PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1996975

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1996975

X Ray Machine Market for Tire Inspection By System Type, Technology, Use Case, Application, and Region - Global Forecast to 2032

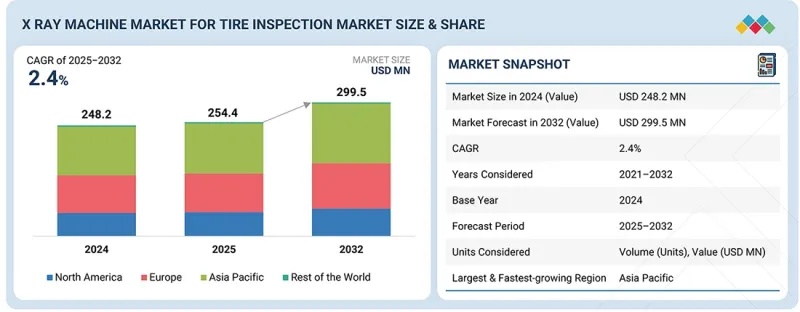

The X ray machine market for tire inspection is projected to grow from USD 254.5 million in 2025 to USD 299.5 million by 2032, at a CAGR of 2.4%. The market is growing as equipment manufacturers are expanding system capabilities to accommodate larger OTR and specialty tires, while broadening their product portfolios across multiple tire sizes, load ratings, and vehicle categories, thereby widening their addressable customer base and application scope.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Volume (Units), Value (USD Million) |

| Segments | System Type, Technology, Use Case, Application, and Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

High-volume passenger and commercial tire plants are implementing 100 percent structural inspection to prevent downstream warranty costs and export rejections. Automated in-line systems are supporting defect traceability, real-time rejection, and process correction. As manufacturers are aligning with zero-defect manufacturing strategies, the demand for integrated high-speed X ray inspection platforms is strengthening.

"The stationary X ray machines are projected to lead the market during the forecast period."

Stationary X ray machines for tire inspection serve as core quality assurance infrastructure within medium and high-volume tire manufacturing plants. Stationary systems are enabling standardized inspection protocols and plant-wide data integration. Digital defect archiving, supporting closed-loop quality control between tire building, curing, and other final inspection stages, is one of the key areas. A stationary X ray machine is driven by increasing internal complexity of modern tires, rising OEM quality benchmarks, growth in EV-specific tire production, expansion of high load commercial vehicle segments, and pressure to minimize field failure rates. Integration with MES platforms and automation systems is allowing stationary installations to function as long-term quality control assets rather than standalone inspection equipment. Their higher throughput capability, consistent inspection accuracy, and suitability for continuous operation are making them the preferred system type for Tier 1 global tire manufacturers. Leading suppliers of stationary X ray tire inspection systems include YXLON International under COMET Group, VisiConsult, Nikon Metrology, Mesnac, and Rayslov Inspection Technology, many of which are integrating automated loading systems and AI-based defect classification modules to support large-scale tire plants.

"The Tier 1 segment is projected to be the largest use case during the forecast period."

Tier 1 manufacturers have large-scale operations, strict compliance obligations, and deep integration with global automotive OEM supply chains. These manufacturers are operating high-volume, automated production lines where each tire is undergoing structural validation before dispatch, particularly across passenger car radial, truck and bus radial, and EV-specific platforms. Global OEMs are enforcing zero-defect policies and traceability standards under frameworks such as IATF 16949, requiring Tier 1 suppliers to validate internal belt alignment, bead integrity, ply overlap, and internal foreign inclusions through non-destructive inspection systems. Tire architectures are also becoming more complex, with multi-layer steel belts, reinforced sidewalls, and noise reduction inserts, making visual inspection insufficient and increasing reliance on high penetration X ray systems. In addition, Tier 1 manufacturers are exporting to regulated markets across Europe and North America, where recall exposure and liability risks are significantly higher, driving proactive investment in advanced inspection technologies. Their stronger capital expenditure capacity and ongoing integration of X-ray systems with MES and AI-driven defect classification platforms are further reinforcing adoption.

"Smart tire integration and regulatory stringency are driving advanced X ray adoption in European manufacturing."

