET, BY SOLUTION TYPE

- 7.1 INTRODUCTION

- 7.2 EMBEDDED

- 7.2.1 NEED FOR INTEGRATION OF ADVANCED FEATURES OF EMBEDDED SYSTEMS WITH DEEP VEHICLE INSIGHTS TO FUEL GROWTH

- 7.3 PORTABLE 125 7.3.1 EASE OF TRANSFER BETWEEN VEHICLES AND LOW UPFRONT COSTS TO DRIVE DEMAND FOR PORTABLE TELEMATICS SOLUTIONS

- 7.4 SMARTPHONE/CELLULAR

- 7.4.1 SMARTPHONES/CELLULAR NETWORKS PROVIDE ADVANCED MANAGEMENT FEATURES TO FLEET TELEMATICS

- 7.5 KEY PRIMARY INSIGHTS

8 FLEET TELEMATICS MARKET, BY VEHICLE TYPE

- 8.1 INTRODUCTION

- 8.2 LIGHT COMMERCIAL VEHICLE

- 8.2.1 SURGE IN E-COMMERCE AND FOCUS ON ROUTE OPTIMIZATION TO FUEL SEGMENT GROWTH

- 8.3 HEAVY COMMERCIAL VEHICLE

- 8.3.1 DEMAND FOR EFFECTIVE FUEL MANAGEMENT SYSTEM AND REAL-TIME DRIVER MONITORING TO DRIVE MARKET

- 8.4 KEY PRIMARY INSIGHTS

9 FLEET TELEMATICS MARKET, BY VENDOR TYPE

- 9.1 INTRODUCTION

- 9.2 OEMS

- 9.2.1 NEED FOR TIGHT INTEGRATION AND PER-VEHICLE SPECIALIZATION TO FUEL GROWTH

- 9.3 AFTERMARKET

- 9.3.1 GROWING DEMAND FOR CUSTOMIZABLE AND SCALABLE TELEMATICS SOLUTIONS TO DRIVE GROWTH

- 9.4 KEY PRIMARY INSIGHTS

10 FLEET TELEMATICS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 Technological advancements in AI-powered fleet management solutions to propel growth

- 10.2.2 CANADA

- 10.2.2.1 Rising demand for efficient fuel management prompts businesses to invest in telematics

- 10.2.1 US

- 10.3 ASIA PACIFIC

- 10.3.1 CHINA

- 10.3.1.1 Presence of vast commercial fleets to drive market

- 10.3.2 INDIA

- 10.3.2.1 Rising e-commerce sector to boost growth

- 10.3.3 JAPAN

- 10.3.3.1 Focus on technological innovations in automotive sector to boost market

- 10.3.4 SOUTH KOREA

- 10.3.4.1 Emphasis on improving fuel economy and operational efficiency to spur growth

- 10.3.1 CHINA

- 10.4 EUROPE

- 10.4.1 FRANCE

- 10.4.1.1 Surge in adoption of vehicle-tracking and fuel management systems to drive market growth

- 10.4.2 GERMANY

- 10.4.2.1 Presence of leading OEMs to drive market

- 10.4.3 ITALY

- 10.4.3.1 Demand for cost-optimized fleet and fuel management solutions to boost adoption of telematics solutions

- 10.4.4 SPAIN

- 10.4.4.1 Growing focus on driver-behavior monitoring and route optimization to drive market

- 10.4.5 UK

- 10.4.5.1 Need for integration of telematics with new technologies and efficient fuel management solutions to propel growth

- 10.4.1 FRANCE

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 11.3 MARKET SHARE ANALYSIS, 2025

- 11.4 REVENUE ANALYSIS OF TOP FIVE LISTED/PUBLIC PLAYERS

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.5.1 COMPANY VALUATION

- 11.5.2 FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Solution type footprint

- 11.7.5.4 Vehicle type footprint

- 11.7.5.5 Vendor type footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 11.8.5.1 Detailed list of startups/SMEs

- 11.8.5.2 Competitive benchmarking of startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES & DEVELOPMENTS

- 11.9.2 DEALS

- 11.9.3 EXPANSION

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 GEOTAB INC.

