PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2003242

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2003242

Data Center Liquid Cooling Market By Component (Solution and Services), End User (Colocation Providers, Enterprises, and Hyperscale Data Centers), Cooling Medium, Data Center Type, Type of Cooling, Enterprise, and Region - Global Forecast to 2033

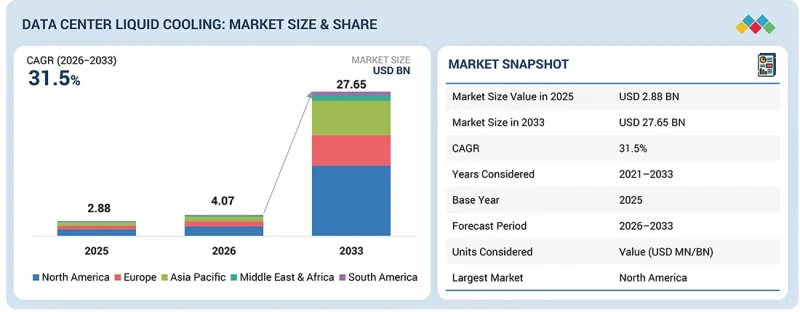

The global data center liquid cooling market will rise from USD 4.07 billion in 2026 to USD 27.65 billion by 2033, at a CAGR of 31.5% from 2026 to 2033. The liquid cooling market for data centers is increasing owing to increased power densities of high-performance computing devices such as GPUs and CPUs, requiring efficient cooling mechanisms. Liquid solutions such as direct-to-chip and immersion cooling are being adopted increasingly to deal with high-density data center problems better than conventional air cooling. The growth in edge computing and IoT further stimulates demand for compact and efficient cooling solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | Value (USD Billion and USD Million) |

| Segments | Component, Data Center Type, Type of Cooling, End User, Enterprise, Cooling Medium, and Region |

| Regions covered | Asia Pacific, North America, Europe, the Middle East & Africa, and South America |

There is also significant emphasis placed on minimizing energy and water consumption. Government support and rising data center investments around the world are also driving faster adoption of newer cooling technologies to boost efficiency and cut operational expenses.

"The services sector within the components category is projected to witness the fastest CAGR from 2026 to 2033."

The services segment in the data center liquid cooling market is anticipated to witness the highest CAGR during the forecast period due to the increasing complexity of liquid cooling systems, which require specialized installation and maintenance. As organizations proceed to embrace enhanced cooling systems, consulting services with the capacity to enhance performance and energy efficiency are in great demand. Edge computing also demands that cooling requirements be addressed through expert support. In addition, ongoing maintenance and development are critical for upholding compliance and sustainability.

"The small and mid-sized data center segment is expected to experience the highest CAGR from 2026 to 2033."

The small and mid-sized data centers segment is projected to register the highest CAGR during the forecast period. These data centers are often limited spatially, making liquid cooling technologies like direct-to-chip and immersion cooling more attractive because of their compact architecture and higher cooling effectiveness. Furthermore, increasing emphasis on energy efficiency and sustainability is compatible with the performance objectives of small data centers to lower energy expenditures. Increasing adoption of edge computing and IoT applications requires innovative cooling solutions, thus driving the use of liquid cooling technologies.

"The hyperscale data centers segment is expected to experience the highest CAGR from 2026 to 2033."

Hyperscale data centers are expected to register the highest CAGR due to their ability to handle large amounts of data, along with scalability and cost benefits. Increased demand for cloud services and big data analysis drives infrastructure investment to facilitate quick growth to meet consumer demands. Besides, advancements in energy-saving technology and state-of-the-art cooling systems make their operation more efficient, which makes them an attractive investment opportunity. As more businesses shift to the cloud, hyperscale data centers offer the flexibility and scalability needed for demanding workloads. This is further enhanced by advancements in artificial intelligence and machine learning, which require significant computational resources, making the hyperscale business model essential for modern data infrastructure.

"The IT and telecom sector is anticipated to register the fastest CAGR from 2026 to 2033."

The rapid digital transformation in many sectors is creating a need for better data processing and storage technologies. The increasing use of cloud computing, big data analytics, and artificial intelligence requires infrastructure capable of effectively managing increased thermal output. Furthermore, the deployment of 5G networks escalates bandwidth requirements, resulting in increased demand for data centers that employ efficient cooling techniques. The proliferation of IoT devices necessitates scalable cooling systems to support the growing number of linked devices. These advancements underscore the imperative for novel cooling systems that enhance energy efficiency and facilitate high-performance operations in the IT and Telecom sectors.

"The direct-to-chip cooling segment is expected to experience the fastest CAGR between 2026 and 2033."

The direct-to-chip cooling market is anticipated to experience the highest CAGR during the forecast period. Direct-to-chip cooling effectively cools high-power components such as CPUs and GPUs with great efficiency, addressing the increasing heat densities present in modern data centers. Furthermore, advancements in cold plate technology have improved thermal efficiency and heat dissipation compared to traditional air-cooling methods. The rising demand for high-performance computing and artificial intelligence applications necessitates more effective cooling systems, thereby boosting demand in this segment. Additionally, the energy efficiency benefits of direct-to-chip cooling align with global efforts to reduce environmental impact, making it an attractive option for data center operators seeking eco-friendly cooling solutions.

"North America is estimated to be the largest market during the forecast period."

The North American region is projected to experience the highest CAGR in the data center liquid cooling market. The rapid digital revolution and the increasing use of cloud services in countries like the US and Canada have resulted in high power densities within data centers. Additionally, the demand for efficient cooling technologies is further fueled by the growth of edge computing and Internet of Things (IoT) applications across the region.

Government policies that promote energy efficiency and sustainability also facilitate the implementation of advanced cooling solutions. Furthermore, significant investments in data center infrastructure, particularly from technology giants and emerging players, are driving the growth of liquid cooling systems in North America.

The distribution of the main participants in the report is as follows:

- By Company Type: Tier 1 - 20%, Tier 2 - 40%, and Tier 3 - 40%

- By Job Title: C-level Executives - 10%, Directors - 70%, and Other Roles - 20%

- By Region: North America - 45%, Asia Pacific - 25%, Europe - 20%, Middle East & Africa - 5%, and South America - 5%

Research Coverage:

The study categorizes and projects the liquid cooling market for data centers based on component, data center type, cooling method, end user, organization, and region. It offers a summary of the primary variables affecting market growth, including drivers, restraints, opportunities, and challenges pertinent to certain industries. It systematically profiles key providers of data center liquid cooling solutions and offers a comprehensive analysis of their market shares and core competencies; it also observes and evaluates competitive actions, including expansion initiatives, agreements, contracts, partnerships with other entities in this sector, as well as acquisitions or divestitures undertaken by them.

Reasons to Buy the Report:

Market leaders and new entrants are expected to benefit from the report, which will provide them with close estimates of revenue figures for the forthcoming data center liquid cooling market and its segments. The report is also expected to assist stakeholders in improving their understanding of the competitive landscape in the market, obtaining insights for enhancing their business position, and designing relevant go-to-market strategies. In addition, it allows them to comprehend the market's pulse and informs them about key drivers, restraints, challenges, and opportunities.

Insights from this report include:

- Analysis of key drivers (rising number of data centers and server density), restraints (high capital expenditure and maintenance), opportunities (emergence of AI, blockchain, and other advanced technologies) & challenges (lack of standardization) influencing growth in the liquid cooling solutions for the data center market.

- Product Development/Innovation: Detailed information on emerging technologies and research & development initiatives in liquid cooling within data centers.

- Market Development: Detailed analysis of the data center liquid cooling market across different areas for analyzing lucrative markets - comprehensive details included in the report.

- Market Diversification: Detailed information about innovative offerings and regions with no market penetration. We are considering investment opportunities as well as new products and services in the context of this cooling system.

- Competitive Assessment: A thorough estimation of the market share of key companies and their product offerings is provided. Rittal GmbH & Co. KG (Friedhelm Loh Group) (Germany), Vertiv Group Corp (US), Green Revolution Cooling Inc. (GRC) (US), Submer (Spain), Schneider Electric (France), Super Micro Computer, Inc. (US), LiquidStack Holding B.V. (Trane Technologies) (US), Iceotope Precision Liquid Cooling (UK), COOLIT SYSTEMS (Canada), Baltimore Aircoil Company Inc. (US), DCX Liquid Cooling Systems (Poland), Delta Power Solutions (Taiwan), Wiwynn Corporation (Taiwan), LiquidCool Solutions, Inc. (US), Midas Immersion Cooling (US), BOYD (US), Kaori Heat Treatment Co., Ltd. (Taiwan), Daikin Industries, Ltd. (Japan), Modine Manufacturing Company (US), Asperitas (Netherlands), Zutacore, Inc. (US), Flex Ltd. (US), Accelsius LLC (US), Refroid Technologies (India), nVent (UK) INSPUR Co., Ltd. (China), Sugon Information Industry Co., Ltd. (China), Lenovo (China), and STULZ GMBH (Germany) are the key players leading the market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DATA CENTER LIQUID COOLING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER LIQUID COOLING MARKET

- 3.2 DATA CENTER LIQUID COOLING MARKET, BY END USER

- 3.3 DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE

- 3.4 DATA CENTER LIQUID COOLING MARKET, BY REGION

- 3.5 DATA CENTER LIQUID COOLING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing server density and high number of data centers

- 4.2.1.2 Growing need for energy-efficient cooling solutions

- 4.2.1.3 Rising demand for compact and noise-free solutions

- 4.2.1.4 Surging need for better overclocking potential

- 4.2.1.5 Increasing requirement for eco-friendly data center cooling solutions

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital expenditure and maintenance requirements

- 4.2.2.2 Slow recognition from end users

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of artificial intelligence, blockchain, and other advanced technologies

- 4.2.3.2 Adoption of immersion cooling solutions in low-density data centers

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of standardization

- 4.2.4.2 High investments in existing data center infrastructure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER LIQUID COOLING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 DATA CENTER INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DATA CENTER COOLING INDUSTRY

- 5.2.5 MANUFACTURING INDUSTRY

- 5.2.6 TRENDS IN GLOBAL HYPERSCALE AND AI DATA CENTER INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SINGLE-PHASE VS. TWO-PHASE LIQUID COOLING: CHOOSING OPTIMAL SOLUTION FOR HIGH-PERFORMANCE DATA CENTERS

- 5.6 ENERGY SUSTAINABILITY FOR DATA CENTERS

- 5.6.1 SUSTAINABLE DATA CENTERS USING LIQUID COOLING

- 5.6.2 ISSUES IN DEVELOPING COUNTRIES

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: ENHANCED DATA CENTER EFFICIENCY WITH DIRECT LIQUID COOLING

- 5.10.2 CASE STUDY 2: OPTIMIZED HYPERSCALE DATA CENTER EFFICIENCY WITH TWO-PHASE IMMERSION COOLING (2-PIC)

6 KEY EMERGING TECHNOLOGIES

- 6.1 OVERVIEW

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Direct-to-liquid cooling in high-density data centers

- 6.1.1.2 Immersion cooling

- 6.1.2 ADJACENT TECHNOLOGIES

- 6.1.2.1 Microchannel liquid cooling

- 6.1.2.2 Microconvective liquid cooling

- 6.1.1 KEY TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.2.1 METHODOLOGY

- 6.2.2 INSIGHTS

- 6.2.3 LEGAL STATUS OF PATENTS

- 6.2.4 JURISDICTION ANALYSIS

- 6.2.5 TOP APPLICANTS

- 6.3 FUTURE APPLICATIONS

- 6.3.1 AI-OPTIMIZED HYPERSCALE DATA CENTERS: ULTRA-HIGH-DENSITY GPU & AI TRAINING CLUSTERS

- 6.3.2 EDGE & DISTRIBUTED DATA CENTERS: COMPACT, MODULAR, AND TELECOM-INTEGRATED DEPLOYMENTS

- 6.3.3 WASTE HEAT RECOVERY & DISTRICT ENERGY SYSTEMS: CIRCULAR ENERGY & SUSTAINABILITY INTEGRATION

- 6.3.4 IMMERSION COOLING FOR HIGH-PERFORMANCE INDUSTRIES: DEFENSE, RESEARCH, FINANCIAL TRADING, AND SCIENTIFIC HPC

- 6.3.5 SUSTAINABLE & WATERLESS COOLING TECHNOLOGIES: LOW-CARBON, LOW-WUE THERMAL ARCHITECTURES

- 6.4 IMPACT OF AI/GEN AI ON DATA CENTER LIQUID COOLING MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST MARKET PRACTICES

- 6.4.3 CASE STUDIES OF AI IMPLEMENTATION IN DATA CENTER LIQUID COOLING MARKET

- 6.4.4 READINESS OF COMPANIES TO ADOPT GENERATIVE AI IN DATA CENTER LIQUID COOLING MARKET

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1.1 US

- 7.1.1.2 Europe

- 7.1.1.3 China

- 7.1.1.4 Japan

- 7.1.1.5 India

- 7.1.1.6 Singapore

- 7.1.2 OPEN COMPUTE PROJECT (OCP): A STANDARD FOR DATA CENTER BUILDINGS

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO APPLICATIONS OF DATA CENTER LIQUID COOLING

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 DATA CENTER LIQUID COOLING MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 SOLUTIONS

- 9.2.1 INDIRECT LIQUID COOLING SOLUTIONS

- 9.2.1.1 Growing demand for precision cooling to drive market

- 9.2.1.1.1 Single-phase indirect cooling

- 9.2.1.1.2 Two-phase indirect cooling

- 9.2.1.1 Growing demand for precision cooling to drive market

- 9.2.2 DIRECT LIQUID COOLING SOLUTIONS

- 9.2.2.1 Increasing demand for high-density cooling to fuel market growth

- 9.2.2.1.1 Single-phase direct cooling

- 9.2.2.1.2 Two-phase direct cooling

- 9.2.2.1 Increasing demand for high-density cooling to fuel market growth

- 9.2.1 INDIRECT LIQUID COOLING SOLUTIONS

- 9.3 SERVICES

- 9.3.1 DESIGN & CONSULTING

- 9.3.1.1 Rising demand for consulting services for liquid cooling systems to drive market

- 9.3.2 INSTALLATION & DEPLOYMENT

- 9.3.2.1 Integration of liquid cooling systems with traditional cooling devices to drive demand

- 9.3.3 SUPPORT & MAINTENANCE

- 9.3.3.1 Growing need for maintenance of coolants to drive market

- 9.3.1 DESIGN & CONSULTING

10 DATA CENTER LIQUID COOLING MARKET, BY COOLING MEDIUM

- 10.1 INTRODUCTION

- 10.2 WATER

- 10.3 DIELECTRIC

- 10.4 REFRIGERANTS

11 DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE

- 11.1 INTRODUCTION

- 11.2 DIRECT-TO-CHIP COOLING

- 11.2.1 INCREASING HIGH-DENSITY DATA CENTER INSTALLATIONS TO DRIVE DEMAND

- 11.3 IMMERSION LIQUID COOLING

- 11.3.1 ABILITY TO LOWER POWER CONSUMPTION AND CARBON FOOTPRINT TO DRIVE MARKET

- 11.4 SPRAY LIQUID COOLING

- 11.4.1 HIGH ENERGY SAVINGS, EXCELLENT HEAT-DISSIPATION EFFICIENCY, AND SILENT OPERATION TO DRIVE DEMAND

12 DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE

- 12.1 INTRODUCTION

- 12.2 SMALL & MID-SIZED DATA CENTERS

- 12.2.1 GROWING NEED FOR INDIRECT LIQUID COOLING SOLUTIONS TO DRIVE MARKET

- 12.3 LARGE DATA CENTERS

- 12.3.1 INCREASING REQUIREMENT FOR DIRECT LIQUID COOLING IN LARGE DATA CENTERS TO DRIVE MARKET

13 DATA CENTER LIQUID COOLING MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 COLOCATION PROVIDERS

- 13.2.1 USE OF COLOCATION DATA CENTERS FOR DISASTER RECOVERY TO DRIVE DEMAND

- 13.3 ENTERPRISES

- 13.3.1 RISING NEED FOR DATA MANAGEMENT AND DOWNTIME REDUCTION TO DRIVE MARKET

- 13.4 HYPERSCALE DATA CENTERS

- 13.4.1 SURGING REQUIREMENT FOR SCALABLE COOLING SOLUTIONS TO BOOST DEMAND

14 DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE

- 14.1 INTRODUCTION

- 14.2 BFSI

- 14.2.1 RISING FOCUS ON LOWERING ENERGY CONSUMPTION TO DRIVE DEMAND

- 14.3 IT & TELECOM

- 14.3.1 GROWING ADOPTION OF ADVANCED SERVERS TO DRIVE MARKET

- 14.4 MEDIA & ENTERTAINMENT

- 14.4.1 INCREASING REQUIREMENT FOR SCALE-OUT SOLUTIONS TO DRIVE DEMAND

- 14.5 HEALTHCARE

- 14.5.1 RISING DEMAND FOR CUSTOMIZED DATA CENTER COOLING SOLUTIONS TO DRIVE MARKET

- 14.6 GOVERNMENT & DEFENSE

- 14.6.1 GROWING DIGITALIZATION INITIATIVES TO FUEL DEMAND

- 14.7 RETAIL

- 14.7.1 INCREASED NEED FOR ROBUST COOLING TO DRIVE DEMAND

- 14.8 RESEARCH & ACADEMIA

- 14.8.1 ADOPTION OF HIGH-PERFORMANCE COMPUTING TO DRIVE MARKET

- 14.9 OTHER ENTERPRISES

15 DATA CENTER LIQUID COOLING MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Rising demand for immersion cooling solutions from cryptocurrency providers to drive market

- 15.2.2 CANADA

- 15.2.2.1 Surge in digitalization and data generation to drive demand

- 15.2.3 MEXICO

- 15.2.3.1 Increasing requirement for cloud, big data, and IoT to drive market

- 15.2.1 US

- 15.3 ASIA PACIFIC

- 15.3.1 CHINA

- 15.3.1.1 Increasing number of colocation facilities and rising data center revenues to drive demand

- 15.3.2 SOUTH KOREA

- 15.3.2.1 Rising adoption of AI and big data technologies to fuel demand

- 15.3.3 JAPAN

- 15.3.3.1 Increasing investments in making data centers greener and more efficient to drive adoption

- 15.3.4 INDIA

- 15.3.4.1 Rising data demand and capacity of data centers to drive adoption

- 15.3.5 MALAYSIA

- 15.3.5.1 Abundant availability of renewable resources and government initiatives to drive market

- 15.3.6 SINGAPORE

- 15.3.6.1 Thriving internet economy to drive demand

- 15.3.7 AUSTRALIA

- 15.3.7.1 Government-led initiatives for infrastructure development to drive adoption

- 15.3.8 REST OF ASIA PACIFIC

- 15.3.1 CHINA

- 15.4 EUROPE

- 15.4.1 UK

- 15.4.1.1 Eco-design requirements set by European Parliament for servers and data storage products to drive market

- 15.4.2 GERMANY

- 15.4.2.1 Substantial investment in data centers to drive demand

- 15.4.3 FRANCE

- 15.4.3.1 Growing adoption of colocation services and overloading and heat issues in data centers to drive demand

- 15.4.4 REST OF EUROPE

- 15.4.1 UK

- 15.5 SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.5.1.1 Surge in IT spending across enterprises to fuel demand for data centers

- 15.5.2 REST OF SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 GCC COUNTRIES

- 15.6.1.1 Saudi Arabia

- 15.6.1.1.1 Increasing demand for rugged data center solutions to drive market

- 15.6.1.2 Other GCC countries

- 15.6.1.2.1 Hyperscale investments and extreme climatic conditions to drive market

- 15.6.1.1 Saudi Arabia

- 15.6.2 SOUTH AFRICA

- 15.6.2.1 Developed telecommunication infrastructure to drive demand

- 15.6.3 REST OF MIDDLE EAST & AFRICA

- 15.6.1 GCC COUNTRIES

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.3 REVENUE ANALYSIS, 2024

- 16.3.1 TOP FOUR PLAYERS: REVENUE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.4.1 RANKING OF KEY MARKET PLAYERS, 2024

- 16.5 BRAND/PRODUCT COMPARISON

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 16.6.5.1 Company footprint

- 16.6.5.2 Region footprint

- 16.6.5.3 Component footprint

- 16.6.5.4 Enterprise footprint

- 16.6.5.5 Data center type footprint

- 16.6.5.6 Cooling type footprint

- 16.6.5.7 End user footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 DYNAMIC COMPANIES

- 16.7.3 RESPONSIVE COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.8 COMPANY VALUATION AND FINANCIAL METRICS

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 VERTIV GROUP CORP.

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Expansions

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 SUPER MICRO COMPUTER, INC.

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Deals

- 17.1.2.3.2 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 SCHNEIDER ELECTRIC

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 DCX LIQUID COOLING SYSTEMS

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 MODINE MANUFACTURING COMPANY

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Expansions

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 GREEN REVOLUTION COOLING, INC.

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.6.3.3 Other developments

- 17.1.6.4 MnM view

- 17.1.6.4.1 Key strengths

- 17.1.6.4.2 Strategic choices

- 17.1.6.4.3 Weaknesses and competitive threats

- 17.1.7 SUBMER

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Expansions

- 17.1.7.3.4 Other developments

- 17.1.7.4 MnM view

- 17.1.7.4.1 Key strengths

- 17.1.7.4.2 Strategic choices

- 17.1.7.4.3 Weaknesses and competitive threats

- 17.1.8 ASPERITAS

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.8.4 MnM view

- 17.1.8.4.1 Key strengths

- 17.1.8.4.2 Strategic choices

- 17.1.8.4.3 Weaknesses and competitive threats

- 17.1.9 COOLIT SYSTEMS

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Deals

- 17.1.9.3.3 Expansions

- 17.1.10 ICEOTOPE PRECISION LIQUID COOLING

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.10.3.3 Expansions

- 17.1.11 RITTAL GMBH & CO. KG (FRIEDHELM LOH GROUP)

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches

- 17.1.11.3.2 Deals

- 17.1.12 MIDAS IMMERSION COOLING

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Deals

- 17.1.13 LIQUIDSTACK HOLDING B.V. (TRANE TECHNOLOGIES)

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product launches

- 17.1.14 DAIKIN INDUSTRIES, LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Deals

- 17.1.15 BALTIMORE AIRCOIL COMPANY, INC.

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product launches

- 17.1.15.3.2 Deals

- 17.1.16 LIQUIDCOOL SOLUTIONS

- 17.1.16.1 Business overview

- 17.1.16.2 Products offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Deals

- 17.1.17 STULZ GMBH

- 17.1.17.1 Business overview

- 17.1.17.2 Products offered

- 17.1.17.3 Recent developments

- 17.1.17.3.1 Product launches

- 17.1.18 DELTA POWER SOLUTIONS

- 17.1.18.1 Business overview

- 17.1.18.2 Products offered

- 17.1.18.3 Recent developments

- 17.1.18.3.1 Deals

- 17.1.19 ZUTACORE, INC.

- 17.1.19.1 Business overview

- 17.1.19.2 Products offered

- 17.1.19.3 Recent developments

- 17.1.19.3.1 Product launches

- 17.1.19.3.2 Deals

- 17.1.20 WIWYNN CORPORATION

- 17.1.20.1 Business overview

- 17.1.20.2 Products offered

- 17.1.20.3 Recent developments

- 17.1.21 BOYD

- 17.1.21.1 Business overview

- 17.1.21.2 Products offered

- 17.1.21.3 Recent developments

- 17.1.22 KAORI HEAT TREATMENT CO., LTD.

- 17.1.22.1 Business overview

- 17.1.22.2 Products offered

- 17.1.22.3 Recent developments

- 17.1.23 FLEX LTD.

- 17.1.23.1 Business overview

- 17.1.23.2 Products offered

- 17.1.23.3 Recent developments

- 17.1.23.3.1 Deals

- 17.1.24 LENOVO

- 17.1.24.1 Business overview

- 17.1.24.2 Products offered

- 17.1.24.3 Recent developments

- 17.1.24.3.1 Product launches

- 17.1.24.3.2 Deals

- 17.1.25 SUGON INFORMATION INDUSTRY CO., LTD.

- 17.1.25.1 Business overview

- 17.1.25.2 Products offered

- 17.1.25.3 Recent developments

- 17.1.25.3.1 Deals

- 17.1.25.3.2 Other developments

- 17.1.26 INSPUR CO., LTD.

- 17.1.26.1 Business overview

- 17.1.26.2 Products offered

- 17.1.26.3 Recent developments

- 17.1.27 NVENT

- 17.1.27.1 Business overview

- 17.1.27.2 Products offered

- 17.1.27.3 Recent developments

- 17.1.27.3.1 Deals

- 17.1.27.3.2 Expansions

- 17.1.28 TAISOL ELECTRONICS CO., LTD.

- 17.1.28.1 Business overview

- 17.1.28.2 Products offered

- 17.1.28.3 Recent developments

- 17.1.29 ACCELSIUS LLC

- 17.1.29.1 Business overview

- 17.1.29.2 Recent developments

- 17.1.30 REFROID TECHNOLOGIES

- 17.1.30.1 Business overview

- 17.1.30.2 Recent developments

- 17.1.30.2.1 Deals

- 17.1.1 VERTIV GROUP CORP.

- 17.2 OTHER PLAYERS

- 17.2.1 TEIMMERS

- 17.2.2 KOOLANCE, INC.

- 17.2.3 GIGA-BYTE TECHNOLOGY CO., LTD.

- 17.2.4 PEZY COMPUTING

- 17.2.5 TAS

- 17.2.6 OPTICOOL TECHNOLOGIES

- 17.2.7 SEGUENTE INC.

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Key industry insights

- 18.1.2.3 List of primary participants

- 18.1.2.4 Breakdown of primary interviews

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH & TOP-DOWN APPROACH

- 18.3 DEMAND-SIDE ANALYSIS

- 18.4 SUPPLY-SIDE ANALYSIS

- 18.4.1 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 18.5 GROWTH FORECAST

- 18.6 DATA TRIANGULATION

- 18.7 RESEARCH ASSUMPTIONS

- 18.8 RESEARCH LIMITATIONS

- 18.9 RISK ASSESSMENT

- 18.10 FACTOR ANALYSIS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS

List of Tables

- TABLE 1 DATA CENTER LIQUID COOLING MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 POWER USAGE BY AIR-COOLED VS. LIQUID-COOLED DATA CENTERS WITH 1 MW OF TECHNICAL LOAD

- TABLE 3 DATA CENTER LIQUID COOLING MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 GDP PERCENTAGE CHANGE OF KEY COUNTRIES, 2021-2029

- TABLE 5 ROLE OF COMPANIES IN DATA CENTER LIQUID COOLING ECOSYSTEM

- TABLE 6 COMPARATIVE ANALYSIS OF DATA CENTER COOLING TECHNOLOGIES

- TABLE 7 DATA CENTER COOLING LIQUID MARKET: KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 8 DATA CENTER LIQUID COOLING MARKET: TOTAL NUMBER OF PATENTS, 2015-2025

- TABLE 9 MAJOR PATENTS RELATED TO DATA CENTER LIQUID COOLING SOLUTIONS

- TABLE 10 DATA CENTER LIQUID COOLING MARKET: TOP USE CASES AND MARKET POTENTIAL

- TABLE 11 DATA CENTER LIQUID COOLING MARKET: BEST PRACTICES

- TABLE 12 DATA CENTER LIQUID COOLING MARKET: CASE STUDIES OF GEN AI IMPLEMENTATION

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 CERTIFICATIONS, LABELING, AND ECO STANDARDS IN DATA CENTER LIQUID COOLING MARKET

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END USER (%)

- TABLE 19 KEY BUYING CRITERIA, BY END USER

- TABLE 20 DATA CENTER LIQUID COOLING MARKET: UNMET NEEDS IN KEY END-USE INDUSTRIES

- TABLE 21 DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 22 DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 23 SOLUTIONS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 24 SOLUTIONS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 25 SERVICES: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 26 SERVICES: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 27 DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE, 2021-2025 (USD MILLION)

- TABLE 28 DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE, 2026-2033 (USD MILLION)

- TABLE 29 DIRECT-TO-CHIP COOLING: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 30 DIRECT-TO-CHIP COOLING: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 31 IMMERSION LIQUID COOLING: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 32 IMMERSION LIQUID COOLING: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 33 DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 34 DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 35 SMALL & MID-SIZED DATA CENTERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 36 SMALL & MID-SIZED DATA CENTERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 37 LARGE DATA CENTERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 38 LARGE DATA CENTERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 39 DATA CENTER LIQUID COOLING MARKET, BY END USER, 2021-2025 (USD MILLION)

- TABLE 40 DATA CENTER LIQUID COOLING MARKET, BY END USER, 2026-2033 (USD MILLION)

- TABLE 41 COLOCATION PROVIDERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 42 COLOCATION PROVIDERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 43 ENTERPRISES: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 44 ENTERPRISES: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 45 HYPERSCALE DATA CENTERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 46 HYPERSCALE DATA CENTERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 47 DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2021-2025 (USD MILLION)

- TABLE 48 DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2026-2033 (USD MILLION)

- TABLE 49 BFSI: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 50 BFSI: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 51 IT & TELECOM: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 52 IT & TELECOM: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 53 MEDIA & ENTERTAINMENT: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 54 MEDIA & ENTERTAINMENT: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 55 HEALTHCARE: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 56 HEALTHCARE: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 57 GOVERNMENT & DEFENSE: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 58 GOVERNMENT & DEFENSE: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 59 RETAIL: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 60 RETAIL: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 61 RESEARCH & ACADEMIA: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 62 RESEARCH & ACADEMIA: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 63 OTHERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 64 OTHERS: DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 65 DATA CENTER LIQUID COOLING MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 66 DATA CENTER LIQUID COOLING MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 67 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 68 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 69 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 70 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 71 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 72 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 73 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2021-2025 (USD MILLION)

- TABLE 74 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2026-2033 (USD MILLION)

- TABLE 75 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2021-2025 (USD MILLION)

- TABLE 76 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2026-2033 (USD MILLION)

- TABLE 77 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE, 2021-2025 (USD MILLION)

- TABLE 78 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE, 2026-2033 (USD MILLION)

- TABLE 79 US: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 80 US: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 81 US: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 82 US: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 83 CANADA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 84 CANADA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 85 CANADA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 86 CANADA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 87 MEXICO: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 88 MEXICO: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 89 MEXICO: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 90 MEXICO: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 91 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 92 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 93 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 94 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 95 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 96 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 97 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2021-2025 (USD MILLION)

- TABLE 98 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2026-2033 (USD MILLION)

- TABLE 99 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2021-2025 (USD MILLION)

- TABLE 100 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2026-2033 (USD MILLION)

- TABLE 101 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE, 2021-2025 (USD MILLION)

- TABLE 102 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COOLING TYPE, 2026-2033 (USD MILLION)

- TABLE 103 CHINA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 104 CHINA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 105 CHINA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 106 CHINA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 107 SOUTH KOREA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 108 SOUTH KOREA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 109 SOUTH KOREA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 110 SOUTH KOREA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 111 JAPAN: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 112 JAPAN: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 113 JAPAN: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 114 JAPAN: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 115 INDIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 116 INDIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 117 INDIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 118 INDIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 119 MALAYSIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 120 MALAYSIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 121 MALAYSIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 122 MALAYSIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 123 SINGAPORE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 124 SINGAPORE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 125 SINGAPORE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 126 SINGAPORE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 127 AUSTRALIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 128 AUSTRALIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 129 AUSTRALIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 130 AUSTRALIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 131 REST OF ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 132 REST OF ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 133 REST OF ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 134 REST OF ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 135 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 136 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 137 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 138 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 139 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 140 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 141 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2021-2025 (USD MILLION)

- TABLE 142 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2026-2033 (USD MILLION)

- TABLE 143 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2021-2025 (USD MILLION)

- TABLE 144 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2026-2033 (USD MILLION)

- TABLE 145 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER COOLING TYPE, 2021-2025 (USD MILLION)

- TABLE 146 EUROPE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER COOLING TYPE, 2026-2033 (USD MILLION)

- TABLE 147 UK: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 148 UK: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 149 UK: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 150 UK: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 151 GERMANY: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 152 GERMANY: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 153 GERMANY: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 154 GERMANY: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 155 FRANCE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 156 FRANCE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 157 FRANCE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 158 FRANCE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 159 REST OF EUROPE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 160 REST OF EUROPE: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 161 REST OF EUROPE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 162 REST OF EUROPE: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 163 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 164 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 165 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 166 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 167 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 168 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 169 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2021-2025 (USD MILLION)

- TABLE 170 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2026-2033 (USD MILLION)

- TABLE 171 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2021-2025 (USD MILLION)

- TABLE 172 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2026-2033 (USD MILLION)

- TABLE 173 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER COOLING TYPE, 2021-2025 (USD MILLION)

- TABLE 174 SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER COOLING TYPE, 2026-2033 (USD MILLION)

- TABLE 175 BRAZIL: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 176 BRAZIL: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 177 BRAZIL: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 178 BRAZIL: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 179 REST OF SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 180 REST OF SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 181 REST OF SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 182 REST OF SOUTH AMERICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 183 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 184 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 185 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 186 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 187 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 188 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 189 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2021-2025 (USD MILLION)

- TABLE 190 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY END USER, 2026-2033 (USD MILLION)

- TABLE 191 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2021-2025 (USD MILLION)

- TABLE 192 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY ENTERPRISE, 2026-2033 (USD MILLION)

- TABLE 193 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER COOLING TYPE, 2021-2025 (USD MILLION)

- TABLE 194 MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER COOLING TYPE, 2026-2033 (USD MILLION)

- TABLE 195 SAUDI ARABIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 196 SAUDI ARABIA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 197 SAUDI ARABIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 198 SAUDI ARABIA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 199 OTHER GCC COUNTRIES: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 200 OTHER GCC COUNTRIES: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 201 OTHER GCC COUNTRIES: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 202 OTHER GCC COUNTRIES: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 203 SOUTH AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 204 SOUTH AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 205 SOUTH AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 206 SOUTH AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 207 REST OF MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2021-2025 (USD MILLION)

- TABLE 208 REST OF MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 209 REST OF MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2021-2025 (USD MILLION)

- TABLE 210 REST OF MIDDLE EAST & AFRICA: DATA CENTER LIQUID COOLING MARKET, BY DATA CENTER TYPE, 2026-2033 (USD MILLION)

- TABLE 211 DATA CENTER LIQUID COOLING MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 212 DATA CENTER LIQUID COOLING MARKET: DEGREE OF COMPETITION

- TABLE 213 DATA CENTER LIQUID COOLING MARKET: REGION FOOTPRINT

- TABLE 214 DATA CENTER LIQUID COOLING MARKET: COMPONENT FOOTPRINT

- TABLE 215 DATA CENTER LIQUID COOLING MARKET: ENTERPRISE FOOTPRINT

- TABLE 216 DATA CENTER LIQUID COOLING MARKET: DATA CENTER TYPE FOOTPRINT

- TABLE 217 DATA CENTER LIQUID COOLING MARKET: COOLING TYPE FOOTPRINT

- TABLE 218 DATA CENTER LIQUID COOLING MARKET: END USER FOOTPRINT

- TABLE 219 DATA CENTER LIQUID COOLING: KEY STARTUPS/SMES

- TABLE 220 DATA CENTER LIQUID COOLING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

- TABLE 221 DATA CENTER LIQUID COOLING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (2/2

- TABLE 222 DATA CENTER LIQUID COOLING MARKET: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 223 DATA CENTER LIQUID COOLING MARKET: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 224 DATA CENTER LIQUID COOLING MARKET: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 225 DATA CENTER LIQUID COOLING MARKET: OTHER DEVELOPMENTS, FEBRUARY 2020-MARCH 2026

- TABLE 226 VERTIV GROUP CORP.: COMPANY OVERVIEW

- TABLE 227 VERTIV GROUP CORP.: PRODUCTS OFFERED

- TABLE 228 VERTIV GROUP CORP.: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 229 VERTIV GROUP CORP.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 230 VERTIV GROUP CORP: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 231 SUPER MICRO COMPUTER, INC.: COMPANY OVERVIEW

- TABLE 232 SUPER MICRO COMPUTER, INC.: PRODUCTS OFFERED

- TABLE 233 SUPER MICRO COMPUTER, INC.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 234 SUPER MICRO COMPUTER, INC.: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 235 SCHNEIDER ELECTRIC: COMPANY OVERVIEW

- TABLE 236 SCHNEIDER ELECTRIC: PRODUCTS OFFERED

- TABLE 237 SCHNEIDER ELECTRIC: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 238 SCHNEIDER ELECTRIC: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 239 SCHNEIDER ELECTRIC: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 240 DCX LIQUID COOLING SYSTEMS: COMPANY OVERVIEW

- TABLE 241 DCX LIQUID COOLING SYSTEMS: PRODUCTS OFFERED

- TABLE 242 DCX LIQUID COOLING SYSTEMS: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 243 MODINE MANUFACTURING COMPANY: COMPANY OVERVIEW

- TABLE 244 MODINE MANUFACTURING COMPANY: PRODUCTS OFFERED

- TABLE 245 MODINE MANUFACTURING COMPANY: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 246 MODINE MANUFACTURING COMPANY: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 247 MODINE MANUFACTURING COMPANY: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 248 GREEN REVOLUTION COOLING, INC.: COMPANY OVERVIEW

- TABLE 249 GREEN REVOLUTION COOLING, INC.: PRODUCTS OFFERED

- TABLE 250 GREEN REVOLUTION COOLING, INC.: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 251 GREEN REVOLUTION COOLING, INC.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 252 GREEN REVOLUTION COOLING, INC.: OTHER DEVELOPMENTS, FEBRUARY 2020-MARCH 2026

- TABLE 253 SUBMER: COMPANY OVERVIEW

- TABLE 254 SUBMER: PRODUCTS OFFERED

- TABLE 255 SUBMER: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 256 SUBMER: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 257 SUBMER: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 258 SUBMER: OTHER DEVELOPMENTS, FEBRUARY 2020-MARCH 2026

- TABLE 259 ASPERITAS: COMPANY OVERVIEW

- TABLE 260 ASPERITAS: PRODUCTS OFFERED

- TABLE 261 ASPERITAS: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 262 ASPERITAS: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 263 COOLIT SYSTEMS: COMPANY OVERVIEW

- TABLE 264 COOLIT SYSTEMS: PRODUCTS OFFERED

- TABLE 265 COOLIT SYSTEMS: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 266 COOLIT SYSTEMS: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 267 COOLIT SYSTEMS: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 268 ICEOTOPE PRECISION LIQUID COOLING: COMPANY OVERVIEW

- TABLE 269 ICEOTOPE PRECISION LIQUID COOLING: PRODUCTS OFFERED

- TABLE 270 ICEOTOPE PRECISION LIQUID COOLING: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 271 ICEOTOPE PRECISION LIQUID COOLING: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 272 ICEOTOPE PRECISION LIQUID COOLING: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 273 RITTAL GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 274 RITTAL GMBH & CO. KG: PRODUCTS OFFERED

- TABLE 275 RITTAL GMBH & CO. KG: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 276 RITTAL GMBH & CO. KG: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 277 MIDAS IMMERSION COOLING: COMPANY OVERVIEW

- TABLE 278 MIDAS IMMERSION COOLING: PRODUCTS OFFERED

- TABLE 279 MIDAS IMMERSION COOLING: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 280 LIQUIDSTACK HOLDING B.V. (TRANE TECHNOLOGIES): COMPANY OVERVIEW

- TABLE 281 LIQUIDSTACK HOLDING B.V. (TRANE TECHNOLOGIES): PRODUCTS OFFERED

- TABLE 282 LIQUIDSTACK HOLDING B.V. (TRANE TECHNOLOGIES): PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 283 DAIKIN INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 284 DAIKIN INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 285 DAIKIN INDUSTRIES, LTD.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 286 BALTIMORE AIRCOIL COMPANY, INC.: COMPANY OVERVIEW

- TABLE 287 BALTIMORE AIRCOIL COMPANY, INC.: PRODUCTS OFFERED

- TABLE 288 BALTIMORE AIRCOIL COMPANY, INC.: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 289 BALTIMORE AIRCOIL COMPANY, INC.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 290 LIQUIDCOOL SOLUTIONS: COMPANY OVERVIEW

- TABLE 291 LIQUIDCOOL SOLUTIONS: PRODUCTS OFFERED

- TABLE 292 LIQUIDCOOL SOLUTIONS: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 293 STULZ GMBH: COMPANY OVERVIEW

- TABLE 294 STULZ GMBH: PRODUCTS OFFERED

- TABLE 295 STULZ GMBH: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 296 DELTA POWER SOLUTIONS: COMPANY OVERVIEW

- TABLE 297 DELTA POWER SOLUTIONS: PRODUCTS OFFERED

- TABLE 298 DELTA POWER SOLUTIONS: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 299 ZUTACORE, INC: COMPANY OVERVIEW

- TABLE 300 ZUTACORE, INC.: PRODUCTS OFFERED

- TABLE 301 ZUTACORE, INC.: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 302 ZUTACORE, INC.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 303 WIWYNN CORPORATION: COMPANY OVERVIEW

- TABLE 304 WIWYNN CORPORATION: PRODUCTS OFFERED

- TABLE 305 BOYD: COMPANY OVERVIEW

- TABLE 306 BOYD: PRODUCTS OFFERED

- TABLE 307 KAORI HEAT TREATMENT CO., LTD.: COMPANY OVERVIEW

- TABLE 308 KAORI HEAT TREATMENT CO., LTD.: PRODUCTS OFFERED

- TABLE 309 FLEX LTD.: COMPANY OVERVIEW

- TABLE 310 FLEX LTD.: PRODUCTS OFFERED

- TABLE 311 FLEX LTD.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 312 LENOVO: COMPANY OVERVIEW

- TABLE 313 LENOVO: PRODUCTS OFFERED

- TABLE 314 LENOVO: PRODUCT LAUNCHES, FEBRUARY 2020-MARCH 2026

- TABLE 315 LENOVO: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 316 SUGON INFORMATION INDUSTRY CO., LTD.: COMPANY OVERVIEW

- TABLE 317 SUGON INFORMATION INDUSTRY CO., LTD.: PRODUCTS OFFERED

- TABLE 318 SUGON INFORMATION INDUSTRY CO., LTD.: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 319 SUGON INFORMATION INDUSTRY CO., LTD.: OTHER DEVELOPMENTS, FEBRUARY 2020-MARCH 2026

- TABLE 320 INSPUR CO., LTD.: COMPANY OVERVIEW

- TABLE 321 INSPUR CO., LTD.: PRODUCTS OFFERED

- TABLE 322 NVENT: COMPANY OVERVIEW

- TABLE 323 NVENT: PRODUCTS OFFERED

- TABLE 324 NVENT: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 325 NVENT: EXPANSIONS, FEBRUARY 2020-MARCH 2026

- TABLE 326 TAISOL ELECTRONICS CO., LTD.: COMPANY OVERVIEW

- TABLE 327 TAISOL ELECTRONICS CO., LTD.: PRODUCTS OFFERED

- TABLE 328 ACCELSIUS LLC: COMPANY OVERVIEW

- TABLE 329 ACCELSIUS LLC: PRODUCTS OFFERED

- TABLE 330 REFROID TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 331 REFROID TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 332 REFROID TECHNOLOGIES: DEALS, FEBRUARY 2020-MARCH 2026

- TABLE 333 TEIMMERS: COMPANY OVERVIEW

- TABLE 334 KOOLANCE, INC.: COMPANY OVERVIEW

- TABLE 335 GIGA-BYTE TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 336 PEZY COMPUTING: COMPANY OVERVIEW

- TABLE 337 TAS: COMPANY OVERVIEW

- TABLE 338 OPTICOOL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 339 SEGUENTE INC.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 DATA CENTER LIQUID COOLING MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 GLOBAL DATA CENTER LIQUID COOLING MARKET, 2026-2033

