PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2029871

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2029871

OCP Rack Market By Application (AI, High-performance computing, Data Management, Enterprise Apps & Others), End User (Retail Colocation, Enterprise, Neocloud Providers, Others - Hyperscalers/Wholesale Colocation) - Global Forecast to 2030

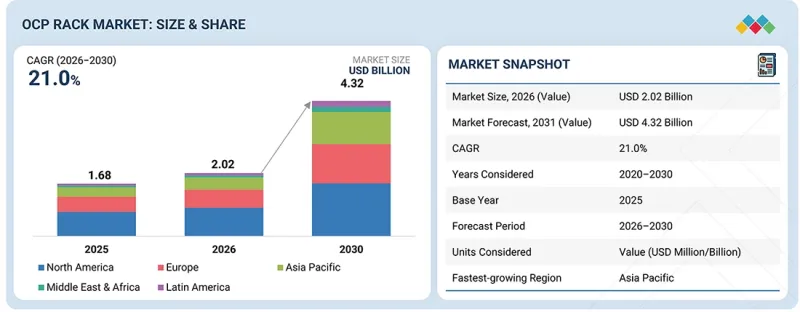

The OCP rack market is expanding rapidly, with the market projected to grow from USD 1.68 billion in 2025 to USD 4.32 billion by 2030, at a CAGR of 21.0%. The expansion of edge computing is emerging as a distinct driver for the OCP rack market, as data processing increasingly shifts closer to end users and devices. Edge facilities are typically space-constrained and require compact, efficient, and easily deployable infrastructure. OCP rack designs, developed under the Open Compute Project, support these requirements through simplified mechanical structures, modular configurations, and efficient power distribution.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2025 |

| Forecast Period | 2026-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Application, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

Unlike large hyperscale environments, edge deployments often prioritize rapid installation and operational consistency across multiple distributed sites. OCP-based racks enable standardized designs that can be replicated with minimal customization, reducing deployment time and integration complexity. In addition, the ability to support higher compute density within a smaller footprint aligns with edge requirements where real estate and power availability are limited. As edge use cases expand across telecom, content delivery, and industrial applications, demand for flexible and scalable rack solutions is expected to support increased adoption of OCP architectures.

"By application, the high-performance computing (HPC) is projected to be the second-fastest-growing in the market during the forecast period."

High-performance computing (HPC) is projected to be the second fastest-growing application in the OCP rack market, supported by increasing demand for compute-intensive workloads across research, enterprise, and industrial use cases. HPC environments require tightly integrated systems with high power density, low-latency networking, and efficient thermal management. OCP rack architectures address these requirements by supporting higher rack power capacities and enabling advanced cooling solutions, including liquid cooling. This allows operators to deploy dense compute clusters without exceeding facility constraints. In addition, HPC workloads often require repeatable and scalable infrastructure designs, which aligns with the standardized approach of OCP racks. As organizations expand simulation, modeling, and AI-assisted computing capabilities, the need for efficient and scalable HPC infrastructure is increasing, contributing to the accelerated adoption of OCP-based rack systems.

"By end user, the others segment is expected to hold the largest market value during the forecast period."

The "others" segment, comprising hyperscalers and wholesale colocation providers, is expected to hold the largest market value in the OCP rack market due to the scale and standardization of their infrastructure deployments. These operators build and operate large data center campuses designed for uniform, repeatable architectures, where OCP racks aligned with Open Compute Project standards provide clear advantages in terms of efficiency and scalability. Hyperscalers deploy OCP-based systems to support high-density workloads, particularly for AI and cloud services, while wholesale colocation providers adopt similar designs to meet the requirements of large tenants. Their ability to invest in custom facility design, including high-capacity power and liquid cooling infrastructure, further supports OCP adoption. Additionally, these players typically operate with long planning horizons and large capital budgets, enabling early adoption of new rack architectures. This combination of scale, standardization, and infrastructure readiness positions the segment as the largest contributor to OCP rack demand.

"North America leads the OCP rack market during the forecast."