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches & developments

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 VERIZON

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches & developments

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 TRIMBLE INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches & developments

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 SAMSARA INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches & developments

- 12.1.4.3.2 Deals

- 12.1.4.3.3 Expansion

- 12.1.4.3.4 Other developments

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses & competitive threats

- 12.1.5 POWERFLEET

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches & developments

- 12.1.5.3.2 Deals

- 12.1.5.3.3 Expansion

- 12.1.5.3.4 Other developments

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses & competitive threats

- 12.1.6 TELETRAC NAVMAN US LTD

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches & developments

- 12.1.6.3.2 Deals

- 12.1.6.3.3 Other developments

- 12.1.7 MASTERNAUT LIMITED

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches & developments

- 12.1.7.3.2 Deals

- 12.1.8 TOMTOM INTERNATIONAL BV

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches & developments

- 12.1.8.3.2 Deals

- 12.1.9 OMNITRACS

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches & developments

- 12.1.9.3.2 Deals

- 12.1.9.3.3 Other developments

- 12.1.10 MICROLISE LIMITED

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches & developments

- 12.1.10.3.2 Deals

- 12.1.11 PTC

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches & developments

- 12.1.11.3.2 Deals

- 12.1.12 AZUGA, A BRIDGESTONE COMPANY

- 12.1.12.1 Business overview

- 12.1.12.2 Products/Solutions/Services offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Product launches & developments

- 12.1.1 GEOTAB INC.

- 12.2 OTHER PLAYERS

- 12.2.1 OCTO GROUP SPA

- 12.2.2 ZONAR SYSTEMS, INC.

- 12.2.3 SPIREON

- 12.2.4 LYTX, INC.

- 12.2.5 MOTIVE TECHNOLOGIES, INC.

- 12.2.6 VOLKSWAGEN GROUP

- 12.2.7 MAHINDRA&MAHINDRA LTD.

- 12.2.8 SUN-TECH INTERNATIONAL GROUP LIMITED

- 12.2.9 CALAMP

- 12.2.10 RAM TRACKING

- 12.2.11 LINXUP

- 12.2.12 ITRIANGLE

- 12.2.13 NOREGON

13 RESEARCH METHODOLOGY

- 13.1 RESEARCH DATA

- 13.1.1 SECONDARY DATA

- 13.1.1.1 List of key secondary sources

- 13.1.1.2 Key data from secondary sources

- 13.1.2 PRIMARY DATA

- 13.1.2.1 Primary interview participants

- 13.1.2.2 Key industry insights and breakdown of primary interviews

- 13.1.2.3 List of primary interviewees

- 13.1.1 SECONDARY DATA

- 13.2 MARKET SIZE ESTIMATION

- 13.2.1 BOTTOM-UP APPROACH

- 13.2.2 TOP-DOWN APPROACH

- 13.3 DATA TRIANGULATION

- 13.4 FACTOR ANALYSIS

- 13.4.1 DEMAND- AND SUPPLY-SIDE FACTOR ANALYSIS

- 13.5 RESEARCH ASSUMPTIONS

- 13.6 RESEARCH LIMITATIONS

- 13.7 RISK ASSESSMENT

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.3.1 FLEET TELEMATICS MARKET, BY VEHICLE TYPE, AT COUNTRY LEVEL

- 14.3.2 FLEET TELEMATICS MARKET, BY SOLUTION TYPE, AT COUNTRY LEVEL

- 14.3.3 COMPANY INFORMATION

- 14.3.3.1 Profiling of additional market players (up to 5)

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS

List of Tables

- TABLE 1 FLEET TELEMATICS MARKET DEFINITION, BY PACKAGE TYPE

- TABLE 2 FLEET TELEMATICS MARKET DEFINITION, BY SOLUTION TYPE

- TABLE 3 FLEET TELEMATICS MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 4 FLEET TELEMATICS MARKET DEFINITION, BY VENDOR TYPE