Europe is projected to register the fastest growth in the X ray machine market for tire inspection due to structural changes in tire architecture, stringent regulatory compliance requirements, and rapid migration from conventional 2D radiography to high-resolution 3D CT systems. Tire manufacturers are embedding pressure, temperature, and tread wear sensors directly within the tire structure, which is increasing internal architecture complexity and introducing additional interfaces between rubber compounds, steel belts, and electronic modules. This structural integration requires higher penetration and higher resolution X ray systems to detect micro voids, cord displacement, air entrapment, and bonding inconsistencies around embedded components. Conventional 2D systems are being supplemented or replaced by advanced digital radiography and 3D CT platforms to ensure precise validation of sensor positioning and structural integrity. At the same time, stringent compliance requirements under the European Tire and Rim Technical Organisation and certification frameworks governed by the European Union Aviation Safety Agency are reinforcing zero-defect manufacturing and traceability mandates. European tire plants are operating highly automated production lines, where stationary in-line X ray systems are being integrated with curing presses, robotic handling units, and MES platforms to enable 100 percent inspection and digital defect mapping. This automation maturity is accelerating the shift toward fully integrated inspection cells rather than standalone offline testing.

The competitive ecosystem includes European X ray technology providers such as Yxlon International, VisiConsult, RX Solutions, and Nikon Metrology, working closely with leading tire manufacturers, including Continental AG, Michelin, and Pirelli. Stationary in-line digital radiography remains the preferred configuration for high-volume passenger and truck tire production, while offline 3D CT systems are increasingly used for smart tire validation, R&D characterization, and premium segment approval. For instance, Continental AG in Germany has embedded sensor technologies that are being validated through enhanced internal X-ray inspection protocols to ensure accurate module placement and long-term structural bonding performance prior to commercial deployment.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: X Ray Machine Manufacturers for Tire Inspection- 50%, Tire Manufacturers - 40%, Others - 10%

- By Designation: CXOs - 30%, Directors - 40%, Others - 30%

- By Country: Asia Pacific - 20%, North America - 20%, Europe - 50%, and Rest of the World - 10%

Major players in the X ray machine market for tire inspection are AMETEK Micro-Poise (US), Technip Energies N.V. (France), Comet (Germany), MESNAC (China), and Nikon Corporation Industrial Solutions (Japan). These players have been adopting various strategies to sustain their positions in the market. Major strategies adopted are product launches, deals, and expansions. These strategies have been analyzed to understand the positions of these companies in the market. Manufacturers focus on maintaining their strategic position in the market by offering advanced, various X ray tire inspection machine solutions to meet evolving regulatory and consumer demands.

Research Coverage:

The report covers the X ray machine market for tire inspection, in terms of system type (stationary (in-line and off-line), mobile), technology (2D X ray and 3D CT), Use Case (Tier 1, OEM, and aftermarket), application (tire inspection, tread inspection, sidewall inspection, bead inspection and others), and region (Asia Pacific, Europe, North America, and Rest of the World). It covers the competitive landscape and company profiles of the major players in the ecosystem.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- This report will help market leaders/new entrants in this market with information on the closest approximations of revenue numbers for the X ray machine market for tire inspection ecosystem and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies.

- This report will also help stakeholders understand the market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (increasing internal inspection practices, advanced 3D imaging capabilities increasing demand, increase in vehicles on road and tire replacement cycles driving higher internal inspection), restraints (high capital investment per inspection line, higher installation and service complexity), opportunities (AI-driven automated defect classification, integration of X ray inspection with manufacturing execution system), and challenges (balancing image resolution with tire production speed)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the X ray machine market for tire inspection across varied regions)

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading market players like AMETEK Micro-Poise (US), Technip Energies N.V. (France), Comet (Germany), MESNAC (China), and Nikon Corporation Industrial Solutions (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN X RAY MACHINE MARKET FOR TIRE INSPECTION

- 2.4 HIGH-GROWTH SEGMENTS IN X RAY MACHINE MARKET FOR TIRE INSPECTION

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 OPPORTUNITIES FOR PLAYERS IN X RAY MACHINE MARKET FOR TIRE INSPECTION

- 3.2 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY SYSTEM TYPE

- 3.3 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- 3.4 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY USE CASE

- 3.5 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing internal inspection practices

- 4.2.1.2 Advanced 3D imaging capabilities

- 4.2.1.3 Increase in vehicles on road and tire replacement cycles driving higher internal inspection

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital investment per inspection line

- 4.2.2.2 Higher installation and service complexity

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 AI-driven automated defect classification

- 4.2.3.2 Integration of X ray inspection with manufacturing execution system

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing image resolution with tire production speed

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY KEY PLAYERS IN X RAY MACHINE MARKET FOR TIRE INSPECTION

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 US PROVIDING STABLE OUTLOOK FOR TIRE INVESTMENTS AND DEMAND TO BE SUPPORTED BY ONGOING UPGRADES IN TIRE INSPECTION

- 5.1.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 COMPONENT SUPPLIERS

- 5.2.2 SUBSYSTEM PROVIDERS

- 5.2.3 SOFTWARE PROVIDERS

- 5.2.4 X RAY TIRE INSPECTION MACHINE MANUFACTURERS

- 5.2.5 END USERS (TIRE MANUFACTURERS, OEMS, AND OTHERS)

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, 2026

- 5.4.2 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY, 2025-2026

- 5.4.3 AVERAGE SELLING PRICE TREND, BY REGION, 2024-2026

- 5.5 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 902219)

- 5.8.2 EXPORT SCENARIO (HS CODE 902219)

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 INLINE 2D DIGITAL X RAY FOR HIGH-VOLUME PASSENGER CAR TIRE PRODUCTION

- 5.9.2 AUTOMATED 2D X RAY WITH AI DEFECT RECOGNITION FOR OEM TIRE SUPPLY

- 5.9.3 INDUSTRIAL CT FOR PREMIUM SUV AND PERFORMANCE TIRE VALIDATION

- 5.9.4 CT BASED INTERNAL STRUCTURE ANALYSIS FOR HIGH-PERFORMANCE TIRE DESIGN

- 5.9.5 INDUSTRIAL CT FOR OEM HOMOLOGATION AND GEOMETRIC VALIDATION

- 5.9.6 LAB-BASED DIGITAL X RAY FOR OEM RETURN FAILURE ANALYSIS

- 5.10 IMPACT OF 2026 EU-INDIA TRADE DEAL

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 SUPPLY CHAIN AND LOCALIZATION IMPACT

- 5.10.5 STRATEGIC MARKET OUTLOOK

- 5.11 ANALYSIS OF LEADING X RAY MACHINE MANUFACTURERS FOR TIRE INSPECTION

- 5.11.1 X RAY TIRE INSPECTION MACHINE COMPARISON BY KEY PLAYERS

- 5.11.2 INLINE VS. OFFLINE ADOPTION TRENDS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 3D TIRE TOMOGRAPHY RECONSTRUCTION

- 6.1.2 AUTOMATIC DEFECT RECOGNITION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 PHASE CONTRAST AND ADVANCED IMAGING PHYSICS

- 6.2.2 STATISTICAL DEFECT MAPPING AND PROCESS FEEDBACK INTEGRATION

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.1.1 List of Patents

- 6.4.1 INTRODUCTION

- 6.5 FUTURE APPLICATIONS

- 6.5.1 ON-DEMAND QUALITY ASSURANCE IN HIGH-VOLUME TIRE PRODUCTION

- 6.5.2 FLEET AND SPECIALTY TIRE HEALTH MONITORING

- 6.5.3 AI-ASSISTED PREDICTIVE TIRE FAILURE DETECTION

- 6.6 IMPACT OF AI ON X RAY MACHINE MARKET FOR TIRE INSPECTION

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY X RAY TIRE INSPECTION MACHINE MANUFACTURERS

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN X RAY MACHINE MARKET FOR TIRE INSPECTION

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED X RAY MACHINES FOR TIRE INSPECTION

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS

- 7.2.1 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 7.3.1 X STRUCTURAL ADOPTION CONSTRAINTS AND OPERATIONAL LIMITATIONS

- 7.3.2 DATA GOVERNANCE AND TRACEABILITY INTEGRATION COMPLEXITY

- 7.3.3 STANDARDIZATION LIMITATIONS AND CROSS-PLANT DEPLOYMENT VARIABILITY

- 7.4 UNMET NEEDS OF VARIOUS END USERS/END-USE INDUSTRIES

- 7.4.1 REAL-TIME INLINE INTEGRATION WITH SMART MANUFACTURING SYSTEMS

- 7.4.2 LOWER TOTAL COST OF OWNERSHIP (TCO) AND REDUCED MAINTENANCE DOWNTIME

- 7.4.3 INSPECTION CAPABILITY FOR INCREASINGLY COMPLEX TIRE ARCHITECTURES

8 REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

9 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY SYSTEM TYPE

- 9.1 INTRODUCTION

- 9.2 STATIONARY

- 9.2.1 INLINE

- 9.2.1.1 Increasing stringency of OEM quality benchmarks to drive growth

- 9.2.2 OFFLINE

- 9.2.2.1 Ideal for high-precision and comprehensive defect detection

- 9.2.1 INLINE

- 9.3 MOBILE

- 9.3.1 FLEXIBLE DEPLOYMENT AND LOWER CAPITAL INTENSITY TO DRIVE GROWTH

- 9.4 KEY PRIMARY INSIGHTS

10 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 2D

- 10.2.1 TO DRIVE HIGH-THROUGHPUT AND COST-EFFICIENT TIRE INSPECTION

- 10.3 3D

- 10.3.1 RISING STRUCTURAL COMPLEXITY IN TIRE ARCHITECTURE TO DRIVE ACCELERATED ADOPTION OF 3D CT INSPECTION SYSTEMS

- 10.4 KEY PRIMARY INSIGHTS

11 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY USE CASE

- 11.1 INTRODUCTION

- 11.2 TIER 1

- 11.2.1 HIGH-VOLUME PRODUCTION AND COMPLEX TIRE ARCHITECTURES TO DRIVE GROWTH

- 11.3 OEM

- 11.3.1 RISING OEM LIABILITY AND ZERO-DEFECT MANUFACTURING STANDARDS TO DRIVE GROWTH

- 11.4 AFTERMARKET

- 11.4.1 RETREADING, IMPROVED TIC, AND INSPECTION PROCESSES TO DRIVE AFTERMARKET

- 11.5 KEY PRIMARY INSIGHTS

12 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 TIRE INSPECTION

- 12.3 TREAD INSPECTION

- 12.4 SIDEWALL INSPECTION

- 12.5 BEAD INSPECTION

- 12.6 OTHER / SPECIALTY INSPECTIONS

- 12.7 KEY PRIMARY INSIGHTS

13 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Scaling tire production capacity to drive advanced digital X ray inspection deployment across high-volume manufacturing hubs

- 13.2.2 INDIA

- 13.2.2.1 Radialization growth and export expansion to boost investment in structural X ray tire inspection systems

- 13.2.3 JAPAN

- 13.2.3.1 Premium engineering to drive high-resolution X ray adoption

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Export-driven growth to accelerate advanced X ray adoption

- 13.2.5 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Premium and EV tire engineering to accelerate 3D CT adoption

- 13.3.2 FRANCE

- 13.3.2.1 Export-led manufacturing to drive automated X ray integration

- 13.3.3 ITALY

- 13.3.3.1 Focus on high-performance tire manufacturing to increase precision inspection demand

- 13.3.4 SPAIN

- 13.3.4.1 High-volume production to reinforce 2D system preference

- 13.3.5 UK

- 13.3.5.1 Replacement-driven market structure to sustain cost-focused 2D X ray adoption

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 NORTH AMERICA

- 13.4.1 US

- 13.4.1.1 Liability pressure and zero-defect mandates to drive inline X ray adoption

- 13.4.2 CANADA

- 13.4.2.1 Strict quality compliance and OEM standards to advance X ray inspection

- 13.4.3 MEXICO

- 13.4.3.1 Export-driven radial tire capacity expansion to accelerate inline X ray inspection system deployment

- 13.4.1 US

- 13.5 REST OF THE WORLD

- 13.5.1 UAE

- 13.5.1.1 Technology upgrades and high vehicle ownership base to drive market

- 13.5.2 SAUDI ARABIA

- 13.5.2.1 Localization-led growth to drive advanced tire inspection systems

- 13.5.1 UAE

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 MARKET RANKING ANALYSIS FOR KEY PLAYERS, 2025

- 14.4 REVENUE ANALYSIS OF KEY PLAYERS, 2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Technology footprint

- 14.7.5.4 System type footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES/DEVELOPMENTS/ENHANCEMENTS

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 AMETEK MICRO-POISE

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 TECHNIP ENERGIES N.V.

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 COMET

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 MESNAC

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.3.2 Expansions

- 15.1.4.3.3 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 NIKON CORPORATION INDUSTRIAL SOLUTIONS

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches/enhancements

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 X-SCAN

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product developments

- 15.1.7 TMSI

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.3.2 Other developments

- 15.1.8 HAMAMATSU PHOTONICS K.K.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.3.2 Expansions

- 15.1.9 BLUE STAR ENGINEERING & ELECTRONICS LTD.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.10 ALFAMATION

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.11 PARTH SYSTEMS INDIA PVT. LTD.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 DETECTION TECHNOLOGY PLC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches/enhancements

- 15.1.12.3.2 Expansions

- 15.1.1 AMETEK MICRO-POISE

- 15.2 OTHER PLAYERS

- 15.2.1 NORTH STAR IMAGING INC.

- 15.2.2 METRIX NDT

- 15.2.3 TEKNA AUTOMAZIONE

- 15.2.4 DANDONG AOLONG RADIATIVE INSTRUMENT GROUP CO., LTD.

- 15.2.5 ZEISS GROUP

- 15.2.6 BAKER HUGHES COMPANY

- 15.2.7 HAVEN METROLOGY, INC.

- 15.2.8 MQS TECHNOLOGIES PRIVATE LIMITED

- 15.2.9 CONTINENTAL AG

- 15.2.10 RX SOLUTIONS SAS

- 15.2.11 GL INSPECTION SYSTEMS GMBH

- 15.2.12 TOSHIBA INFRASTRUCTURE SYSTEMS AND SOLUTIONS CORPORATION

- 15.2.13 RAYSOV INSPECTION TECHNOLOGY CO., LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.2 KEY SECONDARY SOURCES

- 16.1.2.1 List of secondary sources

- 16.1.2.2 Key data from secondary sources

- 16.1.3 PRIMARY DATA

- 16.1.3.1 Primary interviews - demand and supply sides

- 16.1.3.2 Key industry insights and breakdown of primary interviews

- 16.1.3.3 List of primary participants

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 FACTOR ANALYSIS

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 KEY INSIGHTS FROM INDUSTRY EXPERTS

- 17.2 DISCUSSION GUIDE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS

List of Tables

- TABLE 1 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY SYSTEM TYPE

- TABLE 2 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- TABLE 3 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY USE CASE

- TABLE 4 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY APPLICATION

- TABLE 5 INCLUSIONS AND EXCLUSIONS

- TABLE 6 CURRENCY EXCHANGE RATES, 2020-2025

- TABLE 7 COMPARATIVE ASSESSMENT: 2D VS. 3D X RAY IMAGING IN TIRE INSPECTION

- TABLE 8 X RAY MACHINE MARKET FOR TIRE INSPECTION: IMPACT OF MARKET DYNAMICS

- TABLE 9 STRATEGIC MOVES BY KEY PLAYERS OPERATING IN X RAY MACHINE FOR TIRE INSPECTION ECOSYSTEM

- TABLE 10 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 11 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 12 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, 2026 (USD MILLION)

- TABLE 13 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY, 2024-2026 (USD MILLION)

- TABLE 14 AVERAGE SELLING PRICE TREND, BY REGION, 2024-2026 (USD MILLION)

- TABLE 15 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 16 IMPORT DATA FOR HS CODE 902219-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD BILLION)

- TABLE 17 EXPORT DATA FOR HS CODE 902219-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD BILLION)

- TABLE 18 X RAY MACHINE COMPARISON BY KEY PLAYERS FOR TIRE INSPECTION

- TABLE 19 IMPORTANT PATENT REGISTRATIONS RELATED TO X RAY MACHINE MARKET FOR TIRE INSPECTION, 2022-2025

- TABLE 20 AI-DRIVEN BEST PRACTICES FOLLOWED BY MANUFACTURERS AND OEMS IN X RAY MACHINE MARKET FOR TIRE INSPECTION

- TABLE 21 AI-DRIVEN STATISTICAL DEFECT MAPPING FOR PROCESS OPTIMIZATION

- TABLE 22 AI-ENABLED INLINE DEFECT RECOGNITION FOR HIGH-VOLUME TIRE PRODUCTION

- TABLE 23 IMPACT OF ECOSYSTEM COMPONENTS ON X RAY MACHINE MARKET FOR TIRE INSPECTION

- TABLE 24 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- TABLE 25 KEY BUYING CRITERIA FOR X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- TABLE 26 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 28 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 29 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 30 INTERNATIONAL STANDARDS

- TABLE 31 NORTH AMERICA: STANDARDS

- TABLE 32 EUROPE: STANDARDS

- TABLE 33 ASIA PACIFIC: STANDARDS

- TABLE 34 REST OF THE WORLD: STANDARDS

- TABLE 35 POLICY INITIATIVES AFFECTING SUSTAINABILITY, SAFETY, PRIVACY, AND TECHNOLOGY COMPLIANCE FOR X RAY MACHINE MARKET FOR TIRE INSPECTION

- TABLE 36 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY SYSTEM TYPE, 2021-2024 (USD MILLION)

- TABLE 37 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY SYSTEM TYPE, 2025-2032 (USD MILLION)

- TABLE 38 STATIONARY X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 39 STATIONARY X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 40 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY STATIONARY SYSTEM TYPE, 2021-2024 (USD MILLION)

- TABLE 41 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY STATIONARY SYSTEM TYPE, 2025-2032 (USD MILLION)

- TABLE 42 INLINE X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 43 INLINE X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 44 OFFLINE X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 45 OFFLINE X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 46 MOBILE X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 47 MOBILE X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 48 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 49 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 50 2D X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 51 2D X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 52 3D X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 53 3D X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 54 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY USE CASE, 2021-2024 (USD MILLION)

- TABLE 55 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY USE CASE, 2025-2032 (USD MILLION)

- TABLE 56 TIER 1 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 57 TIER 1 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 58 OEM X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 59 OEM X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 60 AFTERMARKET X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 61 AFTERMARKET X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 62 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2021-2024 (USD MILLION)

- TABLE 63 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025-2032 (USD MILLION)

- TABLE 64 ASIA PACIFIC: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 65 ASIA PACIFIC: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 66 CHINA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 67 CHINA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 68 INDIA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 69 INDIA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 70 JAPAN: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 71 JAPAN: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 72 SOUTH KOREA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 73 SOUTH KOREA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 74 REST OF ASIA PACIFIC: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 75 REST OF ASIA PACIFIC: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 76 EUROPE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 77 EUROPE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 78 GERMANY: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 79 GERMANY: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 80 FRANCE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 81 FRANCE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 82 ITALY: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 83 ITALY: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 84 SPAIN: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 85 SPAIN: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 86 UK: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 87 UK: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 88 REST OF EUROPE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 89 REST OF EUROPE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 90 NORTH AMERICA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 91 NORTH AMERICA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 92 US: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 93 US: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 94 CANADA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 95 CANADA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 96 MEXICO: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 97 MEXICO: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 98 REST OF THE WORLD: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 99 REST OF THE WORLD: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2025-2032(USD MILLION)

- TABLE 100 UAE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 101 UAE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 102 SAUDI ARABIA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 103 SAUDI ARABIA: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032 (USD MILLION)

- TABLE 104 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2025

- TABLE 105 MARKET SHARE ANALYSIS, 2024

- TABLE 106 X RAY MACHINE MARKET FOR TIRE INSPECTION: REGION FOOTPRINT, 2025

- TABLE 107 X RAY MACHINE MARKET FOR TIRE INSPECTION: BY TECHNOLOGY FOOTPRINT, 2025

- TABLE 108 X RAY MACHINE MARKET FOR TIRE INSPECTION: SYSTEM TYPE FOOTPRINT, 2025

- TABLE 109 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 110 X RAY MACHINE MARKET FOR TIRE INSPECTION: PRODUCT LAUNCHES/ DEVELOPMENTS/ENHANCEMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 111 X RAY MACHINE MARKET FOR TIRE INSPECTION: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 112 X RAY MACHINE MARKET FOR TIRE INSPECTION: EXPANSIONS, JANUARY 2021-DECEMBER 2025

- TABLE 113 X RAY MACHINE MARKET FOR TIRE INSPECTION: OTHER DEVELOPMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 114 AMETEK MICRO-POISE: COMPANY OVERVIEW

- TABLE 115 AMETEK MICRO-POISE: PRODUCTS OFFERED

- TABLE 116 AMETEK MICRO-POISE: EXPANSIONS

- TABLE 117 TECHNIP ENERGIES N.V.: COMPANY OVERVIEW

- TABLE 118 TECHNIP ENERGIES N.V.: PRODUCTS OFFERED

- TABLE 119 TECHNIP ENERGIES N.V.: DEALS

- TABLE 120 COMET: COMPANY OVERVIEW

- TABLE 121 COMET: PRODUCTS OFFERED

- TABLE 122 COMET: EXPANSIONS

- TABLE 123 MESNAC: COMPANY OVERVIEW

- TABLE 124 MESNAC: PRODUCTS OFFERED

- TABLE 125 MESNAC: DEALS

- TABLE 126 MESNAC: EXPANSIONS

- TABLE 127 MESNAC: OTHER DEVELOPMENTS

- TABLE 128 NIKON CORPORATION INDUSTRIAL SOLUTIONS: COMPANY OVERVIEW

- TABLE 129 NIKON CORPORATION INDUSTRIAL SOLUTIONS: PRODUCTS OFFERED

- TABLE 130 NIKON CORPORATION INDUSTRIAL SOLUTIONS: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 131 NIKON CORPORATION INDUSTRIAL SOLUTIONS: DEALS

