PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1961004

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1961004

Data Center Networking Market by Offering (Network Infrastructure, Software), Network Infrastructure (Switches, Routers, NICs & Offload, AI/HPC Hardware), Workload (AI & HPC, General IT), Data Center Size, End User, and Region - Forecast to 2031

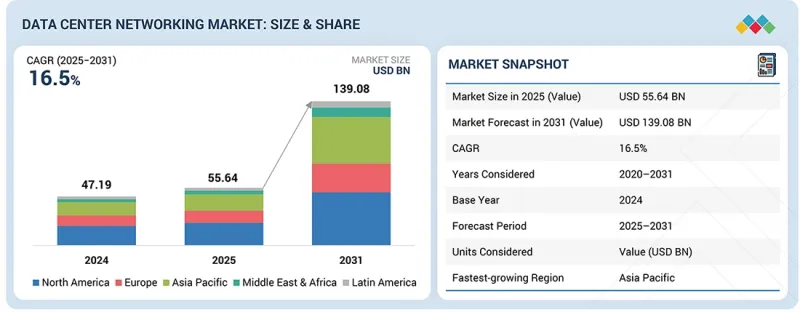

The data center networking market is expanding rapidly, with the market projected to grow from USD 55.64 billion in 2025 to USD 139.08 billion by 2031, at a CAGR of 16.5%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Units Considered | USD (Billion) |

| Segments | By Offering, Network Infrastructure Type, Software, Service, Workload Type, Data Center Size & Capacity, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

The accelerating deployment of AI training clusters, generative AI models, and GPU-dense computing environments is significantly increasing demand for high-performance switching, routing, and offload hardware. Organizations are modernizing their network architectures with 400G and 800G technologies to support massive east-west traffic and scalable cloud environments.

As hyperscale operators expand capacity and enterprises adopt hybrid and multi-cloud strategies, network fabrics must deliver deterministic performance, automation, and advanced security capabilities. The integration of software-defined networking, automation platforms, and programmable network operating systems further enhances scalability and operational efficiency. Growing investments in AI infrastructure, sovereign cloud initiatives, and large-scale data center campuses are strengthening demand for resilient, high-speed data center networking solutions worldwide.

"In software, network management, automation & observability software is expected to register the fastest growth during the forecast period."

Network management, automation & observability software is projected to be the fastest-growing software segment in the data center networking market, driven by increasing network complexity and large-scale AI infrastructure deployments. As hyperscale data centers expand and enterprises adopt multi-cloud and hybrid architectures, managing high-speed fabrics operating at 400G, 800G, and beyond requires advanced automation and real-time visibility. These platforms enable centralized control, zero-touch provisioning, intelligent configuration management, and continuous telemetry monitoring across distributed environments. With the rapid growth of AI clusters and east-west traffic, real-time observability and predictive analytics have become critical for minimizing downtime, detecting congestion, and optimizing performance. Automation tools also help reduce manual intervention, lower operational costs, and improve network reliability. As organizations prioritize scalability, resilience, and operational efficiency, demand for advanced network automation and observability solutions continues to accelerate, positioning this segment as the fastest-growing software category within the data center networking market.

"By offering, the solutions segment is expected to hold the largest market share during the forecast period"

The network infrastructure segment is projected to account for the largest share of the data center networking market, driven by continuous investments in high-performance switching, routing, and offload hardware. As hyperscale data centers expand and AI workloads scale rapidly, demand for advanced Ethernet and InfiniBand switches, high-capacity routers, and intelligent NICs and DPUs continues to rise. These hardware components form the core backbone of modern data center architectures, enabling high-speed east-west and north-south traffic flow across cloud, enterprise, and AI environments. The transition to 400G and 800G technologies, along with the deployment of GPU-dense clusters, significantly increases capital expenditure on physical network infrastructure. Additionally, ongoing refresh cycles from legacy 10G and 40G systems further strengthen hardware demand. Given its critical role in ensuring performance, scalability, and reliability, network infrastructure remains the dominant and highest-revenue-generating offering in the overall data center networking market.

"North America leads the data center networking market, while Asia Pacific is the fastest-growing region driven by rapid hyperscale expansion and AI infrastructure investments."

North America is expected to hold the largest share of the data center networking market due to the strong presence of hyperscale cloud providers, advanced digital infrastructure, and early adoption of high-speed networking technologies. The region hosts a high concentration of large-scale data centers and AI training facilities, driving significant investments in 400G and 800G switching, InfiniBand fabrics, and advanced network interface hardware. Mature fiber connectivity, strong capital expenditure by leading technology companies, and ongoing cloud expansion continue to reinforce its dominant position.

Asia Pacific, however, is projected to be the fastest-growing region during the forecast period. Rapid digital transformation, increasing cloud adoption, government-backed data localization initiatives, and large-scale investments in AI infrastructure across China, India, Japan, and Southeast Asia are accelerating network infrastructure deployments. The expansion of hyperscale campuses and sovereign cloud projects across the region is significantly boosting demand for high-performance data center networking solutions.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the data center networking market.

- By Company: Tier I - 27%, Tier II - 37%, and Tier III - 36%

- By Designation: C-Level Executives - 29%, D-Level Executives -36%, and Others - 35%

- By Region: North America - 35%, Europe - 19%, Asia Pacific - 26%, and RoW - 20%

The report includes a detailed study of key players operating in the data center networking market. The major market participants covered in the study include NVIDIA Corporation (US), Cisco Systems, Inc. (US), Arista Networks, Inc. (US), Huawei Technologies Co., Ltd. (China), Hewlett Packard Enterprise Company (US), Nokia Corporation (Finland), Marvell Technology, Inc. (US), H3C Technologies Co., Ltd. (China), Dell Technologies Inc. (US), Accton Technology Corporation (Taiwan), Extreme Networks, Inc. (US), Ruijie Networks Co., Ltd. (China), Alcatel-Lucent Enterprise (France), Celestica Inc. (Canada), Intel Corporation (US), AMD (US), Quanta Cloud Technology Inc. (Taiwan), Delta Electronics, Inc. (Taiwan), Palo Alto Networks, Inc. (US), Foxconn (Taiwan), Fortinet, Inc. (US), Napatech (Denmark), Arrcus, Inc. (US), Alkira, Inc. (US), and Aviz Networks, Inc. (US).

Research Coverage

This research report categorizes the data center networking market based on Offering (Network Infrastructure, Software, Services), Network Infrastructure Type (Data Center Switches, Data Center Routers, Network Interface & Offload Hardware, AI & HPC Networking Hardware), Port Speed (1-40 Gbps, 40-100 Gbps, 100-400 Gbps, 400 and above), Workload Type (AI & HPC, General-Purpose IT), Data Center Size & Capacity (Small - below 5 MW, Medium - 5-50 MW, Large - above 50 MW), End User (Colocation Data Centers, Hyperscale Data Centers, Enterprise Data Centers), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope encompasses detailed information regarding the major factors influencing market growth, including drivers, restraints, challenges, and opportunities shaping the data center networking landscape. A comprehensive analysis of key industry players has been conducted to provide insights into their business overview, product portfolios, technology offerings, strategic initiatives, partnerships, agreements, product launches, mergers & acquisitions, and recent developments within the data center networking market.

Reason to Buy this Report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall data center networking market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- The report provides insights into key drivers, restraints, opportunities, and challenges shaping the data center networking market. Major drivers include hyperscale capacity expansion, rapid growth in AI and HPC workloads, rising data traffic, and increasing adoption of 400G/800G and InfiniBand-based fabrics. Restraints include interoperability limitations, vendor lock-in concerns, grid power constraints, and high capital expenditure requirements. Opportunities stem from AI cluster expansion, smart, offload-capable switching platforms, virtualization, and the adoption of software-defined networking. Key challenges include component supply constraints, extended equipment lead times, delays in power infrastructure, and rising network complexity, all of which require advanced automation and observability solutions

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the data center networking market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the data center networking market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the data center networking market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and network infrastructure offerings of leading players such as NVIDIA Corporation (US), Cisco Systems, Inc. (US), Arista Networks, Inc. (US), Huawei Technologies Co., Ltd. (China), Hewlett Packard Enterprise Company (US), Nokia Corporation (Finland), Marvell Technology, Inc. (US), H3C Technologies Co., Ltd. (China), Dell Technologies Inc. (US), Accton Technology Corporation (Taiwan), and Extreme Networks, Inc. (US). The report also helps stakeholders understand the data center networking market by providing information on key drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DATA CENTER NETWORKING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER NETWORKING MARKET

- 3.2 DATA CENTER NETWORKING MARKET, BY OFFERING

- 3.3 DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE

- 3.4 DATA CENTER NETWORKING MARKET, BY SOFTWARE

- 3.5 DATA CENTER NETWORKING MARKET, BY SERVICE

- 3.6 DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY

- 3.7 DATA CENTER NETWORKING MARKET, BY END USER

- 3.8 DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER

- 3.9 DATA CENTER NETWORKING MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Hyperscaler capacity expansion programs driving full-fabric networking demand

- 4.2.1.2 AI back-end ethernet increasing network spend per cluster

- 4.2.1.3 High colocation pre-leasing converting capacity commitments into immediate networking demand

- 4.2.1.4 Increase in data traffic and bandwidth

- 4.2.2 RESTRAINTS

- 4.2.2.1 Interoperability limitations and vendor lock-in slowing multi-vendor adoption

- 4.2.2.2 Grid power constraints limiting the pace of networking expansion

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Higher revenue per deployment through smart, offload-capable switching

- 4.2.3.2 AI cluster expansion accelerating high-speed fabric adoption

- 4.2.3.3 Rise in adoption of virtualization technologies to optimize resource utilization

- 4.2.4 CHALLENGES

- 4.2.4.1 Power and grid constraints delaying networking deployment timelines

- 4.2.4.2 Component supply constraints and extended lead times limiting networking equipment availability

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER NETWORKING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Data center networking business models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECASTS

- 5.2.3 TRENDS IN GLOBAL DATA CENTER SOLUTIONS INDUSTRY

- 5.2.4 TRENDS IN GLOBAL SOFTWARE-DEFINED NETWORKING INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 TECHNOLOGY & INFRASTRUCTURE PROVIDERS

- 5.3.2 DATA CENTER NETWORKING PROVIDERS

- 5.3.3 DISTRIBUTORS & RESELLERS

- 5.3.4 SYSTEM INTEGRATORS & CHANNEL PARTNERS

- 5.3.5 END USERS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY SWITCH TYPE, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS OF SWITCHES, BY VENDOR, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 HS CODE: MACHINES FOR THE RECEPTION, CONVERSION, AND TRANSMISSION OR REGENERATION OF VOICE, IMAGES, OR OTHER DATA, INCLUDING SWITCHING AND ROUTING APPARATUS (851762)

- 5.6.1.1 Export Scenario

- 5.6.1.2 Import Scenario

- 5.6.1 HS CODE: MACHINES FOR THE RECEPTION, CONVERSION, AND TRANSMISSION OR REGENERATION OF VOICE, IMAGES, OR OTHER DATA, INCLUDING SWITCHING AND ROUTING APPARATUS (851762)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 MODERNIZING DAIMLER'S DATA CENTER NETWORK THROUGH CISCO SDN

- 5.10.2 COREWEAVE ACCELERATING AI CLOUD PERFORMANCE THROUGH DPU-DRIVEN NETWORKING WITH NVIDIA

- 5.10.3 COSTAISA ACCELERATING HEALTHCARE IT MODERNIZATION WITH HUAWEI DCN SOLUTIONS

- 5.10.4 HOT AISLE BUILDING SCALABLE AI CLOUD INFRASTRUCTURE WITH DELL SONIC NETWORKING

- 5.10.5 MODERNIZING MUNICIPAL INFRASTRUCTURE WITH EXTREME FABRIC CONNECT

- 5.11 IMPACT OF 2025 US TARIFF - DATA CENTER NETWORKING MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END USERS

- 5.11.5.1 Hyperscale data centers

- 5.11.5.2 Colocation data centers

- 5.11.5.3 Enterprise data centers

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 6.5 MARKET PROFITABILITY

- 6.5.1 REVENUE POTENTIAL

- 6.5.2 COST DYNAMICS

- 6.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS, BY REGION

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Middle East & Africa

- 7.1.2.5 Latin America

8 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 8.1 TECHNOLOGY ANALYSIS

- 8.1.1 KEY EMERGING TECHNOLOGIES

- 8.1.1.1 400G/800G Ethernet

- 8.1.1.2 Spine-leaf Fabrics

- 8.1.1.3 SmartNIC/DPU

- 8.1.1.4 Coherent Optics

- 8.1.2 COMPLEMENTARY TECHNOLOGIES

- 8.1.2.1 Streaming Telemetry

- 8.1.2.2 Intent-based Networking

- 8.1.2.3 Networking AIOps

- 8.1.3 ADJACENT TECHNOLOGIES

- 8.1.3.1 AI Compute Clusters

- 8.1.3.2 Cloud-native Platforms

- 8.1.3.3 Edge Data Centers

- 8.1.1 KEY EMERGING TECHNOLOGIES

- 8.2 TECHNOLOGY/PRODUCT ROADMAP

- 8.2.1 SHORT-TERM (2026-2028) | PLATFORM UNIFICATION & COMPLIANCE- BY-DESIGN

- 8.2.2 MID-TERM (2028-2031) | REAL-TIME LABOR ORCHESTRATION & OPERATIONAL INTEGRATION

- 8.2.3 LONG-TERM (2031-2036+) | AUTONOMOUS WORKFORCE OPERATIONS & TRUSTED ECOSYSTEMS

- 8.3 PATENT ANALYSIS

- 8.4 FUTURE APPLICATIONS

- 8.4.1 REAL-TIME AI FABRIC ORCHESTRATION

- 8.4.2 AUTONOMOUS, SELF-OPTIMIZING NETWORK OPERATIONS (AIOPS-DRIVEN NETWORKING)

- 8.4.3 ULTRA HIGH-SPEED, PHOTONIC-BASED NETWORK INTERCONNECT

- 8.4.4 UNIFIED AI-OPTIMIZED ETHERNET FABRICS FOR DISTRIBUTED AI INFRASTRUCTURE

- 8.4.5 MULTI-VENDOR, OPEN AI NETWORKING ECOSYSTEM

- 8.5 IMPACT OF AI/GENERATIVE AI ON DATA CENTER NETWORKING MARKET

- 8.5.1 TOP USE CASES AND MARKET POTENTIAL

- 8.5.2 BEST PRACTICES IN DATA CENTER NETWORKING

- 8.5.3 CASE STUDY OF AI IMPLEMENTATION IN DATA CENTER NETWORKING MARKET

- 8.5.3.1 NVIDIA InfiniBand Networking Powers Meta's AI Research SuperCluster for Hyperscale AI Training

- 8.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 8.5.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN DATA CENTER NETWORKING MARKET