- TABLE 5 USD EXCHANGE RATES, 2019-2024

- TABLE 6 KEY REGULATIONS AND COMPLIANCE RULES, BY COUNTRY/REGION

- TABLE 7 IMPACT OF MARKET DYNAMICS ON FLEET TELEMATICS MARKET

- TABLE 8 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 9 AVERAGE SELLING PRICE OF FLEET TELEMATICS PACKAGE TYPES, BY KEY PLAYER, 2025 (USD PER MONTH)

- TABLE 10 AVERAGE SELLING PRICE TREND OF FLEET TELEMATICS, BY PACKAGE TYPE, 2023-2025 (USD PER YEAR)

- TABLE 11 ENTRY LEVEL: AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD PER YEAR)

- TABLE 12 MID TIER: AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD PER YEAR)

- TABLE 13 ADVANCED: AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD PER YEAR)

- TABLE 14 ROLE OF COMPANIES IN MARKET ECOSYSTEM

- TABLE 15 IMPORT DATA FOR HS CODE 8526-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 16 EXPORT DATA FOR HS CODE 8526-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 17 KEY CONFERENCES & EVENTS, 2026-2027

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE

- TABLE 19 KEY BUYING CRITERIA, BY PACKAGE TYPE

- TABLE 20 MARGIN OPPORTUNITIES, BY APPLICATION

- TABLE 21 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 24 REGULATIONS MANDATING TELEMATICS SERVICES

- TABLE 25 VEHICLE SAFETY STANDARDS, BY COUNTRY/REGION

- TABLE 26 LIST OF PATENTS PUBLISHED IN FLEET TELEMATICS MARKET

- TABLE 27 OEM-WISE TELEMATICS DATA PLANS

- TABLE 28 FLEET TELEMATICS MARKET, BY PACKAGE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 29 FLEET TELEMATICS MARKET, BY PACKAGE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 30 FLEET TELEMATICS MARKET, BY PACKAGE TYPE, 2021-2024 (USD MILLION)

- TABLE 31 FLEET TELEMATICS MARKET, BY PACKAGE TYPE, 2025-2032 (USD MILLION)

- TABLE 32 ENTRY LEVEL: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 33 ENTRY LEVEL: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 34 ENTRY LEVEL: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 35 ENTRY LEVEL: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 36 MID TIER: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 37 MID TIER: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 38 MID TIER: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 39 MID TIER: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 40 ADVANCED: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 41 ADVANCED: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 42 ADVANCED: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 43 ADVANCED: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 44 FLEET TELEMATICS MARKET, BY SOLUTION TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 45 FLEET TELEMATICS MARKET, BY SOLUTION TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 46 EMBEDDED: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 47 EMBEDDED: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 48 PORTABLE: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 49 PORTABLE: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 50 SMARTPHONE/CELLULAR: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 51 SMARTPHONE/CELLULAR: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 52 FLEET TELEMATICS MARKET, BY VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 53 FLEET TELEMATICS MARKET, BY VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 54 LIGHT COMMERCIAL VEHICLE: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 55 LIGHT COMMERCIAL VEHICLE: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 56 HEAVY COMMERCIAL VEHICLE: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 57 HEAVY COMMERCIAL VEHICLE: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 58 FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 59 FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 60 OEMS: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 61 OEMS: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 62 AFTERMARKET: FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 63 AFTERMARKET: FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 64 FLEET TELEMATICS MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 65 FLEET TELEMATICS MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 66 NORTH AMERICA: FLEET TELEMATICS MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 67 NORTH AMERICA: FLEET TELEMATICS MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 68 US: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 69 US: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 70 CANADA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 71 CANADA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 72 ASIA PACIFIC: FLEET TELEMATICS MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 73 ASIA PACIFIC: FLEET TELEMATICS MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 74 CHINA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 75 CHINA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 76 INDIA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 77 INDIA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 78 JAPAN: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 79 JAPAN: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 80 SOUTH KOREA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 81 SOUTH KOREA: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 82 EUROPE: FLEET TELEMATICS MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 83 EUROPE: FLEET TELEMATICS MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 84 FRANCE: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 85 FRANCE: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 86 GERMANY: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 87 GERMANY: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 88 ITALY: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 89 ITALY: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 90 SPAIN: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 91 SPAIN: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 92 UK: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 93 UK: FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 94 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- TABLE 95 MARKET SHARE ANALYSIS OF TOP FLEET TELEMATICS SERVICE PROVIDERS, 2025