- TABLE 132 X-SCAN: COMPANY OVERVIEW

- TABLE 133 X-SCAN: PRODUCTS OFFERED

- TABLE 134 X-SCAN: PRODUCT DEVELOPMENTS

- TABLE 135 TMSI: COMPANY OVERVIEW

- TABLE 136 TMSI: PRODUCTS OFFERED

- TABLE 137 TMSI: DEALS

- TABLE 138 TMSI: OTHER DEVELOPMENTS

- TABLE 139 HAMAMATSU PHOTONICS K.K.: COMPANY OVERVIEW

- TABLE 140 HAMAMATSU PHOTONICS K.K.: PRODUCTS OFFERED

- TABLE 141 HAMAMATSU PHOTONICS K.K.: DEALS

- TABLE 142 HAMAMATSU PHOTONICS K.K.: EXPANSIONS

- TABLE 143 BLUE STAR ENGINEERING & ELECTRONICS LTD.: COMPANY OVERVIEW

- TABLE 144 BLUE STAR ENGINEERING & ELECTRONICS LTD.: PRODUCTS OFFERED

- TABLE 145 BLUE STAR ENGINEERING & ELECTRONICS LTD.: DEALS

- TABLE 146 BLUE STAR ENGINEERING & ELECTRONICS LTD.: EXPANSIONS

- TABLE 147 ALFAMATION: COMPANY OVERVIEW

- TABLE 148 ALFAMATION: PRODUCTS OFFERED

- TABLE 149 PARTH SYSTEMS INDIA PVT. LTD.: COMPANY OVERVIEW

- TABLE 150 PARTH SYSTEMS INDIA PVT. LTD.: PRODUCTS OFFERED

- TABLE 151 DETECTION TECHNOLOGY PLC.: COMPANY OVERVIEW

- TABLE 152 DETECTION TECHNOLOGY PLC.: PRODUCTS OFFERED

- TABLE 153 DETECTION TECHNOLOGY PLC.: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 154 DETECTION TECHNOLOGY PLC: EXPANSIONS

- TABLE 155 NORTH STAR IMAGING INC.: COMPANY OVERVIEW

- TABLE 156 METRIX NDT: COMPANY OVERVIEW

- TABLE 157 TEKNA AUTOMAZIONE: COMPANY OVERVIEW

- TABLE 158 DANDONG AOLONG RADIATIVE INSTRUMENT GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 159 ZEISS GROUP: COMPANY OVERVIEW

- TABLE 160 BAKER HUGHES COMPANY: COMPANY OVERVIEW

- TABLE 161 HAVEN METROLOGY, INC.: COMPANY OVERVIEW

- TABLE 162 MQS TECHNOLOGIES PRIVATE LIMITED: COMPANY OVERVIEW

- TABLE 163 CONTINENTAL AG: COMPANY OVERVIEW

- TABLE 164 RX SOLUTIONS SAS: COMPANY OVERVIEW

- TABLE 165 GL INSPECTION SYSTEMS GMBH: COMPANY OVERVIEW

- TABLE 166 TOSHIBA INFRASTRUCTURE SYSTEMS AND SOLUTIONS CORPORATION: COMPANY OVERVIEW

- TABLE 167 RAYSOV INSPECTION TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 X RAY MACHINE MARKET FOR TIRE INSPECTION SEGMENTATION AND REGIONAL SNAPSHOT

- FIGURE 2 MARKET SCENARIO

- FIGURE 3 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025-2032

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN X RAY MACHINE MARKET FOR TIRE INSPECTION, 2021-2025

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF X RAY MACHINE MARKET FOR TIRE INSPECTION

- FIGURE 6 HIGH-GROWTH SEGMENTS IN X RAY MACHINE MARKET FOR TIRE INSPECTION, 2025-2032

- FIGURE 7 ASIA PACIFIC TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 8 ZERO-DEFECT MANDATES AND SAFETY REGULATIONS TO DRIVE MARKET

- FIGURE 9 STATIONARY X RAY SYSTEMS TO BE DOMINANT SEGMENT IN 2032

- FIGURE 10 2D X RAY TO BE DOMINANT TECHNOLOGY SEGMENT IN 2032

- FIGURE 11 TIER 1 TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 12 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2025

- FIGURE 13 X RAY MACHINE MARKET FOR TIRE INSPECTION: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 14 GLOBAL VEHICLES OPERATING ON ROAD

- FIGURE 15 ECOSYSTEM ANALYSIS OF X RAY MACHINE MARKET FOR TIRE INSPECTION

- FIGURE 16 SUPPLY CHAIN ANALYSIS OF X RAY MACHINE MARKET FOR TIRE INSPECTION

- FIGURE 17 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY, 2024-2026 (USD MILLION)