- 8.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 8.6.1 CISCO: AI-OPTIMIZED DATA CENTER NETWORKING SOLUTIONS

- 8.6.2 NVIDIA: AI-CENTRIC DATA CENTER NETWORKING AND ACCELERATED FABRIC SOLUTIONS

9 DATA CENTER NETWORKING MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: DATA CENTER NETWORKING MARKET DRIVERS

- 9.2 NETWORK INFRASTRUCTURE

- 9.2.1 NETWORK INFRASTRUCTURE SHIFTS TOWARD HIGHER-SPEED FABRICS, OPTICS-POWER CO-DESIGN, AND TELEMETRY-AWARE SWITCHING AND ROUTING ARCHITECTURES

- 9.3 SOFTWARE

- 9.3.1 SOFTWARE SHIFTS FROM DEVICE CONFIGURATION TO FABRIC INTENT, STREAMING TELEMETRY, POLICY ENFORCEMENT, AND AUTOMATION WORKFLOWS

- 9.4 SERVICES

- 9.4.1 SERVICES SHIFT FROM MANUAL DEPLOYMENTS TO TEMPLATE-DRIVEN ROLLOUTS, CONTINUOUS VALIDATION, AND TELEMETRY-INFORMED PROACTIVE SUPPORT MODELS

10 DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE

- 10.1 INTRODUCTION

- 10.1.1 NETWORK INFRASTRUCTURE: DATA CENTER NETWORKING MARKET DRIVERS

- 10.2 DATA CENTER SWITCH

- 10.2.1 AI-DRIVEN BANDWIDTH SCALING ACCELERATES TRANSITION TOWARD 400G AND 800G DATA CENTER SWITCHING ARCHITECTURES

- 10.2.2 BY TYPE

- 10.2.2.1 InfiniBand Switches

- 10.2.2.2 Ethernet Switches

- 10.2.2.2.1 Spine Switches

- 10.2.2.2.2 Leaf/Aggregation Switches

- 10.2.2.2.3 Top-of-Rack (ToR) Switches

- 10.2.2.2.4 Other Switches

- 10.2.3 BY PORT SPEED

- 10.2.3.1 1 GBPS to 40 GBPS

- 10.2.3.2 40 GBPS to 100 GBPS

- 10.2.3.3 100 GBPS to 400 GBPS

- 10.2.3.4 400 GBPS and above

- 10.3 DATA CENTER ROUTERS

- 10.3.1 SHIFT TOWARD 800G ROUTING AND IP-OPTICAL CONVERGENCE RESHAPES DATA CENTER BACKBONE ARCHITECTURES

- 10.3.2 CORE ROUTERS

- 10.3.3 EDGE/PEERING ROUTERS

- 10.3.4 AGGREGATION ROUTERS

- 10.3.5 OTHER ROUTERS

- 10.4 NETWORK INTERFACE & OFFLOAD HARDWARE

- 10.4.1 SHIFT TOWARD 400G NICS AND DPUS RESHAPES DATA CENTER HOST CONNECTIVITY ARCHITECTURE

- 10.4.2 NETWORK INTERFACE CARD (NIC)

- 10.4.3 NETWORK ADAPTERS

- 10.4.4 DPUS/IPUS

- 10.5 AI & HPC NETWORKING HARDWARE

- 10.5.1 AI CLUSTER SCALING DRIVES 800G FABRICS, TRANSPORT REDESIGN, AND ENDPOINT ACCELERATION

- 10.5.2 DATA CENTER SWITCHES

- 10.5.2.1 InfiniBand Switches

- 10.5.2.2 Ethernet Switches

- 10.5.3 NETWORK INTERFACE & OFFLOAD HARDWARE

- 10.5.3.1 Network Interface Card (NIC)

- 10.5.3.2 Network Adapters

11 DATA CENTER NETWORKING MARKET, BY SOFTWARE

- 11.1 INTRODUCTION

- 11.1.1 SOFTWARE: DATA CENTER NETWORKING MARKET DRIVERS

- 11.2 NETWORK MANAGEMENT, AUTOMATION & OBSERVABILITY SOFTWARE

- 11.2.1 AUTOMATION AND TELEMETRY-DRIVEN OPERATIONS BECOME CENTRAL TO STABLE, SCALABLE DATA CENTER NETWORK FABRIC MANAGEMENT

- 11.2.2 NETWORK FABRIC & LIFECYCLE OPERATIONS

- 11.2.3 NETWORK AUTOMATION & CONFIGURATION MANAGEMENT

- 11.2.4 MONITORING, TELEMETRY & NETWORK OBSERVABILITY

- 11.3 NETWORK FUNCTION VIRTUALIZATION (NFV) & OFFLOAD SOFTWARE

- 11.3.1 NFV EVOLVES TOWARD CLOUD-NATIVE FUNCTIONS, WITH OFFLOAD AND ACCELERATION SHAPING PERFORMANCE-CRITICAL DATA PATHS

- 11.3.2 VIRTUAL NETWORK SECURITY FUNCTIONS

- 11.3.3 VIRTUAL APPLICATION DELIVERY & LOAD BALANCING

- 11.3.4 PROGRAMMABLE/OFFLOAD NETWORKING SOFTWARE

- 11.3.5 OTHER VIRTUAL NETWORK FUNCTIONS

- 11.4 NETWORK SECURITY SOFTWARE

- 11.4.1 ZERO TRUST-ALIGNED POLICY ENFORCEMENT AND TELEMETRY CORRELATION REDEFINE DATA CENTER NETWORK SECURITY AND RESPONSE OPERATIONS

- 11.4.2 NETWORK SEGMENTATION & POLICY ENFORCEMENT PLATFORMS

- 11.4.3 NETWORK THREAT DETECTION & RESPONSE (NDR)

- 11.4.4 SECURITY ANALYTICS

- 11.4.5 SECURITY ORCHESTRATION FOR NETWORK CONTROLS

- 11.5 SOFTWARE-DEFINED NETWORKING (SDN)

- 11.5.1 SDN SHIFTS TOWARD POLICY INTEGRATION AND OPERATIONAL AUTOMATION ACROSS HYBRID, MULTI-TENANT DATA CENTER NETWORKS

- 11.5.2 SDN CONTROLLERS & POLICY ENGINES

- 11.5.3 NETWORK VIRTUALIZATION & OVERLAY PLATFORMS

- 11.6 NETWORK OPERATING SYSTEMS (NOS)

- 11.6.1 NOS BECOMES OPERATIONS STRATEGY LAYER, PRIORITIZING TELEMETRY, AUTOMATION, AND OPEN, DISAGGREGATED FLEXIBILITY

12 DATA CENTER NETWORKING MARKET, BY SERVICE

- 12.1 INTRODUCTION

- 12.1.1 SERVICE: DATA CENTER NETWORKING MARKET DRIVERS

- 12.2 DESIGN & CONSULTING

- 12.2.1 DESIGN SCOPE EXPANDS TO AI-READY FABRICS, STANDARDS-BASED PHYSICAL BASELINES, AND POLICY-LED SECURITY ARCHITECTURE SERVICES DELIVERABLES

- 12.3 INTEGRATION & DEPLOYMENT

- 12.3.1 INTEGRATION SHIFTS TO DEPLOY-AS-CODE, TEMPLATE-DRIVEN FABRICS, CONTINUOUS VALIDATION, AND TELEMETRY-FIRST COMMISSIONING AT SCALE FOR PROGRAMS

- 12.4 SUPPORT & MAINTENANCE

- 12.4.1 SUPPORT MOVES TOWARD PROACTIVE, TELEMETRY-INFORMED OPERATIONS, AI-ASSISTED WORKFLOWS, AND SAAS MANAGEMENT PLANE COVERAGE WITH GOVERNANCE