- TABLE 96 FLEET TELEMATICS MARKET: REGION FOOTPRINT, 2025

- TABLE 97 FLEET TELEMATICS MARKET: SOLUTION TYPE FOOTPRINT, 2025

- TABLE 98 FLEET TELEMATICS MARKET: VEHICLE TYPE FOOTPRINT, 2025

- TABLE 99 FLEET TELEMATICS MARKET: VENDOR TYPE FOOTPRINT, 2025

- TABLE 100 DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 101 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 102 FLEET TELEMATICS MARKET: PRODUCT LAUNCHES & DEVELOPMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 103 FLEET TELEMATICS MARKET: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 104 FLEET TELEMATICS MARKET: EXPANSION, JANUARY 2021-DECEMBER 2025

- TABLE 105 GEOTAB INC.: COMPANY OVERVIEW

- TABLE 106 GEOTAB INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 107 GEOTAB INC.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 108 GEOTAB INC.: DEALS

- TABLE 109 GEOTAB INC.: EXPANSION

- TABLE 110 VERIZON: COMPANY OVERVIEW

- TABLE 111 VERIZON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 112 VERIZON: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 113 VERIZON: DEALS

- TABLE 114 TRIMBLE INC.: COMPANY OVERVIEW

- TABLE 115 TRIMBLE INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 116 TRIMBLE INC.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 117 TRIMBLE INC.: DEALS

- TABLE 118 SAMSARA INC.: COMPANY OVERVIEW

- TABLE 119 SAMSARA INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 120 SAMSARA INC.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 121 SAMSARA INC.: DEALS

- TABLE 122 SAMSARA INC.: EXPANSION

- TABLE 123 SAMSARA INC.: OTHER DEVELOPMENTS

- TABLE 124 POWERFLEET: COMPANY OVERVIEW

- TABLE 125 POWERFLEET: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 126 POWERFLEET: MIX FLEET MANAGER PACKAGE DIFFERENCES

- TABLE 127 POWERFLEET: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 128 POWERFLEET: DEALS

- TABLE 129 POWERFLEET: EXPANSION

- TABLE 130 POWERFLEET: OTHER DEVELOPMENTS

- TABLE 131 TELETRAC NAVMAN US LTD: COMPANY OVERVIEW

- TABLE 132 TELETRAC NAVMAN US LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 133 TELETRAC NAVMAN US LTD.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 134 TELETRAC NAVMAN US LTD.: DEALS

- TABLE 135 TELETRAC NAVMAN US LTD.: OTHER DEVELOPMENTS

- TABLE 136 MASTERNAUT LIMITED: COMPANY OVERVIEW

- TABLE 137 MASTERNAUT LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 138 MASTERNAUT LIMITED: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 139 MASTERNAUT LIMITED: DEALS

- TABLE 140 TOMTOM INTERNATIONAL BV: COMPANY OVERVIEW

- TABLE 141 TOMTOM INTERNATIONAL BV: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 142 TOMTOM INTERNATIONAL BV: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 143 TOMTOM INTERNATIONAL BV: DEALS

- TABLE 144 OMNITRACS: COMPANY OVERVIEW

- TABLE 145 OMNITRACS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 146 OMNITRACS: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 147 OMNITRACS: DEALS