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DATA CENTER LIQUID COOLING MARKET (2020-2025)

- FIGURE 5 DISRUPTIVE TRENDS IMPACTING GROWTH OF DATA CENTER LIQUID COOLING MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN DATA CENTER LIQUID COOLING MARKET

- FIGURE 7 NORTH AMERICA TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 8 RAPID ADOPTION OF AI, ML, AND BLOCKCHAIN TECHNOLOGIES TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 9 HYPERSCALE DATA CENTERS TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 10 BFSI TO SECURE LEADING POSITION DURING FORECAST PERIOD

- FIGURE 11 NORTH AMERICA TO DOMINATE GLOBAL DATA CENTER LIQUID COOLING MARKET

- FIGURE 12 CHINA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 13 DATA CENTER LIQUID COOLING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 14 COUNTRIES WITH HIGHEST NUMBER OF DATA CENTERS, 2022 AND 2024

- FIGURE 15 POWER DENSITIES, BY DEVELOPMENT TYPE (KW PER RACK)

- FIGURE 16 GLOBAL DATA CENTER POWER USAGE EFFECTIVENESS (PUE) 2007-2035

- FIGURE 17 LIQUID COOLING FOR HIGH-DENSITY RACKS AND IMMERSION COOLING FOR ABOVE 150 KW PER RACK

- FIGURE 18 REGIONAL SPENDING ON BLOCKCHAIN SOLUTIONS, 2022 (USD BILLION)

- FIGURE 19 DATA CENTER LIQUID COOLING MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 20 DATA CENTER LIQUID COOLING MARKET: VALUE CHAIN ANALYSIS

- FIGURE 21 DATA CENTER LIQUID COOLING MARKET: ECOSYSTEM ANALYSIS

- FIGURE 22 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 23 DATA CENTER LIQUID COOLING MARKET: INVESTMENT AND FUNDING RELATED TO STARTUPS/SMES, 2019-2024

- FIGURE 24 PATENT ANALYSIS, BY DOCUMENT TYPE, 2015-2025

- FIGURE 25 PATENT PUBLICATION TRENDS, 2015-2025

- FIGURE 26 DATA CENTER LIQUID COOLING MARKET: LEGAL STATUS OF PATENTS, JANUARY 2015-DECEMBER 2025

- FIGURE 27 JURISDICTION OF US REGISTERED HIGHEST SHARE OF PATENTS, 2015-2025

- FIGURE 28 TOP PATENT APPLICANTS, 2015-2025

- FIGURE 29 FUTURE APPLICATIONS OF DATA CENTER LIQUID COOLING MARKET

- FIGURE 30 DATA CENTER LIQUID COOLING MARKET: DECISION-MAKING FACTORS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END USER

- FIGURE 32 KEY BUYING CRITERIA, BY END USER

- FIGURE 33 ADOPTION BARRIERS & INTERNAL CHALLENGES

- FIGURE 34 SERVICES SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 35 DIRECT-TO-CHIP COOLING SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 36 SMALL & MID-SIZED DATA CENTERS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 37 HYPERSCALE DATA CENTERS SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 38 IT & TELECOM SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 39 NORTH AMERICA TO LEAD MARKET BY 2033

- FIGURE 40 NORTH AMERICA: DATA CENTER LIQUID COOLING MARKET SNAPSHOT

- FIGURE 41 ASIA PACIFIC: DATA CENTER LIQUID COOLING MARKET SNAPSHOT

- FIGURE 42 EUROPE: DATA CENTER LIQUID COOLING MARKET SNAPSHOT

- FIGURE 43 DATA CENTER LIQUID COOLING MARKET: REVENUE ANALYSIS OF KEY COMPANIES, 2020-2024 (USD BILLION)

- FIGURE 44 DATA CENTER LIQUID COOLING MARKET SHARE ANALYSIS, 2024

- FIGURE 45 DATA CENTER LIQUID COOLING MARKET: RANKING OF TOP FIVE PLAYERS, 2024

- FIGURE 46 DATA CENTER LIQUID COOLING MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 47 DATA CENTER LIQUID COOLING MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 48 DATA CENTER LIQUID COOLING MARKET: COMPANY FOOTPRINT

- FIGURE 49 DATA CENTER LIQUID COOLING MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 50 DATA CENTER LIQUID COOLING MARKET: COMPANY VALUATION, 2024 (EV/REVENUE)

- FIGURE 51 DATA CENTER LIQUID COOLING MARKET: FINANCIAL METRICS, 2024 (EV/EBITDA)

- FIGURE 52 DATA CENTER LIQUID COOLING MARKET: YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND FIVE-YEAR STOCK BETA OF KEY MANUFACTURERS, 2024

- FIGURE 53 VERTIV GROUP CORP.: COMPANY SNAPSHOT

- FIGURE 54 SUPER MICRO COMPUTER, INC.: COMPANY SNAPSHOT

- FIGURE 55 SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

- FIGURE 56 MODINE MANUFACTURING COMPANY: COMPANY SNAPSHOT

- FIGURE 57 DAIKIN INDUSTRIES, LTD.: COMPANY SNAPSHOT

- FIGURE 58 DELTA POWER SOLUTIONS: COMPANY SNAPSHOT

- FIGURE 59 WIWYNN CORPORATION: COMPANY SNAPSHOT

- FIGURE 60 KAORI HEAT TREATMENT CO., LTD.: COMPANY SNAPSHOT

- FIGURE 61 FLEX LTD.: COMPANY SNAPSHOT

- FIGURE 62 LENOVO: COMPANY SNAPSHOT

- FIGURE 63 INSPUR CO., LTD.: COMPANY SNAPSHOT

- FIGURE 64 NVENT: COMPANY SNAPSHOT

- FIGURE 65 TAISOL ELECTRONICS CO., LTD.: COMPANY SNAPSHOT

- FIGURE 66 DATA CENTER LIQUID COOLING MARKET: RESEARCH DESIGN

- FIGURE 67 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH & TOP-DOWN APPROACH

- FIGURE 68 MAIN MATRIX CONSIDERED TO ASSESS DEMAND FOR DATA CENTER LIQUID COOLING

- FIGURE 69 STEPS CONSIDERED TO ANALYZE SUPPLY IN DATA CENTER LIQUID COOLING MARKET

- FIGURE 70 DATA CENTER LIQUID COOLING MARKET: DATA TRIANGULATION