North America is expected to hold the largest market value in the OCP rack market due to its concentration of hyperscale capacity, early adoption of open hardware standards, and continued investment in AI infrastructure. The region hosts major contributors to the Open Compute Project ecosystem, including large cloud providers that design and deploy OCP-based architectures at scale. These operators have already transitioned significant portions of their infrastructure to 21-inch Open Rack designs, enabling higher power density, efficient thermal management, and standardized deployments across multiple campuses.

The rapid expansion of AI training and inference clusters is driving the market as it requires rack-level optimization for power delivery and cooling, particularly with the increasing adoption of liquid cooling and high-capacity busbar systems. In parallel, wholesale colocation providers in North America are aligning new facility builds with OCP requirements to support hyperscale tenants, further reinforcing demand. The region is also seeing continued advancement in rack-scale integration, where compute, networking, and cooling are deployed as pre-integrated systems rather than discrete components. This reduces deployment timelines and operational complexity. Combined with strong supply chain presence across OEMs, ODMs, and infrastructure vendors, these factors position North America as the leading market for OCP rack deployments.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the OCP rack market.

- By Company: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: Directors - 35%, Managers - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 45%, Asia Pacific - 25%, Middle East & Africa - 3%, and Latin America - 2%.

The report includes a detailed study of key players operating in the OCP rack market. The major market participants covered in the study include Rittal (Germany), Dell Technologies (US), Sanmina Corporation (US), Legrand (France), Vertiv (US), Eaton (Ireland), Belden (US), Wiwynn Corporation (Taiwan), Lite-on Cloud Infrastructure (Taiwan), Cheval Group, Gigabyte (Taiwan), and Chatsworth Product (US).

Research Coverage

This research report categorizes the OCP rack market based on applications By Applications (AI (training & inference), high performance computing (HPC), data management and enterprise apps & others)), By end users (retail colocation providers, enterprise, necloud providers and others (hyperscalers/ wholesale colocation providers) and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope encompasses detailed insights into the key factors influencing the OCP rack market, including drivers, restraints, challenges, and opportunities shaping its growth. It provides a comprehensive analysis of leading vendors, covering their product portfolios, rack-scale capabilities, and alignment with standards defined by the Open Compute Project. The report also examines strategic initiatives such as partnerships with hyperscalers and ODMs, collaborations across the OCP ecosystem, product innovations in rack design, power and cooling integration, as well as mergers, acquisitions, and recent developments impacting the OCP rack market landscape.

Reason to Buy this Report

The report provides market leaders and new entrants with insights into the closest estimations of revenue for the overall OCP rack market and its subsegments. It enables stakeholders to understand the competitive landscape and gain actionable insights to better position their offerings and develop effective go-to-market strategies. Additionally, the report helps stakeholders assess market trends and dynamics by providing a detailed analysis of key drivers, restraints, challenges, and opportunities shaping the OCP rack market.

The report provides insights into the following points:

- The report provides insights into key drivers, restraints, opportunities, and challenges shaping the OCP rack market. Major drivers include AI rack power density exceeding driving OCP adoption, rack-scale integrated infrastructure replacing component-level deployments, and hyperscaler-led standardization accelerating global OCP adoption. Restraints include limited compatibility with legacy 19-inch rack infrastructure and high upfront redesign costs for facility power and cooling systems. Opportunities include integration of liquid cooling (D2C and immersion) within rack designs, pre-configured AI-ready rack solutions for hyperscale and neo-cloud players. Key challenges include interoperability issues in multi-vendor OCP ecosystems and legacy system complexity impacting deployment efficiency.

- Services Development/Innovation: Detailed insight into upcoming technologies, research & development activities, and new product & service launches in the OCP rack market

- Market Development: Comprehensive information about lucrative markets - the report analyses the OCP rack market across varied regions

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the OCP rack market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and OCP rack offerings of leading players such as Rittal (Germany), Dell Technologies (US), Sanmina Corporation (US), Legrand (France), Vertiv (US), Eaton (Ireland), Belden (US), Wiwynn Corporation (Taiwan), Lite-on Cloud Infrastructure (Taiwan), Cheval Group, Gigabyte (Taiwan), and Chatsworth Product (US). The report also helps stakeholders understand the OCP rack market by providing information on key drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 MARKET OVERVIEW

- 2.1 INTRODUCTION

- 2.2 MARKET DYNAMICS

- 2.2.1 DRIVERS

- 2.2.1.1 Adoption in high-density data center environments driven by AI rack power density

- 2.2.1.2 Rack-scale integration across high-density deployments

- 2.2.1.3 Hyperscale standardization

- 2.2.2 RESTRAINTS

- 2.2.2.1 Legacy 19-inch infrastructure limits broader OCP rack adoption in existing data centers

- 2.2.2.2 High facility redesign costs constrain OCP rack adoption in retrofit data center environments

- 2.2.3 OPPORTUNITIES

- 2.2.3.1 Liquid cooling integration to improve adoption opportunity in high-density AI infrastructure

- 2.2.3.2 Pre-configured AI rack systems among hyperscale and neocloud operators

- 2.2.4 CHALLENGES

- 2.2.4.1 Multi-vendor interoperability gaps increase deployment complexity in OCP environments

- 2.2.4.2 Thermal constraints at ultra-high rack densities challenge OCP scalability

- 2.2.1 DRIVERS

- 2.3 CASE STUDY ANALYSIS

- 2.3.1 MODERNIZED ENTERPRISE INFRASTRUCTURE WITH OCP-BASED PRIVATE CLOUD DEPLOYMENT

- 2.3.2 REDUCED DATA CENTER COST AND IMPROVED FLEXIBILITY WITH OPEN BRIDGE RACK ADOPTION

- 2.3.3 STRENGTHENED SCALABLE PRIVATE CLOUD DELIVERY WITH OCP-BASED INTEGRATED INFRASTRUCTURE

- 2.4 ANALYSIS: DOES RISING RACK POWER DENSITY STRUCTURALLY REDUCE RACK COUNTS?

- 2.5 ANALYSIS OF KW EVOLUTION OF 21" OCP RACKS BY 2030

- 2.5.1 LEGACY TO EARLY OCP FOUNDATION (PRE-2015 -> 2020 | 5-15 KW)

- 2.5.2 PHASE 2: CLOUD SCALING & EARLY AI TRANSITION (2020 -> 2023 | 15-40 KW)

- 2.5.3 PHASE 3: STANDARDIZED HIGH-DENSITY ORV3 ERA (2023 -> 2025 | 50-130 KW)

- 2.5.4 PHASE 4: ORV3 STRETCH PHASE (2025 -> 2026 | 130-200 KW+)

- 2.5.5 PHASE 5: TRANSITION TO HIGH-VOLTAGE ARCHITECTURES (2027 -> 2028 | 200-500 KW)

- 2.5.6 PHASE 6: ULTRA-HIGH-DENSITY AI RACKS (2028 -> 2030 | 500 KW-1 MW)

- 2.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 2.7 PRICING ANALYSIS

- 2.7.1 AVERAGE SELLING PRICE

- 2.7.2 INDICATIVE PRICING, BY VENDOR

3 21-INCH OCP RACK MARKET, BY END USER

- 3.1 INTRODUCTION

- 3.1.1 21 INCH OCP RACK, BY END USER: MARKET DRIVERS

- 3.2 RETAIL COLOCATION PROVIDERS

- 3.2.1 ABILITY TO SUPPORT HIGH-DENSITY DEPLOYMENTS IN SHARED DATA CENTER ENVIRONMENTS TO PROPEL GROWTH

- 3.3 ENTERPRISE (ON-PREMISES)

- 3.3.1 DRIVING ENTERPRISE INFRASTRUCTURE TRANSFORMATION THROUGH OCP ADOPTION TO FUEL GROWTH

- 3.4 NEOCLOUD PROVIDERS

- 3.4.1 ACCELERATING NEOCLOUD GROWTH THROUGH MODULAR OCP INFRASTRUCTURE TO DRIVE ADOPTION

- 3.5 OTHER END USERS

4 21-INCH OCP RACK MARKET, BY APPLICATION

- 4.1 INTRODUCTION

- 4.1.1 21 INCH OCP RACK, BY APPLICATION: MARKET DRIVERS

- 4.2 AI (TRAINING & INFERENCES)

- 4.2.1 ENABLING AI-SCALE TRAINING WITH HIGH-DENSITY OCP RACK ARCHITECTURES TO DRIVE GROWTH

- 4.3 HIGH-PERFORMANCE COMPUTING (HPC)

- 4.3.1 ENHANCING HPC EFFICIENCY WITH ADVANCED COOLING AND POWER SYSTEMS TO PROPEL GROWTH

- 4.4 DATA MANAGEMENT

- 4.4.1 SUPPORTING REAL-TIME DATA PROCESSING WITH OCP RACK SOLUTIONS TO DRIVE ADOPTION

- 4.5 ENTERPRISE APPS AND OTHERS

5 21-INCH OCP RACK MARKET, BY REGION

- 5.1 INTRODUCTION

- 5.2 NORTH AMERICA

- 5.2.1 US

- 5.2.1.1 Accelerating OCP rack adoption through hyperscale and AI expansion to boost market growth

- 5.2.2 CANADA

- 5.2.2.1 Growing emphasis on building scalable AI infrastructure through ecosystem collaboration to support market growth

- 5.2.1 US

- 5.3 EUROPE

- 5.3.1 UK

- 5.3.1.1 Enabling high-density AI workloads through 21-inch OCP rack deployments to propel growth

- 5.3.2 GERMANY

- 5.3.2.1 Leveraging OCP architectures to support liquid cooling and higher rack powers

- 5.3.3 FRANCE

- 5.3.3.1 Supporting gigawatt-scale AI data centers with high-density rack architectures to fuel growth

- 5.3.4 ITALY

- 5.3.4.1 Expanding data center investments to support OCP rack adoption in Italy

- 5.3.5 SPAIN

- 5.3.5.1 Increase in hyperscale activity, including large AI-focused deployments, to drive demand for high-density and scalable infrastructure

- 5.3.6 REST OF EUROPE

- 5.3.1 UK

- 5.4 ASIA PACIFIC

- 5.4.1 CHINA

- 5.4.1.1 Public cloud expansion supporting open rack deployment to propel growth

- 5.4.2 JAPAN

- 5.4.2.1 Japan strengthens OCP rack adoption through AI infrastructure design

- 5.4.3 INDIA

- 5.4.3.1 India supports OCP rack adoption through local infrastructure demand

- 5.4.4 REST OF ASIA PACIFIC

- 5.4.1 CHINA

- 5.5 MIDDLE EAST & AFRICA

- 5.5.1 GCC

- 5.5.1.1 Saudi Arabia

- 5.5.1.1.1 Saudi data center expansion to drive OCP rack demand

- 5.5.1.2 UAE

- 5.5.1.2.1 UAE hyperscale growth to increase OCP adoption potential

- 5.5.1.3 Rest of GCC

- 5.5.1.1 Saudi Arabia

- 5.5.2 SOUTH AFRICA

- 5.5.2.1 Improving rack power density and cooling efficiency with OCP designs to drive growth

- 5.5.3 REST OF MIDDLE EAST & AFRICA

- 5.5.1 GCC

- 5.6 LATIN AMERICA

- 5.6.1 BRAZIL

- 5.6.1.1 Brazil to strengthen open infrastructure with domestic OCP manufacturing

- 5.6.2 MEXICO

- 5.6.2.1 Mexico to standardize next-generation rack infrastructure for AI workloads

- 5.6.3 REST OF LATIN AMERICA

- 5.6.1 BRAZIL

6 COMPANY PROFILES

- 6.1 INTRODUCTION

- 6.2 KEY PLAYERS

- 6.2.1 SANMINA CORPORATION

- 6.2.1.1 Business overview

- 6.2.1.2 Products/Solutions/Services offered

- 6.2.1.3 Recent developments

- 6.2.1.3.1 Product launches and enhancements

- 6.2.1.3.2 Deals

- 6.2.1.4 MnM view

- 6.2.1.4.1 Right to win

- 6.2.1.4.2 Strategic choices

- 6.2.1.4.3 Weaknesses and competitive threats

- 6.2.2 DELL TECHNOLOGIES

- 6.2.2.1 Business overview

- 6.2.2.2 Products/Solutions/Services offered

- 6.2.2.2.1 Product launches and enhancements

- 6.2.2.3 MnM view

- 6.2.2.3.1 Right to win

- 6.2.2.3.2 Strategic choices

- 6.2.2.3.3 Weaknesses and competitive threats

- 6.2.3 WIWYNN

- 6.2.3.1 Business overview

- 6.2.3.2 Products/Solutions/Services offered

- 6.2.3.3 Recent developments

- 6.2.3.3.1 Product launches and enhancements

- 6.2.3.3.2 Deals

- 6.2.3.4 MnM view

- 6.2.3.4.1 Right to win

- 6.2.3.4.2 Strategic choices

- 6.2.3.4.3 Weaknesses and competitive threats

- 6.2.4 GIGABYTE

- 6.2.4.1 Business overview

- 6.2.4.2 Products/Solutions/Services offered

- 6.2.4.3 Recent developments

- 6.2.4.3.1 Product launches and enhancements

- 6.2.4.4 MnM view

- 6.2.4.4.1 Right to win

- 6.2.4.4.2 Strategic choices

- 6.2.4.4.3 Weaknesses and competitive threats

- 6.2.5 EATON

- 6.2.5.1 Business overview

- 6.2.5.2 Products/Solutions/Services offered

- 6.2.5.3 Recent developments

- 6.2.5.3.1 Product launches and enhancements

- 6.2.5.4 MnM view

- 6.2.5.4.1 Right to win

- 6.2.5.4.2 Strategic choices

- 6.2.5.4.3 Weaknesses and competitive threats

- 6.2.6 RITTAL

- 6.2.6.1 Business overview

- 6.2.6.2 Products/Solutions/Services offered

- 6.2.6.3 Recent developments

- 6.2.6.3.1 Product launches and enhancements

- 6.2.6.3.2 Deals

- 6.2.7 LEGRAND

- 6.2.7.1 Business overview

- 6.2.7.2 Products/Solutions/Services offered

- 6.2.7.3 Recent developments

- 6.2.7.3.1 Product launches and enhancements

- 6.2.8 RACK RENEW

- 6.2.8.1 Business overview

- 6.2.8.2 Products/Solutions/Services offered

- 6.2.8.3 Recent developments

- 6.2.8.3.1 Product launches and enhancements

- 6.2.9 BELDEN

- 6.2.9.1 Business overview

- 6.2.9.2 Products/Solutions/Services offered

- 6.2.10 CHEVAL GROUP

- 6.2.10.1 Business overview

- 6.2.10.2 Products/Solutions/Services offered

- 6.2.1 SANMINA CORPORATION

List of Tables

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES, 2020-2025

- TABLE 3 INDICATIVE PRICING, BY VENDOR, 2025 (USD)

- TABLE 4 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 5 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 6 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (THOUSAND UNITS)

- TABLE 7 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (THOUSAND UNITS)

- TABLE 8 21-INCH OCP RACK MARKET FOR RETAIL COLOCATION PROVIDERS, BY REGION, 2020-2025 (USD MILLION)

- TABLE 9 21-INCH OCP RACK MARKET FOR RETAIL COLOCATION PROVIDERS, BY REGION, 2026-2030 (USD MILLION)

- TABLE 10 21-INCH OCP RACK MARKET FOR ENTERPRISE (ON-PREMISES), BY REGION, 2020-2025 (USD MILLION)

- TABLE 11 21-INCH OCP RACK MARKET FOR ENTERPRISE (ON-PREMISES), BY REGION, 2026-2030 (USD MILLION)

- TABLE 12 21-INCH OCP RACK MARKET FOR NEOCLOUD, BY REGION, 2020-2025 (USD MILLION)

- TABLE 13 21-INCH OCP RACK MARKET FOR NEOCLOUD, BY REGION, 2026-2030 (USD MILLION)

- TABLE 14 21-INCH OCP RACK MARKET FOR OTHERS, BY REGION, 2020-2025 (USD MILLION)