- TABLE 148 OMNITRACS: OTHER DEVELOPMENTS

- TABLE 149 MICROLISE LIMITED: COMPANY OVERVIEW

- TABLE 150 MICROLISE LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 151 MICROLISE LIMITED: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 152 MICROLISE LIMITED: DEALS

- TABLE 153 PTC: COMPANY OVERVIEW

- TABLE 154 PTC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 155 PTC: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 156 PTC: DEALS

- TABLE 157 AZUGA, A BRIDGESTONE COMPANY: COMPANY OVERVIEW

- TABLE 158 AZUGA, A BRIDGESTONE COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 159 AZUGA, A BRIDGESTONE COMPANY: PRODUCT LAUNCHES & DEVELOPMENTS

List of Figures

- FIGURE 1 MARKET SCENARIO

- FIGURE 2 GLOBAL FLEET TELEMATICS MARKET, 2021-2032

- FIGURE 3 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN FLEET TELEMATICS MARKET, 2021-2025

- FIGURE 4 DISRUPTIONS INFLUENCING GROWTH OF FLEET TELEMATICS MARKET

- FIGURE 5 HIGH-GROWTH SEGMENTS IN FLEET TELEMATICS MARKET, 2025-2032

- FIGURE 6 NORTH AMERICA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 7 RISING FOCUS ON IMPROVING FLEET EFFICIENCY TO DRIVE MARKET

- FIGURE 8 OEMS SEGMENT TO ACHIEVE SIGNIFICANT GROWTH DURING FORECAST PERIOD

- FIGURE 9 HEAVY COMMERCIAL VEHICLE SEGMENT TO LEAD MARKET BY 2032

- FIGURE 10 ADVANCED SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 11 EMBEDDED SEGMENT TO LEAD MARKET BY 2032

- FIGURE 12 NORTH AMERICA TO BE LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 13 WORKING OF VEHICLE TELEMATICS

- FIGURE 14 FLEET TELEMATICS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 15 ADOPTION RATE OF TELEMATICS AND FLEET MANAGEMENT SOLUTIONS, 2025

- FIGURE 16 AVERAGE FLEET OPERATING EXPENSES, 2025 (USD)

- FIGURE 17 PRIVACY CONCERNS FROM CONSUMERS AND BUSINESSES

- FIGURE 18 SOLUTION ARCHITECTURE TO GET PREDICTIVE INSIGHTS USING VEHICLE TELEMATICS DATA

- FIGURE 19 GROWTH OF LOGISTICS INDUSTRY, 2016-2030

- FIGURE 20 COMMERCIAL VEHICLE SALES, BY COUNTRY, 2024 (MILLION UNITS)

- FIGURE 21 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 22 AVERAGE SELLING PRICE TREND OF FLEET TELEMATICS, BY PACKAGE TYPE, 2023-2025 (USD PER YEAR)

- FIGURE 23 ENTRY LEVEL: AVERAGE SELLING PRICE, BY REGION, 2023-2025 (USD PER YEAR)

- FIGURE 24 MID TIER: AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD PER YEAR)

- FIGURE 25 ADVANCED: AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD PER YEAR)

- FIGURE 26 FLEET TELEMATICS MARKET ECOSYSTEM

- FIGURE 27 SUPPLY CHAIN ANALYSIS

- FIGURE 28 INVESTMENT & FUNDING SCENARIO, 2022-2025 (USD MILLION)

- FIGURE 29 IMPORT DATA FOR HS CODE 8526-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 30 EXPORT DATA FOR HS CODE 8526-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE

- FIGURE 32 KEY BUYING CRITERIA, BY PACKAGE TYPE

- FIGURE 33 PATENTS APPLIED AND GRANTED, 2015-2025

- FIGURE 34 LEGAL STATUS OF PATENTS PUBLISHED, 2015-2025

- FIGURE 35 5G FEATURES OF FUTURE TELEMATICS

- FIGURE 36 IMPACT OF VEHICLE TELEMATICS ON COST SAVINGS OF WEBFLEET

- FIGURE 37 IMPACT OF VEHICLE TELEMATICS ON COST SAVINGS OF GEOTAB

- FIGURE 38 COST ANALYSIS OF FLEET TELEMATICS SOLUTIONS

- FIGURE 39 FLEET TELEMATICS MARKET, BY PACKAGE TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 40 FLEET TELEMATICS MARKET, BY SOLUTION TYPE, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 41 FLEET TELEMATICS MARKET, BY VEHICLE TYPE, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 42 IN-HAND NETWORKS' TELEMATICS SOLUTIONS FOR LIGHT COMMERCIAL VEHICLES

- FIGURE 43 TOTAL COST OF FLEET OPERATIONS AND BENEFITS OF FLEET MANAGEMENT SYSTEM

- FIGURE 44 FLEET TELEMATICS MARKET, BY VENDOR TYPE, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 45 BENEFITS OF OEM TELEMATICS SOLUTIONS

- FIGURE 46 FLEET TELEMATICS MARKET, BY REGION, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 47 NORTH AMERICA: FLEET TELEMATICS MARKET SNAPSHOT

- FIGURE 48 ASIA PACIFIC: FLEET TELEMATICS MARKET SNAPSHOT

- FIGURE 49 CHINA: FLEET TELEMATICS MARKET DEVELOPMENT

- FIGURE 50 EUROPE: FLEET TELEMATICS MARKET, BY COUNTRY, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 51 MARKET SHARE ANALYSIS OF TOP FLEET TELEMATICS SERVICE PROVIDERS, 2025

- FIGURE 52 REVENUE ANALYSIS OF TOP FIVE LISTED/PUBLIC PLAYERS, 2020-2024 (USD BILLION)

- FIGURE 53 COMPANY VALUATION, 2025 (USD BILLION)

- FIGURE 54 FINANCIAL METRICS, 2025

- FIGURE 55 BRAND/PRODUCT COMPARISON OF TOP FIVE PLAYERS

- FIGURE 56 FLEET TELEMATICS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 57 FLEET TELEMATICS MARKET: COMPANY FOOTPRINT, 2025

- FIGURE 58 FLEET TELEMATICS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 59 EVOLUTION OF FLEET TRACKING THROUGH GEOTAB GO9

- FIGURE 60 GEOTAB INC.: STRONG OPPORTUNITY FOR ADOPTION OF IN-CAB AI COACHING

- FIGURE 61 VERIZON: COMPANY SNAPSHOT

- FIGURE 62 TRIMBLE INC.: COMPANY SNAPSHOT

- FIGURE 63 SAMSARA INC.: COMPANY SNAPSHOT

- FIGURE 64 POWERFLEET: COMPANY SNAPSHOT

- FIGURE 65 POWERFLEET: ENTERPRISE FLEET SOLUTIONS

- FIGURE 66 POWERFLEET: FLEET MANAGEMENT SOLUTIONS

- FIGURE 67 TELETRAC NAVMAN US LTD.: COMPANY SNAPSHOT

- FIGURE 68 MASTERNAUT LIMITED: COMPANY SNAPSHOT

- FIGURE 69 TOMTOM INTERNATIONAL BV: COMPANY SNAPSHOT

- FIGURE 70 OMNITRACS: COMPANY SNAPSHOT

- FIGURE 71 MICROLISE LIMITED: COMPANY SNAPSHOT

- FIGURE 72 PTC: COMPANY SNAPSHOT

- FIGURE 73 AZUGA, A BRIDGESTONE COMPANY: COMPANY SNAPSHOT

- FIGURE 74 RESEARCH DESIGN

- FIGURE 75 RESEARCH PROCESS FLOW

- FIGURE 76 KEY INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 77 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 78 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 79 FLEET TELEMATICS MARKET: BOTTOM-UP APPROACH

- FIGURE 80 FLEET TELEMATICS MARKET: TOP-DOWN APPROACH

- FIGURE 81 DATA TRIANGULATION

- FIGURE 82 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES