PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2003240

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2003240

Patient Engagement Solutions Market by Therapy, Functionality, End User, Unmet Need, Investment, Market Share, and Trends - Global Forecast to 2030

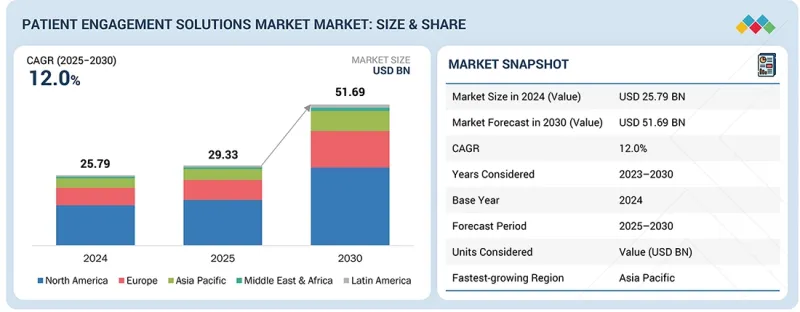

The patient engagement solutions market is projected to reach USD 51.69 billion by 2030 from USD 29.33 billion in 2025, at a CAGR of 12.0% during the forecast period. Factors such as the rising use of digital solutions that allow real-time communication, personalized interaction, and easy interfacing.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Component, Delivery Mode, Therapeutic Area, Application, Functionality, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America and Middle East & Africa |

Others may include advancements such as cloud solutions, mobile solutions, and analytics. High investment requirements for healthcare infrastructure and a lack of skilled IT professionals in the healthcare sector are anticipated to impede the growth of this market .

"Services segment is expected to grow at the highest rate during the forecast period."

By components, the patient engagement solutions market is divided into software, hardware, and services. The services segment is expected to grow at the fastest rate as healthcare organizations increasingly seek support for implementation, customization, integration with EHRs, change management, training, and ongoing optimization of engagement technologies. These professional and managed services help providers and payers maximize the value of engagement platforms, adapt to evolving clinical workflows, and ensure seamless deployment across complex healthcare environments .

"The on-premise segment is anticipated to dominate the Patient Engagement Solutions market in 2024"

By delivery modes, the patient engagement solutions market is categorized into on-premise and cloud-based/web-based modes. In 2024, the on-premise segment is expected to dominate because many healthcare organizations, especially large hospitals and health systems, prefer to maintain direct control over sensitive patient data and core clinical systems. On-premise deployments also align with established IT infrastructures, existing EHR environments, and stringent security and compliance requirements, making them a dominant choice for organizations prioritizing data governance and internal integration .

"Health management segment accounted for the largest share of the global patient engagement solutions market, by applications"

By application, the patient engagement solutions market is divided into health management, home health management, social and behavioral management, and financial health management. In 2024, the health management applications segment accounts held the largest share of the global patient engagement solutions market. It encompasses comprehensive care coordination, chronic disease management, and population health initiatives that rely heavily on engagement tools to maintain continuous patient communication. These solutions help providers and payers monitor patient outcomes, close care gaps, and support preventive care, making health management the dominant application driving adoption of engagement platforms .

"Providers' segment accounted for the largest share of the global patient engagement solutions market, by end user in 2024."

By end users, the patient engagement solutions market is divided into providers, payers, patients, and other end users. The providers are further bifurcated into hospitals and healthcare system, ambulatory care centers, home healthcare, and other providers. Moreover the payers is further divided into private and public. By end users, the providers' segment accounted for the largest share of the global patient engagement solutions market in 2024. The large share of this segment is due to increasing implementation of patient engagement solutions to curtail mounting healthcare costs, offer value-based care, and expand financial outcomes are factors that are driving the growth of this segment.

"North America to dominate the patient engagement solutions market

In 2024, North America dominated the global patient engagement solutions market by region. Factors such as favorable government initiatives and regulations, the imperative to reduce healthcare costs, the increasing prevalence of chronic diseases, and the presence of key market players contribute significantly to the growth of the patient engagement solutions market in North America. Strong regulatory frameworks promoting patient access, data interoperability, and value-based care, along with the presence of leading healthcare IT vendors and high healthcare spending, continue to drive market leadership in the region .

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (45%), Tier 2 (30%), and Tier 3 (25%)

- By Designation: C-level (44%), Director-level (35%), and Others (21%)

- By Region: North America (46%), Europe (26%), Asia Pacific (18%), Latin America (7%), and Middle East & Africa (10%)

McKesson Corporation (US), Veradigm LLC (US), Oracle (US), athenahealth (US), Health Catalyst (US), GetWellNetwork, Inc. (US), Lincata, Inc. (US), Cognizant (US), TruBridge (US), Oneview Healthcare (Ireland), AdvancedMD, Inc. (US), Epic Systems Corporation (US), Harris Healthcare (US), Medical Information Technology, Inc. (US), Tebra Technologies, Inc. (US), Televox (US), Medhost (US), Nuance Communications, Inc. (US) (Microsoft), Solutionreach, Inc. (US), Experian Information Solutions, Inc. (US). These players are increasingly focusing on new product launches and partnerships to expand their product offerings in the patient engagement solutions market.

Research Coverage

- The report studies the Patient Engagement Solutions market based on component, delivery mode, therapeutic area, application, functionality, end user, and region.

- The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

- The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

- The report studies micro-markets with respect to their growth trends, prospects, and contributions to the total patient engagement solutions market.

- The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

- This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the below-mentioned strategies to strengthen their positions in the market.

- Analysis of key drivers (implementation of government regulations and initiatives to promote patient centric care, increasing adoption of patient engagement solutions, rising number of collaborations and partnerships between stakeholders, increasing utilisation of mobile health apps, rising geriatric population and subsequent increase in prevalence of chronic diseases), restraints (large investment requirement for healthcare infrastructure, protection of patient information, inadequate interoperability across healthcare providers and shortage of skilled IT professionals in the healthcare industry ), opportunities (growth opportunities in emerging markets, wearable health technology, cloud computing solutions), and challenges (high deployment cost of healthcare IT systems, low levels of healthcare literacy) impacting the growth of the patient engagement solutions market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the patient engagement solutions market.

- Market Development: Comprehensive information on the lucrative emerging markets, component, delivery mode, therapeutic area, application, functionality, end user, and region

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the patient engagement solutions market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, company evaluation quadrant, and capabilities of leading players in the global patient engagement market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PATIENT ENGAGEMENT SOLUTIONS MARKET OVERVIEW

- 3.2 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE AND REGION

- 3.3 PATIENT ENGAGEMENT SOLUTIONS MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing adoption of telehealth and remote care

- 4.2.1.2 Increasing smartphone use and digital comfort

- 4.2.1.3 Implementation of government regulations and initiatives to promote patient-centric care

- 4.2.1.4 Growing prevalence of chronic diseases and rising demand for long-term patient involvement

- 4.2.2 RESTRAINTS

- 4.2.2.1 Data privacy and cybersecurity concerns

- 4.2.2.2 Inadequate interoperability across healthcare providers

- 4.2.2.3 Shortage of skilled IT professionals in healthcare industry

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of remote and home-based care models

- 4.2.3.2 AI-driven personalization in patient engagement solutions

- 4.2.3.3 Integration with wearables and personalized health tech

- 4.2.4 CHALLENGES

- 4.2.4.1 Low patient adoption and engagement over time

- 4.2.4.2 Fragmented data and siloed digital tools

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 ROLE IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR PATIENT ENGAGEMENT SOLUTIONS, BY COMPONENT, 2025

- 5.5.2 INDICATIVE PRICE FOR PATIENT ENGAGEMENT SOLUTIONS, BY REGION, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO FOR HS CODE 8528, 2021-2024

- 5.6.2 IMPORT SCENARIO FOR HS CODE 8471, 2021-2024

- 5.6.3 EXPORT SCENARIO FOR HS CODE 8528, 2021-2024

- 5.6.4 EXPORT SCENARIO FOR HS CODE 8471, 2021-2024

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ACHIEVING USD 15 MILLION IN SAVINGS BY REDUCING READMISSIONS WITH POST-DISCHARGE FOLLOW-UP

- 5.10.2 BUILD TRUST THROUGH PATIENT ENGAGEMENT TECHNOLOGY: CHILDREN'S HOSPITAL CASE STUDY

- 5.10.3 IMPROVING PATIENT ENGAGEMENT AT SPARTA COMMUNITY HOSPITAL WITH TRUBRIDGE PATIENT CONNECT

- 5.11 IMPACT OF 2025 US TARIFF ON PATIENT ENGAGEMENT SOLUTIONS MARKET

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRY/REGION

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END-USE INDUSTRIES

- 5.11.4.1 Hospitals and healthcare systems

- 5.11.4.2 ASCs, ACCs, and other outpatient settings

- 5.11.4.3 Home healthcare providers

- 5.11.4.4 Private payers

- 5.11.4.5 Public payers

- 5.11.4.6 Other end users

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 CLOUD COMPUTING

- 6.1.2 API & EHR INTEGRATION TECHNOLOGIES

- 6.1.3 DATA ANALYTICS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ARTIFICIAL INTELLIGENCE (AI) AND MACHINE LEARNING (ML)

- 6.2.2 CONVERSATIONAL AI/CHATBOTS

- 6.2.3 BEHAVIORAL ANALYTICS AND PERSONALIZATION ENGINES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CYBERSECURITY AND DATA ENCRYPTION

- 6.3.2 BLOCKCHAIN

- 6.3.3 BIG DATA AND ADVANCED ANALYTICS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR PATIENT ENGAGEMENT SOLUTION

- 6.5.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5.3 LIST OF PATENTS/PATENT APPLICATIONS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE ENGAGEMENT

- 6.6.2 CONTINUOUS REMOTE CARE AND HOSPITAL-AT-HOME ENABLEMENT

- 6.6.3 PERSONALIZED DIGITAL THERAPEUTICS AND BEHAVIORAL COACHING

- 6.6.4 CLOSED-LOOP CARE COORDINATION AND VALUE-BASED PERFORMANCE OPTIMIZATION

- 6.6.5 DECENTRALIZED CLINICAL TRIALS AND REAL-WORLD EVIDENCE GENERATION

- 6.7 IMPACT OF AI/GEN AI ON PATIENT ENGAGEMENT SOLUTIONS MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 AI-driven conversational AI for pre/post-op engagement

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.4.1 Patient communication & virtual care platforms

- 6.7.4.2 Remote patient monitoring & digital therapeutics

- 6.7.4.3 Population health & health equity programs

- 6.7.5 USER READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.1.1 User A: Hospitals & clinics

- 6.7.5.1.2 User B: Healthcare providers, employers, and forensic agencies

- 6.7.5.2 Impact assessment

- 6.7.5.2.1 User A: Clinical, reference, and toxicology laboratories

- 6.7.5.2.2 User B: Healthcare providers, employers, and forensic agencies

- 6.7.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS/END-USER EXPECTATIONS

- 8.5.1 UNMET NEEDS

- 8.5.2 END-USER EXPECTATIONS

- 8.6 MARKET PROFITIBILITY

9 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 HARDWARE

- 9.2.1 IN-ROOM TELEVISIONS

- 9.2.1.1 Rising patient demand for real-time health transparency and smart room modernization initiatives to drive market

- 9.2.2 INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES

- 9.2.2.1 Hospitals to increasingly adopt bedside terminals to address workforce shortages and reduce nursing workload

- 9.2.3 TABLETS

- 9.2.3.1 Strong ROI profile, lower upfront investment, and rapid rollout capability to propel market growth

- 9.2.1 IN-ROOM TELEVISIONS

- 9.3 SOFTWARE

- 9.3.1 PRE-CARE ENGAGEMENT

- 9.3.1.1 Increasing adoption of consumer-centric access models to aid segment growth

- 9.3.2 POINT-OF-CARE ENGAGEMENT

- 9.3.2.1 Exponential growth in healthcare data and rising information complexity to augment segment growth

- 9.3.3 POST-CARE ENGAGEMENT

- 9.3.3.1 Shift toward value-based care and reimbursement models for readmission rates to drive segment growth

- 9.3.1 PRE-CARE ENGAGEMENT

- 9.4 SERVICES

- 9.4.1 IMPLEMENTATION & INTEGRATION SERVICES

- 9.4.1.1 Need for expertise to operationalize sophisticated patient engagement ecosystems to fuel market growth

- 9.4.2 TRAINING & EDUCATION SERVICES

- 9.4.2.1 Need to eradicate measurable staff usability challenges and patient digital access gaps to drive segment

- 9.4.3 SUPPORT & MAINTENANCE SERVICES

- 9.4.3.1 Dependency on patient portals, telehealth systems, and integrated EHR infrastructures to aid market growth

- 9.4.4 CONSULTING SERVICES

- 9.4.4.1 Shift from volume-based to value-based care models to drive consulting services market

- 9.4.1 IMPLEMENTATION & INTEGRATION SERVICES

10 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE

- 10.1 INTRODUCTION

- 10.2 ON-PREMISES

- 10.2.1 ON-PREMISES ADOPTION TO ACCELERATE AMID SECURITY, REGULATORY, AND INTEGRATION PRIORITIES

- 10.3 CLOUD-BASED

- 10.3.1 CLOUD-BASED PATIENT ENGAGEMENT TO PROPEL SCALABLE, SECURE, AND INTEROPERABLE CARE

11 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 CLINICAL CARE

- 11.2.1 VALUE-BASED CARE MODELS AND TELEHEALTH EXPANSION TO PROPEL CLINICAL CARE SEGMENT

- 11.3 CARE COORDINATION & COMMUNICATION

- 11.3.1 FRAGMENTED CARE PATHWAYS AND INTEROPERABILITY MANDATES TO ACCELERATE MARKET GROWTH

- 11.4 HOME & REMOTE CARE

- 11.4.1 HOSPITAL-AT-HOME EXPANSION, READMISSION PENALTIES, AND RPM REIMBURSEMENT TO FUEL SEGMENT GROWTH

- 11.5 POPULATION HEALTH & BEHAVIORAL ENGAGEMENT

- 11.5.1 VALUE-BASED CARE MANDATES, RISK STRATIFICATION, AND BEHAVIORAL HEALTH INTEGRATION TO PROPEL SEGMENT GROWTH

- 11.6 FINANCIAL ENGAGEMENT

- 11.6.1 RISING OUT-OF-POCKET COSTS, CONSUMERISM, AND REVENUE PRESSURE TO DRIVE FINANCIAL ENGAGEMENT ADOPTION

- 11.7 OTHER APPLICATIONS

12 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA

- 12.1 INTRODUCTION

- 12.2 CHRONIC DISEASES

- 12.2.1 CARDIOVASCULAR DISEASES

- 12.2.1.1 Need for continuous monitoring and preventive engagement through digital health platforms to drive market

- 12.2.2 DIABETES

- 12.2.2.1 Continuous glucose monitoring, behavioral adherence, and data-driven self-management through digital engagement to drive market

- 12.2.3 OBESITY

- 12.2.3.1 Preventive engagement, behavioral modification, and long-term risk reduction through digital health platforms to drive market

- 12.2.4 RESPIRATORY DISORDERS

- 12.2.4.1 Advancing continuous symptom monitoring and preventive care through digital engagement platforms to fuel market growth

- 12.2.5 ONCOLOGY

- 12.2.5.1 Longitudinal care coordination, symptom monitoring, and survivorship engagement to boost market

- 12.2.6 OTHER CHRONIC DISEASES

- 12.2.1 CARDIOVASCULAR DISEASES

- 12.3 WOMEN'S HEALTH

- 12.3.1 PREVENTIVE SCREENING, REPRODUCTIVE CARE COORDINATION, AND LIFECYCLE ENGAGEMENT TO AID MARKET GROWTH

- 12.4 BEHAVIORAL & MENTAL HEALTH

- 12.4.1 INCREASING GLOBAL PREVALENCE OF DEPRESSION, ANXIETY, SUBSTANCE USE DISORDERS TO AID MARKET GROWTH

- 12.5 OTHER THERAPEUTIC AREAS

13 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY

- 13.1 INTRODUCTION

- 13.2 PATIENT/CLIENT SCHEDULING

- 13.2.1 DIGITAL-FIRST, MOBILE-DRIVEN SCHEDULING TO REDUCE NO-SHOWS AND STRENGTHEN ACCESS PERFORMANCE

- 13.3 TELEHEALTH

- 13.3.1 TELEHEALTH TO DRIVE QUALITY IMPROVEMENT AND HYBRID CARE DELIVERY GROWTH

- 13.4 E-PRESCRIBING

- 13.4.1 E-PRESCRIBING TO STRENGTHEN MEDICATION SAFETY REGULATORY COMPLIANCE

- 13.5 DOCUMENT MANAGEMENT

- 13.5.1 DIGITAL RECORD ACCESS TO DRIVE DOCUMENT MANAGEMENT IN CORE PATIENT ENGAGEMENT INFRASTRUCTURE

- 13.6 BILLING & PAYMENTS

- 13.6.1 RISING PATIENT FINANCIAL RESPONSIBILITY AND GROWING DEMAND FOR DIGITAL TRANSPARENCY TO DRIVE MARKET

- 13.7 PATIENT EDUCATION

- 13.7.1 SELF-DIRECTED HEALTH RESEARCH AND DIGITAL LITERACY GAPS TO RISE DEMAND FOR INTEGRATED PATIENT EDUCATION TOOLS

- 13.8 OTHER FUNCTIONALITIES

14 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 PROVIDERS

- 14.2.1 HOSPITALS & HEALTHCARE SYSTEMS

- 14.2.1.1 Healthcare systems to drive patient experience and operational efficiency through integrated patient engagement solutions

- 14.2.2 ASCS, ACCS, AND OTHER OUTPATIENT SETTINGS

- 14.2.2.1 Need for optimizing patient access and engagement in outpatient care settings to propel segment growth

- 14.2.3 HOME HEALTHCARE PROVIDERS

- 14.2.3.1 Home healthcare provides to enhance patient engagement and remote care delivery in home settings

- 14.2.4 OTHER PROVIDERS

- 14.2.1 HOSPITALS & HEALTHCARE SYSTEMS

- 14.3 PAYERS

- 14.3.1 PRIVATE PAYERS

- 14.3.1.1 Private payers to enhance member experience and cost efficiency through digital-first engagement strategies

- 14.3.2 PUBLIC PAYERS

- 14.3.2.1 Public payers to strengthen population health management through inclusive and scalable digital engagement

- 14.3.1 PRIVATE PAYERS

- 14.4 OTHER END USERS

15 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 Value-based care reforms and long-term care management need to accelerate market growth

- 15.2.3 CANADA

- 15.2.3.1 Government policies to strengthen digital health infrastructure and interoperability

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 GERMANY

- 15.3.2.1 Nationwide ePA rollout and digital therapeutics leadership to propel market growth

- 15.3.3 FRANCE

- 15.3.3.1 Near-universal digital health record adoption and strategic investment to aid market growth

- 15.3.4 UK

- 15.3.4.1 NHS app scale-up and virtual care expansion to boost market growth

- 15.3.5 ITALY

- 15.3.5.1 Rising digital health investment and growing focus on national telemedicine infrastructure to fuel market growth

- 15.3.6 SPAIN

- 15.3.6.1 Rising telemedicine expansion and growing mHealth adoption to strengthen market

- 15.3.7 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 CHINA

- 15.4.2.1 High digital health adoption and internet hospital expansion to accelerate market growth

- 15.4.3 JAPAN

- 15.4.3.1 Healthcare digitalization to accelerate patient engagement in Japan

- 15.4.4 INDIA

- 15.4.4.1 Digital public health infrastructure and mobile penetration to augment market growth

- 15.4.5 SOUTH KOREA

- 15.4.5.1 National digital integration and rapid population aging to aid market growth

- 15.4.6 AUSTRALIA

- 15.4.6.1 Near-universal digital records and embedded telehealth adoption to fuel market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 15.5.2 BRAZIL

- 15.5.2.1 Government-led telehealth scale and institutionalized patient participation to propel digital engagement

- 15.5.3 MEXICO

- 15.5.3.1 Structural health system gaps to spur digital patient engagement adoption

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 15.6.2 GCC COUNTRIES

- 15.6.2.1 High NCD burden and government-owned digital platforms to augment patient engagement

- 15.6.2.2 Kingdom of Saudi Arabia

- 15.6.2.2.1 Government-led digital health innovations to accelerate patient engagement

- 15.6.2.3 UAE

- 15.6.2.3.1 Progressive digital health innovations to strengthen UAE patient engagement solutions market

- 15.6.2.4 Rest of GCC countries

- 15.6.3 SOUTH AFRICA

- 15.6.3.1 Massive telemedicine adoption and innovative digital platforms to aid market growth

- 15.6.4 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.2.1 OVERVIEW OF KEY STRATEGIES ADOPTED BY KEY PLAYERS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 16.3 REVENUE ANALYSIS, 2020-2024

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.5 BRAND COMPARISON

- 16.6 COMPANY VALUATION & FINANCIAL METRICS

- 16.6.1 FINANCIAL METRICS

- 16.6.2 COMPANY VALUATION

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Component footprint

- 16.7.5.4 Application footprint

- 16.7.5.5 End-user footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 MCKESSON CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 ORACLE

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 MICROSOFT (NUANCE COMMUNICATIONS, INC.)

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 TRUBRIDGE

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 HEALTH CATALYST

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses & competitive threats

- 17.1.6 VERADIGM LLC

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 ATHENAHEALTH

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches and enhancements

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Other developments

- 17.1.8 GETWELLNETWORK, INC.

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product enhancements

- 17.1.8.3.2 Deals

- 17.1.9 LINCATA, INC.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 COGNIZANT

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deals

- 17.1.11 ONEVIEW HEALTHCARE

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches and enhancements

- 17.1.11.3.2 Deals

- 17.1.11.3.3 Other developments

- 17.1.12 ADVANCEDMD, INC.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product enhancements

- 17.1.12.3.2 Deals

- 17.1.13 EPIC SYSTEMS CORPORATION

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product enhancement

- 17.1.13.3.2 Deals

- 17.1.14 HARRIS HEALTHCARE

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Deals

- 17.1.15 MEDICAL INFORMATION TECHNOLOGY, INC.

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Deals

- 17.1.15.3.2 Other developments

- 17.1.16 TEBRA TECHNOLOGIES, INC.

- 17.1.16.1 Business overview

- 17.1.16.2 Products offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Product enhancements

- 17.1.16.3.2 Deals

- 17.1.17 TELEVOX

- 17.1.17.1 Business overview

- 17.1.17.2 Products offered

- 17.1.17.3 Recent developments

- 17.1.17.3.1 Product launches

- 17.1.17.3.2 Deals

- 17.1.18 SOLUTIONREACH, INC.

- 17.1.18.1 Business overview

- 17.1.18.2 Products offered

- 17.1.18.3 Recent developments

- 17.1.18.3.1 Product launches and enhancements

- 17.1.19 EXPERIAN INFORMATION SOLUTIONS, INC.

- 17.1.19.1 Business overview

- 17.1.19.2 Products offered

- 17.1.20 ECLINICALWORKS

- 17.1.20.1 Business overview

- 17.1.20.2 Products offered

- 17.1.1 MCKESSON CORPORATION

- 17.2 OTHER PLAYERS

- 17.2.1 WELLSTACK

- 17.2.2 RELATIENT

- 17.2.3 LUMA HEALTH INC.

- 17.2.4 CIPHERHEALTH INC.

- 17.2.5 YOSI HEALTH

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH APPROACH

- 18.1.1 SECONDARY RESEARCH

- 18.1.1.1 Key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY RESEARCH

- 18.1.2.1 Primary sources

- 18.1.2.2 Key objectives of primary research

- 18.1.2.3 Key data from primary sources

- 18.1.2.4 Breakdown of primaries

- 18.1.2.5 Insights from primary experts

- 18.1.1 SECONDARY RESEARCH

- 18.2 RESEARCH METHODOLOGY DESIGN

- 18.3 MARKET SIZE ESTIMATION

- 18.3.1 BOTTOM-UP APPROACH (REVENUE SHARE ANALYSIS)

- 18.3.2 TOP-DOWN OF PARENT MARKET ASSESSMENT

- 18.3.3 PRIMARY INTERVIEWS

- 18.3.4 TOP-DOWN APPROACH

- 18.4 DATA TRIANGULATION

- 18.5 MARKET SHARE ESTIMATION

- 18.6 STUDY ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

- 18.8 RISK ANALYSIS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS

List of Tables

- TABLE 1 PATIENT ENGAGEMENT SOLUTIONS MARKET: INCLUSIONS & EXCLUSIONS

- TABLE 2 EXCHANGE RATES UTILIZED FOR CONVERSION TO USD

- TABLE 3 IMPACT OF PORTER'S FIVE FORCES ON PATIENT ENGAGEMENT SOLUTIONS MARKET

- TABLE 4 ROLE OF COMPANIES IN PATIENT ENGAGEMENT SOLUTIONS MARKET ECOSYSTEM

- TABLE 5 INDICATIVE PRICE FOR PATIENT ENGAGEMENT SOLUTIONS, BY COMPONENT, 2025 (USD)

- TABLE 6 INDICATIVE PRICE FOR PATIENT ENGAGEMENT SOLUTIONS, BY REGION, 2025 (USD)

- TABLE 7 IMPORT SCENARIO FOR HS CODE 8528, 2021-2024 (USD THOUSAND)

- TABLE 8 IMPORT SCENARIO FOR HS CODE 8741, 2021-2024 (USD THOUSAND)

- TABLE 9 EXPORT SCENARIO FOR HS CODE 8528, 2021-2024 (USD THOUSAND)

- TABLE 10 EXPORT SCENARIO FOR HS CODE 8471, 2021-2024 (USD THOUSAND)

- TABLE 11 LIST OF KEY CONFERENCES AND EVENTS IN PATIENT ENGAGEMENT SOLUTIONS MARKET, JANUARY 2026-DECEMBER 2027

- TABLE 12 CASE STUDY 1: ACHIEVING USD 15 MILLION IN SAVINGS BY REDUCING READMISSIONS WITH POST-DISCHARGE FOLLOW-UP

- TABLE 13 CASE STUDY 2: BUILD TRUST THROUGH PATIENT ENGAGEMENT TECHNOLOGY: A CHILDREN'S HOSPITAL CASE STUDY

- TABLE 14 CASE STUDY 3: IMPROVING PATIENT ENGAGEMENT AT SPARTA COMMUNITY HOSPITAL WITH TRUBRIDGE PATIENT CONNECT

- TABLE 15 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 16 JURISDICTION ANALYSIS OF TOP APPLICANT COUNTRIES FOR PATIENT ENGAGEMENT SOLUTIONS MARKET

- TABLE 17 LIST OF PATENTS/PATENT APPLICATIONS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- TABLE 18 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 REGULATORY SCENARIO OF NORTH AMERICA

- TABLE 24 REGULATORY SCENARIO OF EUROPE

- TABLE 25 REGULATORY SCENARIO OF ASIA PACIFIC

- TABLE 26 REGULATORY SCENARIO OF LATIN AMERICA

- TABLE 27 REGULATORY SCENARIO OF MIDDLE EAST & AFRICA

- TABLE 28 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS OF MAJOR END USERS (%)

- TABLE 29 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 30 UNMET NEEDS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- TABLE 31 END-USER EXPECTATIONS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- TABLE 32 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 33 LIST OF PRODUCTS OFFERED BY KEY PLAYERS IN PATIENT ENGAGEMENT HARDWARE MARKET

- TABLE 34 PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 35 PATIENT ENGAGEMENT HARDWARE MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 36 PATIENT ENGAGEMENT HARDWARE MARKET FOR IN-ROOM TELEVISIONS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 37 PATIENT ENGAGEMENT HARDWARE MARKET FOR INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 38 PATIENT ENGAGEMENT HARDWARE MARKET FOR TABLETS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 39 LIST OF PRODUCTS OFFERED BY KEY PLAYERS IN PATIENT ENGAGEMENT SOFTWARE MARKET

- TABLE 40 PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 41 PATIENT ENGAGEMENT SOFTWARE MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 42 PATIENT ENGAGEMENT SOFTWARE MARKET FOR PRE-CARE ENGAGEMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 43 PATIENT ENGAGEMENT SOFTWARE MARKET FOR POINT-OF-CARE ENGAGEMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 44 PATIENT ENGAGEMENT SOFTWARE MARKET FOR POST-CARE ENGAGEMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 45 LIST OF PRODUCTS OFFERED BY KEY PLAYERS IN PATIENT ENGAGEMENT SERVICES MARKET

- TABLE 46 PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 47 PATIENT ENGAGEMENT SERVICES MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 48 PATIENT ENGAGEMENT SERVICES MARKET FOR IMPLEMENTATION & INTEGRATION SERVICES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 49 PATIENT ENGAGEMENT SERVICES MARKET FOR TRAINING & EDUCATION SERVICES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 50 PATIENT ENGAGEMENT SERVICES MARKET FOR SUPPORT & MAINTENANCE SERVICES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 51 PATIENT ENGAGEMENT SERVICES MARKET FOR CONSULTING SERVICES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 52 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 53 KEY COMPANIES OFFERING ON-PREMISES PATIENT ENGAGEMENT SOLUTIONS

- TABLE 54 ON-PREMISES PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 55 KEY COMPANIES OFFERING CLOUD-BASED PATIENT ENGAGEMENT SOLUTIONS

- TABLE 56 CLOUD-BASED PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 57 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 58 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR CLINICAL CARE

- TABLE 59 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CLINICAL CARE, BY REGION, 2024-2031 (USD MILLION)

- TABLE 60 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR CARE COORDINATION & COMMUNICATION

- TABLE 61 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARE COORDINATION & COMMUNICATION, BY REGION, 2024-2031 (USD MILLION)

- TABLE 62 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR HOME & REMOTE CARE

- TABLE 63 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME & REMOTE CARE, BY REGION, 2024-2031 (USD MILLION)

- TABLE 64 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR POPULATION HEALTH & BEHAVIORAL ENGAGEMENT

- TABLE 65 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR POPULATION HEALTH & BEHAVIORAL ENGAGEMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 66 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR FINANCIAL ENGAGEMENT

- TABLE 67 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL ENGAGEMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 68 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR OTHER APPLICATIONS

- TABLE 69 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER APPLICATIONS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 70 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 71 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR CHRONIC DISEASES

- TABLE 72 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 73 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 74 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 75 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 76 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY REGION, 2024-2031 (USD MILLION)

- TABLE 77 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR RESPIRATORY DISORDERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 78 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ONCOLOGY, BY REGION, 2024-2031 (USD MILLION)

- TABLE 79 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 80 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR WOMEN'S HEALTH

- TABLE 81 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY REGION, 2024-2031 (USD MILLION)

- TABLE 82 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR BEHAVIORAL & MENTAL HEALTH

- TABLE 83 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BEHAVIORAL & MENTAL HEALTH, BY REGION, 2024-2031 (USD MILLION)

- TABLE 84 MAJOR PLAYERS OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR OTHER THERAPEUTIC AREAS

- TABLE 85 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 86 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 87 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR PATIENT/CLIENT SCHEDULING

- TABLE 88 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY REGION, 2024-2031 (USD MILLION)

- TABLE 89 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR TELEHEALTH

- TABLE 90 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY REGION, 2024-2031 (USD MILLION)

- TABLE 91 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR E-PRESCRIBING

- TABLE 92 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY REGION, 2024-2031 (USD MILLION)

- TABLE 93 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR DOCUMENT MANAGEMENT

- TABLE 94 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 95 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR BILLING & PAYMENTS

- TABLE 96 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 97 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR PATIENT EDUCATION

- TABLE 98 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY REGION, 2024-2031 (USD MILLION)

- TABLE 99 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS FOR OTHER FUNCTIONALITIES

- TABLE 100 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 101 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 102 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS TO PAYERS

- TABLE 103 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 104 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 105 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 106 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ASCS, ACCS, AND OTHER OUTPATIENT SETTINGS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 107 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTHCARE PROVIDERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 108 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 109 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS TO PAYERS

- TABLE 110 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 111 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 112 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 113 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 114 MAJOR COMPANIES OFFERING PATIENT ENGAGEMENT SOLUTIONS TO OTHER END USERS

- TABLE 115 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 116 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 117 NORTH AMERICA: KEY MACROINDICATORS

- TABLE 118 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 119 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 120 NORTH AMERICA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 121 NORTH AMERICA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 122 NORTH AMERICA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 123 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 124 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 125 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 126 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 127 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 128 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 129 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 130 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 131 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 132 US: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 133 US: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 134 US: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 135 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 136 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 137 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 138 US: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 139 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 140 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 141 US: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 142 US: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 143 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 144 CANADA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 145 CANADA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 146 CANADA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 147 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 148 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 149 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 150 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 151 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 152 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 153 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 154 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 155 EUROPE: KEY MACROINDICATORS