13 DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE

- 13.1 INTRODUCTION

- 13.1.1 WORKLOAD TYPE: DATA CENTER NETWORKING MARKET DRIVERS

- 13.2 AI & HPC

- 13.2.1 AI/HPC NETWORKS MOVE TO 800G FABRICS WITH TELEMETRY-BASED VISIBILITY, CONGESTION CONTROL, AND OPEN ETHERNET STANDARDS

- 13.3 GENERAL PURPOSE IT

- 13.3.1 GENERAL IT WORKLOADS CONTINUE TO RELY ON VXLAN-EVPN OVERLAYS AND ETHERNET LEAF-SPINE FABRIC DESIGNS

14 DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY

- 14.1 INTRODUCTION

- 14.1.1 DATA CENTER SIZE & CAPACITY: DATA CENTER NETWORKING MARKET DRIVERS

- 14.2 SMALL DATA CENTERS (BELOW 5 MW)

- 14.2.1 SMALL SITES FAVOR SIMPLIFIED FABRICS, REMOTE OPERABILITY, AND COLLAPSED DESIGNS DRIVEN BY LIMITED ON-SITE EXPERTISE

- 14.3 MEDIUM DATA CENTERS (5-50 MW)

- 14.3.1 MEDIUM SITES SHIFT TOWARD FABRIC OPERATING MODELS, EVPN/VXLAN STANDARDIZATION, AND DCI READINESS FOR TENANCY

- 14.4 LARGE DATA CENTERS (ABOVE 50 MW)

- 14.4.1 LARGE CAMPUSES INDUSTRIALIZE NETWORKING WITH AUTOMATION-FIRST BUILDS, OPTICS ROADMAPS, AND MULTI-SITE AI FABRIC CONSISTENCY

15 DATA CENTER NETWORKING MARKET, BY END USER

- 15.1 INTRODUCTION

- 15.1.1 END USER: DATA CENTER NETWORKING MARKET DRIVERS

- 15.2 COLOCATION DATA CENTER

- 15.2.1 COLOCATION NETWORKS CENTER ON INTERCONNECTION DENSITY, PRIVATE CLOUD ON-RAMPS, AND HIGH-SPEED DCI FOR AI

- 15.3 HYPERSCALE DATA CENTER

- 15.3.1 HYPERSCALERS PUSH DISAGGREGATED NETWORKING, HIGHER-RADIX SILICON, AND TELEMETRY-DRIVEN AI ETHERNET ACROSS MULTIPLE DATA CENTERS

- 15.4 ENTERPRISE DATA CENTER

- 15.4.1 ENTERPRISES SHIFT TO ZERO TRUST, KUBERNETES POLICY CONTROLS, AND OBSERVABILITY ON EVPN/VXLAN OVERLAY FABRICS

- 15.4.2 BFSI

- 15.4.3 TECHNOLOGY & SOFTWARE

- 15.4.4 TELECOMMUNICATIONS

- 15.4.5 GOVERNMENT & PUBLIC SECTOR

- 15.4.6 HEALTHCARE & LIFE SCIENCES

- 15.4.7 LOGISTICS & TRANSPORTATION

- 15.4.8 RETAIL & E-COMMERCE

- 15.4.9 MANUFACTURING

- 15.4.10 ENERGY & UTILITIES

- 15.4.11 OTHERS (MEDIA & ENTERTAINMENT AND EDUCATION)

16 DATA CENTER NETWORKING MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 AI and Cloud-led Data Center Expansion Driving Advanced Networking Deployments Across US

- 16.2.2 CANADA

- 16.2.2.1 Government Investments Accelerating Data Center Networking Deployment in Canada

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 UK

- 16.3.1.1 Expansion of Regional Data Center Clusters Strengthening Demand for Scalable Network Architectures Across UK

- 16.3.2 GERMANY

- 16.3.2.1 Government-supported Federated Cloud Infrastructure Strengthening Data Center Networking Investments Across Germany

- 16.3.3 FRANCE

- 16.3.3.1 Expansion of Digital Infrastructure Reinforcing Demand for Low-latency and High-bandwidth Network Connectivity

- 16.3.4 ITALY

- 16.3.4.1 Expansion of Data Center Campuses in Milan Accelerating High-performance Network Investments

- 16.3.5 REST OF EUROPE

- 16.3.1 UK

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Eastern Data, Western Compute Driving Cross-regional Networking Needs

- 16.4.2 INDIA

- 16.4.2.1 Sovereign AI Infrastructure Development Increasing Demand for High-performance Networking

- 16.4.3 JAPAN

- 16.4.3.1 Expansion Beyond Tokyo and Osaka Driving Long-distance Data Center Networking Investments

- 16.4.4 AUSTRALIA & NEW ZEALAND

- 16.4.4.1 Hyperscale Availability Zone Expansion Driving Inter-city Network Infrastructure Demand

- 16.4.5 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.5.1.1 Saudi Arabia

- 16.5.1.1.1 Government Digital Transformation Increasing Demand for Secure and Low-latency Network

- 16.5.1.2 UAE

- 16.5.1.2.1 Data Sovereignty Regulations Strengthening Domestic Network Infrastructure Investments

- 16.5.1.3 Other GCC countries

- 16.5.1.1 Saudi Arabia

- 16.5.2 SOUTH AFRICA

- 16.5.2.1 Subsea Cable Expansions Strengthening South Africa's Global Data Center Connectivity

- 16.5.3 REST OF MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.6 LATIN AMERICA

- 16.6.1 BRAZIL

- 16.6.1.1 Scaling Network Infrastructure to Support Brazil's Increasing Data Traffic Volumes

- 16.6.2 MEXICO

- 16.6.2.1 Expanding Fiber Connectivity to Support Mexico's Growing Data Center Footprint

- 16.6.3 REST OF LATIN AMERICA

- 16.6.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 INTRODUCTION

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2025

- 17.3 REVENUE ANALYSIS, NETWORKING BUSINESS SEGMENT, 2021-2024

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.5 PRODUCT COMPARISON

- 17.5.1 CISCO

- 17.5.2 ARISTA NETWORKS

- 17.5.3 NVIDIA

- 17.5.4 HUAWEI

- 17.5.5 HPE

- 17.6 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 17.6.1 STARS

- 17.6.2 EMERGING LEADERS

- 17.6.3 PERVASIVE PLAYERS

- 17.6.4 PARTICIPANTS

- 17.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.6.5.1 Company footprint

- 17.6.5.2 Region footprint

- 17.6.5.3 Offering footprint

- 17.6.5.4 Network infrastructure footprint

- 17.6.5.5 Software footprint

- 17.6.5.6 Service footprint

- 17.6.5.7 Workload type footprint

- 17.6.5.8 Data center size & capacity footprint

- 17.6.5.9 End user footprint

- 17.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 17.7.1 PROGRESSIVE COMPANIES

- 17.7.2 RESPONSIVE COMPANIES

- 17.7.3 DYNAMIC COMPANIES

- 17.7.4 STARTING BLOCKS

- 17.7.5 COMPETITIVE BENCHMARKING: STARTUP/SMES, 2024

- 17.7.5.1 Detailed list of key startups/SMEs

- 17.7.5.2 Competitive benchmarking of key startups/SMEs

- 17.8 COMPANY VALUATION AND FINANCIAL METRICS

- 17.8.1 COMPANY VALUATION OF KEY VENDORS

- 17.8.2 FINANCIAL METRICS OF KEY VENDORS

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

18 COMPANY PROFILES

- 18.1 INTRODUCTION

- 18.2 KEY PLAYERS

- 18.2.1 CISCO

- 18.2.1.1 Business overview

- 18.2.1.2 Products/Solutions/Services offered

- 18.2.1.3 Recent developments

- 18.2.1.3.1 Product launches

- 18.2.1.3.2 Deals

- 18.2.1.4 MnM view

- 18.2.1.4.1 Right to win

- 18.2.1.4.2 Strategic choices

- 18.2.1.4.3 Weaknesses and competitive threats

- 18.2.2 ARISTA NETWORKS

- 18.2.2.1 Business overview

- 18.2.2.2 Products/Solutions/Services offered

- 18.2.2.3 Recent developments

- 18.2.2.3.1 Product launches

- 18.2.2.3.2 Deals

- 18.2.2.4 MnM view

- 18.2.2.4.1 Right to win

- 18.2.2.4.2 Strategic choices

- 18.2.2.4.3 Weaknesses and competitive threats

- 18.2.3 NVIDIA

- 18.2.3.1 Business overview

- 18.2.3.2 Products/Solutions/Services offered

- 18.2.3.2.1 Product launches

- 18.2.3.2.2 Deals

- 18.2.3.3 MnM view

- 18.2.3.3.1 Right to win

- 18.2.3.3.2 Strategic choices

- 18.2.3.3.3 Weaknesses and competitive threats

- 18.2.4 HUAWEI

- 18.2.4.1 Business overview

- 18.2.4.2 Products/Solutions/Services offered

- 18.2.4.3 Recent developments

- 18.2.4.3.1 Product launches

- 18.2.4.3.2 Deals

- 18.2.4.4 MnM view

- 18.2.4.4.1 Right to win

- 18.2.4.4.2 Strategic choices

- 18.2.4.4.3 Weaknesses and competitive threats

- 18.2.5 HPE

- 18.2.5.1 Business overview

- 18.2.5.2 Products/Solutions/Services offered

- 18.2.5.3 Recent developments

- 18.2.5.3.1 Product launches

- 18.2.5.3.2 Deals

- 18.2.5.4 MnM view

- 18.2.5.4.1 Right to win

- 18.2.5.4.2 Strategic choices

- 18.2.5.4.3 Weaknesses and competitive threats

- 18.2.6 DELL TECHNOLOGIES

- 18.2.6.1 Business overview

- 18.2.6.2 Products/Solutions/Services offered

- 18.2.6.3 Recent developments

- 18.2.6.3.1 Product launches

- 18.2.6.3.2 Deals

- 18.2.7 EXTREME NETWORKS

- 18.2.7.1 Business overview

- 18.2.7.2 Products/Solutions/Services offered

- 18.2.7.3 Recent developments

- 18.2.7.3.1 Product launches

- 18.2.7.3.2 Deals

- 18.2.8 NOKIA

- 18.2.8.1 Business overview

- 18.2.8.2 Products/Solutions/Services offered

- 18.2.8.3 Recent developments

- 18.2.8.3.1 Product launches

- 18.2.8.3.2 Deals

- 18.2.9 H3C

- 18.2.9.1 Business overview

- 18.2.9.2 Products/Solutions/Services offered

- 18.2.9.3 Recent developments

- 18.2.9.3.1 Product launches

- 18.2.9.3.2 Deals

- 18.2.10 ACCTON TECHNOLOGY

- 18.2.10.1 Business overview

- 18.2.10.2 Products/Solutions/Services offered

- 18.2.10.3 Recent developments

- 18.2.10.3.1 Product launches

- 18.2.10.3.2 Deals

- 18.2.1 CISCO

- 18.3 OTHER PLAYERS

- 18.3.1 MARVELL TECHNOLOGY

- 18.3.2 BROADCOM

- 18.3.3 INTEL CORPORATION

- 18.3.4 AMD

- 18.3.5 QUANTA CLOUD TECHNOLOGY

- 18.3.6 DELTA ELECTRONICS

- 18.3.7 CELESTICA

- 18.3.8 NETRIS

- 18.3.9 FORTINET

- 18.3.10 NAPATECH

- 18.3.11 RUIJIE NETWORKS

- 18.3.12 PAL0 ALTO NETWORKS

- 18.3.13 ARRCUS INC.

- 18.3.14 ALKIRA

- 18.3.15 AVIZ NETWORKS

- 18.3.16 DRIVENETS

- 18.3.17 ALCATEL-LUCENT

- 18.3.18 ZPE SYSTEM

- 18.3.19 NEC CORPORATION

- 18.3.20 ZTE

- 18.3.21 HEDGEHOG

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH APPROACH

- 19.1.1 SECONDARY DATA

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Breakup of primary interviews

- 19.1.2.2 Key industry insights

- 19.2 MARKET BREAKUP AND DATA TRIANGULATION

- 19.3 MARKET SIZE ESTIMATION

- 19.3.1 TOP-DOWN APPROACH

- 19.3.2 BOTTOM-UP APPROACH

- 19.3.3 MARKET ESTIMATION APPROACHES

- 19.4 MARKET FORECAST

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2020-2025

- TABLE 2 IMPACT OF PORTER'S FIVE FORCES ON DATA CENTER NETWORKING MARKET

- TABLE 3 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2029

- TABLE 4 DATA CENTER NETWORKING MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 5 AVERAGE SELLING PRICE, BY SWITCH TYPE, 2025

- TABLE 6 INDICATIVE PRICING ANALYSIS OF SWITCHES, BY VENDOR, 2025

- TABLE 7 EXPORT SCENARIO FOR HS CODE: 851762, BY COUNTRY, 2022-2024 (USD THOUSAND)

- TABLE 8 IMPORT SCENARIO FOR HS CODE: 851762, BY COUNTRY, 2022-2024 (USD THOUSAND)

- TABLE 9 DATA CENTER NETWORKING MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2026

- TABLE 10 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS (%)

- TABLE 12 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 13 DATA CENTER NETWORKING MARKET: UNMET NEEDS IN KEY END-USER INDUSTRIES

- TABLE 14 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 MIDDLE EAST & AFRICA AND LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 LIST OF GRANTED PATENTS IN DATA CENTER NETWORKING MARKET

- TABLE 19 TOP USE CASES AND MARKET POTENTIAL

- TABLE 20 BEST PRACTICES: COMPANIES IMPLEMENTING AI IN DATA CENTER NETWORKING

- TABLE 21 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPLICATIONS FOR MARKET PLAYERS

- TABLE 22 DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 23 DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 24 NETWORK INFRASTRUCTURE: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 25 NETWORK INFRASTRUCTURE: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 26 SOFTWARE: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 27 SOFTWARE: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 28 SERVICES: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 29 SERVICES: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 30 DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2020-2024 (USD MILLION)

- TABLE 31 DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2025-2031 (USD MILLION)

- TABLE 32 DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 33 DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 34 DATA CENTER SWITCH: DATA CENTER NETWORKING MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 35 DATA CENTER SWITCH: DATA CENTER NETWORKING MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 36 INFINITY SWITCHES: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 37 INFINITY SWITCHES: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 38 ETHERNET SWITCHES: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 39 ETHERNET SWITCHES: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 40 DATA CENTER SWITCHES: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2020-2024 (USD MILLION)

- TABLE 41 DATA CENTER SWITCHES: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2025-2031 (USD MILLION)

- TABLE 42 1 GBPS TO 40 GBPS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 43 1 GBPS TO 40 GBPS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 44 40 GBPS TO 100 GBPS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 45 40 GBPS TO 100 GBPS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 46 100 GBPS TO 400 GBPS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 47 100 GBPS TO 400 GBPS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 48 400 GBPS AND ABOVE: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 49 400 GBPS AND ABOVE: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 50 DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2020-2024 (USD MILLION)

- TABLE 51 DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2025-2031 (USD MILLION)

- TABLE 52 CORE ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 53 CORE ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 54 EDGE/PEERING ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 55 EDGE/PEERING ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 56 AGGREGATION ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 57 AGGREGATION ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 58 OTHER ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 59 OTHER ROUTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 60 DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2020-2024 (USD MILLION)

- TABLE 61 DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2025-2031 (USD MILLION)

- TABLE 62 NETWORK INTERFACE CARDS (NIC): DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 63 NETWORK INTERFACE CARDS (NIC): DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 64 NETWORK ADAPTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 65 NETWORK ADAPTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 66 DPUS/IPUS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 67 DPUS/IPUS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 68 DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2020-2024 (USD MILLION)

- TABLE 69 DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2025-2031 (USD MILLION)

- TABLE 70 DATA CENTER SWITCHES: DATA CENTER NETWORKING MARKET FOR AI & HPC NETWORKING HARDWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 71 DATA CENTER SWITCHES: DATA CENTER NETWORKING MARKET FOR AI & HPC NETWORKING HARDWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 72 NETWORK INTERFACE & OFFLOAD HARDWARE: DATA CENTER NETWORKING MARKET FOR AI & HPC NETWORKING HARDWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 73 NETWORK INTERFACE & OFFLOAD HARDWARE: DATA CENTER NETWORKING MARKET FOR AI & HPC NETWORKING HARDWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 74 DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2020-2024 (USD MILLION)

- TABLE 75 DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2025-2031 (USD MILLION)

- TABLE 76 NETWORK MANAGEMENT, AUTOMATION & OBSERVABILITY SOFTWARE: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 77 NETWORK MANAGEMENT, AUTOMATION & OBSERVABILITY SOFTWARE: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 78 NETWORK FUNCTION VIRTUALIZATION (NFV) & OFFLOAD SOFTWARE: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 79 NETWORK FUNCTION VIRTUALIZATION (NFV) & OFFLOAD SOFTWARE: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 80 NETWORK SECURITY SOFTWARE: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 81 NETWORK SECURITY SOFTWARE: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 82 SOFTWARE-DEFINED NETWORK: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 83 SOFTWARE-DEFINED NETWORK: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 84 NETWORK OPERATING SYSTEM: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 85 NETWORK OPERATING SYSTEM: DATA CENTER NETWORKING MARKET FOR SOFTWARE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 86 DATA CENTER NETWORKING MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 87 DATA CENTER NETWORKING MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 88 DESIGN & CONSULTING: DATA CENTER NETWORKING MARKET FOR SERVICES, BY REGION, 2020-2024 (USD MILLION)

- TABLE 89 DESIGN & CONSULTING: DATA CENTER NETWORKING MARKET FOR SERVICES, BY REGION, 2025-2031 (USD MILLION)

- TABLE 90 INTEGRATION & DEPLOYMENT: DATA CENTER NETWORKING MARKET FOR SERVICES, BY REGION, 2020-2024 (USD MILLION)

- TABLE 91 INTEGRATION & DEPLOYMENT: DATA CENTER NETWORKING MARKET FOR SERVICES, BY REGION, 2025-2031 (USD MILLION)

- TABLE 92 SUPPORT & MAINTENANCE: DATA CENTER NETWORKING MARKET FOR SERVICES, BY REGION, 2020-2024 (USD MILLION)

- TABLE 93 SUPPORT & MAINTENANCE: DATA CENTER NETWORKING MARKET FOR SERVICES, BY REGION, 2025-2031 (USD MILLION)

- TABLE 94 DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2020-2024 (USD MILLION)

- TABLE 95 DATA CENTER NETWORKING MARKET, BY SERVICES, 2025-2031 (USD MILLION)

- TABLE 96 AI & HPC: DATA CENTER NETWORKING MARKET FOR WORKLOAD TYPE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 97 AI & HPC: DATA CENTER NETWORKING MARKET FOR WORKLOAD TYPE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 98 GENERAL PURPOSE IT: DATA CENTER NETWORKING MARKET FOR WORKLOAD TYPE, BY REGION, 2020-2024 (USD MILLION)

- TABLE 99 GENERAL PURPOSE IT: DATA CENTER NETWORKING MARKET FOR WORKLOAD TYPE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 100 DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2020-2024 (USD MILLION)

- TABLE 101 DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2025-2031 (USD MILLION)

- TABLE 102 SMALL DATA CENTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 103 SMALL DATA CENTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 104 MEDIUM DATA CENTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 105 MEDIUM DATA CENTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 106 LARGE DATA CENTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 107 LARGE DATA CENTERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 108 DATA CENTER NETWORKING MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 109 DATA CENTER NETWORKING MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 110 COLOCATION DATA CENTER: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 111 COLOCATION DATA CENTER: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 112 HYPERSCALE DATA CENTER: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 113 HYPERSCALE DATA CENTER: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 114 ENTERPRISE DATA CENTER: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 115 ENTERPRISE DATA CENTER: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 116 DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2020-2024 (USD MILLION)

- TABLE 117 DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2025-2031 (USD MILLION)

- TABLE 118 BFSI: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 119 BFSI: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 120 TECHNOLOGY & SOFTWARE: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 121 TECHNOLOGY & SOFTWARE: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 122 TELECOMMUNICATIONS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 123 TELECOMMUNICATIONS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 124 GOVERNMENT & PUBLIC SECTOR: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 125 GOVERNMENT & PUBLIC SECTOR: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 126 HEALTHCARE & LIFE SCIENCES: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 127 HEALTHCARE & LIFE SCIENCES: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 128 LOGISTICS & TRANSPORTATION: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 129 LOGISTICS & TRANSPORTATION: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 130 RETAIL & E-COMMERCE: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 131 RETAIL & E-COMMERCE: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 132 MANUFACTURING: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 133 MANUFACTURING: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 134 ENERGY & UTILITIES: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 135 ENERGY & UTILITIES: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 136 OTHERS: DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 137 OTHERS: DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 138 DATA CENTER NETWORKING MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 139 DATA CENTER NETWORKING MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 140 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 141 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 142 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2020-2024 (USD MILLION)

- TABLE 143 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2025-2031 (USD MILLION)

- TABLE 144 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 145 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 146 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2020-2024 (USD MILLION)

- TABLE 147 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2025-2031 (USD MILLION)

- TABLE 148 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2020-2024 (USD MILLION)

- TABLE 149 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2025-2031 (USD MILLION)

- TABLE 150 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2020-2024 (USD MILLION)

- TABLE 151 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2025-2031 (USD MILLION)

- TABLE 152 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2020-2024 (USD MILLION)

- TABLE 153 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2025-2031 (USD MILLION)

- TABLE 154 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2020-2024 (USD MILLION)

- TABLE 155 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2025-2031 (USD MILLION)

- TABLE 156 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 157 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 158 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2020-2024 (USD MILLION)

- TABLE 159 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2025-2031 (USD MILLION)

- TABLE 160 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2020-2024 (USD MILLION)

- TABLE 161 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2025-2031 (USD MILLION)

- TABLE 162 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 163 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 164 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2020-2024 (USD MILLION)

- TABLE 165 NORTH AMERICA: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2025-2031 (USD MILLION)

- TABLE 166 US: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 167 US: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 168 US: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 169 US: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 170 CANADA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 171 CANADA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 172 EUROPE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 173 EUROPE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 174 EUROPE: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2020-2024 (USD MILLION)

- TABLE 175 EUROPE: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2025-2031 (USD MILLION)

- TABLE 176 EUROPE: DATA CENTER NETWORKING MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 177 EUROPE: DATA CENTER NETWORKING MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 178 EUROPE: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2020-2024 (USD MILLION)

- TABLE 179 EUROPE: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2025-2031 (USD MILLION)

- TABLE 180 EUROPE: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2020-2024 (USD MILLION)

- TABLE 181 EUROPE: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2025-2031 (USD MILLION)

- TABLE 182 EUROPE: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2020-2024 (USD MILLION)

- TABLE 183 EUROPE: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2025-2031 (USD MILLION)

- TABLE 184 EUROPE: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2020-2024 (USD MILLION)

- TABLE 185 EUROPE: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2025-2031 (USD MILLION)

- TABLE 186 EUROPE: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2020-2024 (USD MILLION)

- TABLE 187 EUROPE: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2025-2031 (USD MILLION)

- TABLE 188 EUROPE: DATA CENTER NETWORKING MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 189 EUROPE: DATA CENTER NETWORKING MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 190 EUROPE: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2020-2024 (USD MILLION)

- TABLE 191 EUROPE: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2025-2031 (USD MILLION)

- TABLE 192 EUROPE: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2020-2024 (USD MILLION)

- TABLE 193 EUROPE: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2025-2031 (USD MILLION)

- TABLE 194 EUROPE: DATA CENTER NETWORKING MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 195 EUROPE: DATA CENTER NETWORKING MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 196 EUROPE: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2020-2024 (USD MILLION)

- TABLE 197 EUROPE: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2025-2031 (USD MILLION)

- TABLE 198 EUROPE: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 199 EUROPE: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 200 UK: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 201 UK: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 202 GERMANY: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 203 GERMANY: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 204 FRANCE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 205 FRANCE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 206 ITALY: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 207 ITALY: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 208 REST OF EUROPE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 209 REST OF EUROPE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 210 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 211 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 212 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2020-2024 (USD MILLION)

- TABLE 213 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2025-2031 (USD MILLION)

- TABLE 214 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 215 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 216 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2020-2024 (USD MILLION)

- TABLE 217 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2025-2031 (USD MILLION)

- TABLE 218 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2020-2024 (USD MILLION)

- TABLE 219 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2025-2031 (USD MILLION)

- TABLE 220 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2020-2024 (USD MILLION)

- TABLE 221 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2025-2031 (USD MILLION)

- TABLE 222 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2020-2024 (USD MILLION)

- TABLE 223 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2025-2031 (USD MILLION)

- TABLE 224 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2020-2024 (USD MILLION)

- TABLE 225 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2025-2031 (USD MILLION)

- TABLE 226 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 227 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 228 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2020-2024 (USD MILLION)

- TABLE 229 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2025-2031 (USD MILLION)

- TABLE 230 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2020-2024 (USD MILLION)

- TABLE 231 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2025-2031 (USD MILLION)

- TABLE 232 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 233 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 234 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2020-2024 (USD MILLION)

- TABLE 235 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2025-2031 (USD MILLION)

- TABLE 236 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 237 ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 238 CHINA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 239 CHINA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 240 INDIA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 241 INDIA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 242 JAPAN: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 243 JAPAN: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 244 AUSTRALIA & NEW ZEALAND: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 245 AUSTRALIA & NEW ZEALAND: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 246 REST OF ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 247 REST OF ASIA PACIFIC: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 248 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 249 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 250 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2020-2024 (USD MILLION)

- TABLE 251 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2025-2031 (USD MILLION)

- TABLE 252 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 253 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 254 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2020-2024 (USD MILLION)

- TABLE 255 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2025-2031 (USD MILLION)

- TABLE 256 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2020-2024 (USD MILLION)

- TABLE 257 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2025-2031 (USD MILLION)

- TABLE 258 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2020-2024 (USD MILLION)

- TABLE 259 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2025-2031 (USD MILLION)

- TABLE 260 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2020-2024 (USD MILLION)

- TABLE 261 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2025-2031 (USD MILLION)

- TABLE 262 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2020-2024 (USD MILLION)

- TABLE 263 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2025-2031 (USD MILLION)

- TABLE 264 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 265 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 266 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2020-2024 (USD MILLION)

- TABLE 267 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2025-2031 (USD MILLION)

- TABLE 268 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2020-2024 (USD MILLION)

- TABLE 269 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2025-2031 (USD MILLION)

- TABLE 270 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 271 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 272 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2020-2024 (USD MILLION)

- TABLE 273 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2025-2031 (USD MILLION)

- TABLE 274 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 275 MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 276 GCC COUNTRIES: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 277 GCC COUNTRIES: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 278 GCC COUNTRIES: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 279 GCC COUNTRIES: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 280 SAUDI ARABIA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 281 SAUDI ARABIA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 282 UAE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 283 UAE: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 284 OTHER GCC COUNTRIES: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 285 OTHER GCC COUNTRIES: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 286 SOUTH AFRICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 287 SOUTH AFRICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 288 REST OF MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 289 REST OF MIDDLE EAST & AFRICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 290 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 291 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 292 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2020-2024 (USD MILLION)

- TABLE 293 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE, 2025-2031 (USD MILLION)

- TABLE 294 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 295 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 296 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2020-2024 (USD MILLION)

- TABLE 297 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY PORT SPEED, 2025-2031 (USD MILLION)

- TABLE 298 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2020-2024 (USD MILLION)

- TABLE 299 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER ROUTER, 2025-2031 (USD MILLION)

- TABLE 300 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2020-2024 (USD MILLION)

- TABLE 301 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY NETWORK INTERFACE & OFFLOAD HARDWARE, 2025-2031 (USD MILLION)

- TABLE 302 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2020-2024 (USD MILLION)

- TABLE 303 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY AI & HPC NETWORKING HARDWARE, 2025-2031 (USD MILLION)

- TABLE 304 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2020-2024 (USD MILLION)

- TABLE 305 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY SOFTWARE, 2025-2031 (USD MILLION)

- TABLE 306 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 307 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 308 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2020-2024 (USD MILLION)

- TABLE 309 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY WORKLOAD TYPE, 2025-2031 (USD MILLION)

- TABLE 310 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2020-2024 (USD MILLION)

- TABLE 311 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY, 2025-2031 (USD MILLION)

- TABLE 312 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 313 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 314 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2020-2024 (USD MILLION)

- TABLE 315 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER, 2025-2031 (USD MILLION)

- TABLE 316 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 317 LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 318 BRAZIL: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 319 BRAZIL: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 320 MEXICO: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 321 MEXICO: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 322 REST OF LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 323 REST OF LATIN AMERICA: DATA CENTER NETWORKING MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 324 DATA CENTER NETWORKING MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2023-2025

- TABLE 325 MARKET SHARE OF KEY VENDORS, 2025

- TABLE 326 DATA CENTER NETWORKING MARKET: REGION FOOTPRINT

- TABLE 327 DATA CENTER NETWORKING MARKET: OFFERING FOOTPRINT

- TABLE 328 DATA CENTER NETWORKING MARKET: NETWORK INFRASTRUCTURE FOOTPRINT

- TABLE 329 DATA CENTER NETWORKING MARKET: SOFTWARE FOOTPRINT

- TABLE 330 DATA CENTER NETWORKING MARKET: SERVICE FOOTPRINT

- TABLE 331 DATA CENTER NETWORKING MARKET: WORKLOAD TYPE FOOTPRINT

- TABLE 332 DATA CENTER NETWORKING MARKET: DATA CENTER SIZE & CAPACITY FOOTPRINT

- TABLE 333 DATA CENTER NETWORKING MARKET: END USER FOOTPRINT

- TABLE 334 DATA CENTER NETWORKING MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 335 DATA CENTER NETWORKING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 336 DATA CENTER NETWORKING MARKET: PRODUCT LAUNCHES/ENHANCEMENTS, APRIL 2023-FEBRUARY 2026

- TABLE 337 DATA CENTER NETWORKING MARKET: DEALS, OCTOBER 2023-JANUARY 2026

- TABLE 338 CISCO: COMPANY OVERVIEW

- TABLE 339 CISCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 340 CISCO: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 341 CISCO: DEALS

- TABLE 342 ARISTA NETWORKS: COMPANY OVERVIEW

- TABLE 343 ARISTA NETWORKS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 344 ARISTA NETWORKS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 345 ARISTA NETWORKS: DEALS

- TABLE 346 NVIDIA: COMPANY OVERVIEW

- TABLE 347 NVIDIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 348 NVIDIA: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 349 NVIDIA: DEALS

- TABLE 350 HUAWEI: COMPANY OVERVIEW

- TABLE 351 HUAWEI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 352 HUAWEI: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 353 HUAWEI: DEALS

- TABLE 354 HPE: COMPANY OVERVIEW

- TABLE 355 HPE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 356 HPE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 357 HPE: DEALS

- TABLE 358 DELL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 359 DELL TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 360 DELL TECHNOLOGIES: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 361 DELL TECHNOLOGIES: DEALS

- TABLE 362 EXTREME NETWORKS: COMPANY OVERVIEW

- TABLE 363 EXTREME NETWORKS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 364 EXTREME NETWORKS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 365 EXTREME NETWORKS: DEALS

- TABLE 366 NOKIA: COMPANY OVERVIEW

- TABLE 367 NOKIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 368 NOKIA: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 369 NOKIA: DEALS

- TABLE 370 H3C: COMPANY OVERVIEW

- TABLE 371 H3C: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 372 H3C: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 373 H3C: DEALS

- TABLE 374 ACCTON TECHNOLOGY: COMPANY OVERVIEW

- TABLE 375 ACCTON TECHNOLOGY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 376 ACTON TECHNOLOGY: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 377 ACCTON TECHNOLOGY: DEALS

- TABLE 378 FACTOR ANALYSIS

List of Figures

- FIGURE 1 DATA CENTER NETWORKING MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 MARKET SCENARIO

- FIGURE 3 GLOBAL DATA CENTER NETWORKING MARKET, 2020-2031

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DATA CENTER NETWORKING MARKET (2022-2025)

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF DATA CENTER NETWORKING MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN DATA CENTER NETWORKING MARKET, 2025-2031

- FIGURE 7 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN DATA CENTER NETWORKING MARKET, IN TERMS OF VALUE, DURING FORECAST PERIOD

- FIGURE 8 RISING AI WORKLOAD INTENSITY AND HYPERSCALE EXPANSION TO DRIVE DATA CENTER NETWORKING MARKET

- FIGURE 9 NETWORK INFRASTRUCTURE SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 10 DATA CENTER SWITCH TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 11 NETWORK MANAGEMENT, AUTOMATION & OBSERVABILITY SOFTWARE TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 12 SUPPORT & MAINTENANCE TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 13 LARGE DATA CENTERS (ABOVE 50 MW) TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 14 HYPERSCALE DATA CENTER TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 15 BFSI TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 16 ASIA PACIFIC TO EMERGE AS MOST SIGNIFICANT MARKET IN NEXT SIX YEARS

- FIGURE 17 DATA CENTER NETWORKING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 18 DATA CENTER NETWORKING MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 19 DAAT CENTER NETWORKING MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 20 DATA CENTER NETWORKING MARKET: ECOSYSTEM ANALYSIS

- FIGURE 21 AVERAGE SELLING PRICE, BY SWITCH TYPE, 2025

- FIGURE 22 EXPORT SCENARIO FOR HS CODE: 8471

- FIGURE 23 IMPORT SCENARIO FOR HS CODE: 8471

- FIGURE 24 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 25 DATA CENTER NETWORKING MARKET: INVESTMENT AND FUNDING SCENARIO

- FIGURE 26 DATA CENTER NETWORKING MARKET: DECISION-MAKING FACTOR

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- FIGURE 28 KEY BUYING CRITERIA FOR TOP END USERS

- FIGURE 29 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 30 PATENTS APPLIED AND GRANTED, 2015-2025

- FIGURE 31 FUTURE APPLICATIONS OF DATA CENTER NETWORKING

- FIGURE 32 NETWORK INFRASTRUCTURE TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 33 DATA CENTER SWITCH TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 34 NETWORK MANAGEMENT, AUTOMATION & OBSERVABILITY SOFTWARE TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 35 SUPPORT & MAINTENANCE TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 36 AI & HPC TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 37 LARGE DATA CENTERS TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 38 HYPERSCALE DATA CENTER TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 39 NORTH AMERICA TO REGISTER LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 40 NORTH AMERICA: DATA CENTER NETWORKING MARKET SNAPSHOT

- FIGURE 41 ASIA PACIFIC: DATA CENTER NETWORKING MARKET SNAPSHOT

- FIGURE 42 REVENUE ANALYSIS OF KEY VENDORS, 2021-2024

- FIGURE 43 DATA CENTER NETWORKING MARKET: MARKET SHARE ANALYSIS, 2025

- FIGURE 44 DATA CENTER NETWORKING MARKET: COMPARATIVE ANALYSIS OF VENDOR PRODUCTS

- FIGURE 45 COMPANY EVALUATION MATRIX FOR KEY PLAYERS: CRITERIA WEIGHTAGE

- FIGURE 46 DATA CENTER NETWORKING MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 47 DATA CENTER NETWORKING MARKET: COMPANY FOOTPRINT

- FIGURE 48 COMPANY EVALUATION MATRIX FOR STARTUPS/SMES: CRITERIA WEIGHTAGE

- FIGURE 49 DATA CENTER NETWORKING MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 50 COMPANY VALUATION OF KEY VENDORS

- FIGURE 51 EV/EBITDA ANALYSIS OF KEY VENDORS

- FIGURE 52 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 53 CISCO: COMPANY SNAPSHOT

- FIGURE 54 ARISTA NETWORKS: COMPANY SNAPSHOT

- FIGURE 55 NVIDIA: COMPANY SNAPSHOT

- FIGURE 56 HUAWEI: COMPANY SNAPSHOT

- FIGURE 57 HPE: COMPANY SNAPSHOT

- FIGURE 58 DELL TECHNOLOGIES: COMPANY SNAPSHOT

- FIGURE 59 EXTREME NETWORKS: COMPANY SNAPSHOT

- FIGURE 60 NOKIA: COMPANY SNAPSHOT

- FIGURE 61 ACCTON TECHNOLOGY: COMPANY SNAPSHOT

- FIGURE 62 DATA CENTER NETWORKING MARKET: RESEARCH DESIGN

- FIGURE 63 DATA CENTER NETWORKING MARKET: MARKET BREAKUP AND DATA TRIANGULATION

- FIGURE 64 DATA CENTER NETWORKING MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 65 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 66 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 67 DATA CENTER NETWORKING MARKET: RESEARCH FLOW

- FIGURE 68 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- FIGURE 69 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH FROM SUPPLY SIDE - COLLECTIVE REVENUE OF VENDORS

- FIGURE 70 BOTTOM-UP APPROACH FROM SUPPLY SIDE: COLLECTIVE REVENUE OF VENDORS

- FIGURE 71 DEMAND-SIDE APPROACH: DATA CENTER NETWORKING MARKET