- FIGURE 18 AVERAGE SELLING PRICE TREND, BY REGION, 2024-2026 (USD MILLION)

- FIGURE 19 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 20 INVESTMENT AND FUNDING SCENARIO, 2023-2026 (USD MILLION)

- FIGURE 21 IMPORT DATA FOR HS CODE 902219-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD BILLION)

- FIGURE 22 EXPORT DATA FOR HS CODE 902219-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD BILLION)

- FIGURE 23 TARIFF LIBERALIZATION DRIVES DEEPER INDIA-EU INDUSTRIAL INTEGRATION

- FIGURE 24 LOWER VEHICLE IMPORT DUTIES INTENSIFY COMPETITION IN INDIAN AUTOMOTIVE MARKET

- FIGURE 25 REDUCED INPUT TARIFFS STRENGTHEN AUTOMOTIVE SUPPLY CHAIN COMPETITIVENESS

- FIGURE 26 FTA MARKET ACCESS EXPANDS TWO-WAY AUTOMOTIVE TRADE AND COMPONENT EXPORTS

- FIGURE 27 X RAY MACHINE MARKET FOR TIRE INSPECTION PRODUCT ROADMAP

- FIGURE 28 PATENT ANALYSIS, 2016-2026

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- FIGURE 30 KEY BUYING CRITERIA FOR X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY

- FIGURE 31 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY SYSTEM TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 32 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY TECHNOLOGY, 2025 VS. 2032 (USD MILLION)

- FIGURE 33 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY USE CASE, 2025 VS. 2032 (USD MILLION)

- FIGURE 34 TIRE DEFECT INSPECTION AREAS

- FIGURE 35 X RAY MACHINE MARKET FOR TIRE INSPECTION, BY REGION, 2025 VS. 2032 (USD MILLION)

- FIGURE 36 ASIA PACIFIC: X RAY MACHINE MARKET FOR TIRE INSPECTION SNAPSHOT

- FIGURE 37 EUROPE: X RAY MACHINE MARKET FOR TIRE INSPECTION, BY COUNTRY, 2025-2032 (USD MILLION)

- FIGURE 38 NORTH AMERICA: X RAY MACHINE MARKET FOR TIRE INSPECTION SNAPSHOT

- FIGURE 39 REST OF THE WORLD: X-RAY MACHINE MARKET FOR TIRE INSPECTION SNAPSHOT

- FIGURE 40 MARKET SHARE ANALYSIS OF TOP 5 PLAYERS, 2025

- FIGURE 41 REVENUE ANALYSIS OF KEY PLAYERS, 2021-2025 (USD BILLION)

- FIGURE 42 COMPANY VALUATION OF KEY PLAYERS, 2025 (USD BILLION)

- FIGURE 43 FINANCIAL METRICS OF KEY PLAYERS, 2025

- FIGURE 44 BRAND/PRODUCT COMPARISON

- FIGURE 45 X RAY MACHINE MARKET FOR TIRE INSPECTION: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 46 X RAY MACHINE MARKET FOR TIRE INSPECTION: COMPANY FOOTPRINT, 2025

- FIGURE 47 X RAY MACHINE MARKET FOR TIRE INSPECTION: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 48 AMETEK MICRO-POISE: COMPANY SNAPSHOT

- FIGURE 49 TECHNIP ENERGIES N.V.: COMPANY SNAPSHOT

- FIGURE 50 COMET: COMPANY SNAPSHOT

- FIGURE 51 MESNAC: COMPANY SNAPSHOT

- FIGURE 52 NIKON CORPORATION INDUSTRIAL SOLUTIONS: COMPANY SNAPSHOT

- FIGURE 53 HAMAMATSU PHOTONICS K.K.: COMPANY SNAPSHOT

- FIGURE 54 BLUE STAR ENGINEERING & ELECTRONICS LTD.: COMPANY SNAPSHOT

- FIGURE 55 ALFAMATION: COMPANY SNAPSHOT

- FIGURE 56 X RAY MACHINE MARKET FOR TIRE INSPECTION: RESEARCH DESIGN

- FIGURE 57 RESEARCH DESIGN MODEL

- FIGURE 58 KEY INDUSTRY INSIGHTS

- FIGURE 59 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 60 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 61 TOP-DOWN APPROACH

- FIGURE 62 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 63 MARKET GROWTH PROJECTIONS FROM SUPPLY-SIDE DRIVERS AND OPPORTUNITIES