- TABLE 156 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 157 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 158 EUROPE: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 159 EUROPE: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 160 EUROPE: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 161 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 162 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 163 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 164 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 165 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 166 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 167 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 168 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 169 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 170 GERMANY: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 171 GERMANY: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 172 GERMANY: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 173 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 174 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 175 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 176 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 177 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 178 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 179 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 180 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 181 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 182 FRANCE: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 183 FRANCE: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 184 FRANCE: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 185 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 186 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 187 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 188 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 189 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 190 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 191 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 192 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 193 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 194 UK: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 195 UK: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 196 UK: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 197 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 198 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 199 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 200 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 201 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 202 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 203 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 204 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 205 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 206 ITALY: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 207 ITALY: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 208 ITALY: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 209 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 210 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 211 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 212 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 213 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 214 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 215 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 216 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 217 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 218 SPAIN: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 219 SPAIN: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 220 SPAIN: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 221 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 222 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 223 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 224 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 225 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 226 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 227 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 228 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 229 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 230 REST OF EUROPE: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 231 REST OF EUROPE: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 232 REST OF EUROPE: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 233 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 234 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 235 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 236 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 237 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 238 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 239 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 240 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 241 ASIA PACIFIC: KEY MACROINDICATORS

- TABLE 242 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 243 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 244 ASIA PACIFIC: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 245 ASIA PACIFIC: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 246 ASIA PACIFIC: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 247 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 248 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 249 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 250 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 251 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 252 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 253 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 254 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 255 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 256 CHINA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 257 CHINA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 258 CHINA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 259 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 260 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 261 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 262 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 263 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 264 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 265 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 266 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 267 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 268 JAPAN: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 269 JAPAN: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 270 JAPAN: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 271 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 272 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 273 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 274 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 275 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 276 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 277 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 278 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 279 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 280 INDIA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 281 INDIA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 282 INDIA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 283 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 284 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 285 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 286 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 287 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 288 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 289 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 290 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 291 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 292 SOUTH KOREA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 293 SOUTH KOREA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 294 SOUTH KOREA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 295 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 296 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 297 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 298 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 299 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 300 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 301 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 302 SOUTH KOREA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 303 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 304 AUSTRALIA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 305 AUSTRALIA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 306 AUSTRALIA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 307 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 308 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 309 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 310 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 311 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 312 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 313 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 314 AUSTRALIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 315 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 316 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 317 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 318 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 319 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 320 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 321 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 322 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 323 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 324 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 325 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 326 REST OF ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 327 LATIN AMERICA: KEY MACROINDICATORS

- TABLE 328 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 329 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 330 LATIN AMERICA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 331 LATIN AMERICA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 332 LATIN AMERICA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 333 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 334 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 335 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 336 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 337 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 338 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 339 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 340 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 341 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 342 BRAZIL: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 343 BRAZIL: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 344 BRAZIL: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 345 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 346 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 347 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 348 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 349 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 350 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 351 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 352 BRAZIL: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 353 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 354 MEXICO: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 355 MEXICO: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 356 MEXICO: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 357 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 358 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 359 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 360 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 361 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 362 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 363 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 364 MEXICO: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 365 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 366 REST OF LATIN AMERICA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 367 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 368 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 369 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 370 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 371 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 372 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 373 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 374 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 375 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 376 REST OF LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 377 MIDDLE EAST & AFRICA: KEY MACROINDICATORS

- TABLE 378 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 379 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 380 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 381 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 382 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 383 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 384 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 385 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 386 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 387 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 388 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 389 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 390 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 391 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 392 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 393 GCC COUNTRIES: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 394 GCC COUNTRIES: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 395 GCC COUNTRIES: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 396 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 397 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 398 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 399 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 400 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 401 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 402 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 403 GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 404 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 405 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 406 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 407 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 408 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 409 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 410 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 411 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 412 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 413 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 414 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 415 KINGDOM OF SAUDI ARABIA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 416 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 417 UAE: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 418 UAE: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 419 UAE: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 420 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 421 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 422 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 423 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 424 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 425 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 426 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 427 UAE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 428 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 429 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 430 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 431 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 432 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 433 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 434 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 435 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 436 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 437 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 438 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 439 REST OF GCC COUNTRIES: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 440 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 441 SOUTH AFRICA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 442 SOUTH AFRICA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 443 SOUTH AFRICA: PATIENT ENGAGEMENT SERVICES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 444 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2024-2031 (USD MILLION)

- TABLE 445 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 446 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERPEUTIC AREA, 2024-2031 (USD MILLION)

- TABLE 447 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 448 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2024-2031 (USD MILLION)

- TABLE 449 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 450 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 451 SOUTH AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 452 REST OF MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 453 REST OF MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT HARDWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 454 REST OF MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOFTWARE MARKET, BY TYPE, 2024-2031 (USD MILLION)