- TABLE 15 21-INCH OCP RACK MARKET FOR OTHERS, BY REGION, 2026-2030 (USD MILLION)

- TABLE 16 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 17 21-INCH OCP RACK MARKET, BY APPLICATIONS, 2026-2030 (USD MILLION)

- TABLE 18 21-INCH OCP RACK MARKET FOR AI (TRAINING & INFERENCE), BY REGION, 2020-2025 (USD MILLION)

- TABLE 19 21-INCH OCP RACK MARKET FOR AI (TRAINING & INFERENCE), BY REGION, 2026-2030 (USD MILLION)

- TABLE 20 21-INCH OCP RACK MARKET FOR HIGH-PERFORMANCE COMPUTING (HPC), BY REGION, 2020-2025 (USD MILLION)

- TABLE 21 21-INCH OCP RACK MARKET FOR HIGH-PERFORMANCE COMPUTING (HPC), BY REGION, 2026-2030 (USD MILLION)

- TABLE 22 21-INCH OCP RACK MARKET FOR DATA MANAGEMENT, BY REGION, 2020-2025 (USD MILLION)

- TABLE 23 21-INCH OCP RACK MARKET FOR DATA MANAGEMENT, BY REGION, 2026-2030 (USD MILLION)

- TABLE 24 21-INCH OCP RACK MARKET FOR ENTERPRISE APPS & OTHERS, BY REGION, 2020-2025 (USD MILLION)

- TABLE 25 21-INCH OCP RACK MARKET FOR ENTERPRISE APPS & OTHERS, 2026-2030 (USD MILLION)

- TABLE 26 21-INCH OCP RACK MARKET, BY REGION, 2020-2025 (USD MILLION)

- TABLE 27 21-INCH OCP RACK MARKET, BY REGION, 2026-2030 (USD MILLION)

- TABLE 28 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 29 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 30 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 31 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 32 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 33 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 34 US: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 35 US: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 36 CANADA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 37 CANADA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 38 EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 39 EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 40 EUROPE: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 41 EUROPE: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 42 EUROPE: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 43 EUROPE: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 44 UK: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 45 UK: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 46 GERMANY: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 47 GERMANY: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 48 FRANCE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 49 FRANCE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 50 ITALY: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 51 ITALY: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 52 SPAIN: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 53 SPAIN: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 54 REST OF EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 55 REST OF EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 56 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 57 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 58 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 59 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 60 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 61 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 62 CHINA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 63 CHINA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 64 JAPAN: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 65 JAPAN: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 66 INDIA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 67 INDIA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 68 REST OF ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 69 REST OF ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 70 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 71 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 72 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 73 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 74 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 75 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 76 GCC: 21 INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 77 GCC: 21 INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 78 GCC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 79 GCC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 80 SAUDI ARABIA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 81 SAUDI ARABIA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 82 UAE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 83 UAE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 84 REST OF GCC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 85 REST OF GCC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 86 SOUTH AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 87 SOUTH AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 88 REST OF MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 89 REST OF MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 90 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 91 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 92 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATIONS, 2020-2025 (USD MILLION)

- TABLE 93 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATIONS, 2026-2030 (USD MILLION)

- TABLE 94 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 95 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 96 BRAZIL: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 97 BRAZIL: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 98 MEXICO: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 99 MEXICO: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 100 REST OF LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 101 REST OF LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 102 SANMINA CORPORATION: COMPANY OVERVIEW

- TABLE 103 SANMINA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 104 SANMINA CORPORATION: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 105 SANMINA CORPORATION: DEALS

- TABLE 106 DELL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 107 DELL TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 108 DELL TECHNOLOGIES: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 109 WIWYNN: COMPANY OVERVIEW

- TABLE 110 WIWYNN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 111 WIWYNN: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 112 WIWYNN: DEALS

- TABLE 113 GIGABYTE: COMPANY OVERVIEW

- TABLE 114 GIGABYTE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 115 GIGABYTE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 116 EATON: COMPANY OVERVIEW

- TABLE 117 EATON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 118 EATON: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 119 RITTAL: COMPANY OVERVIEW

- TABLE 120 RITTAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 121 RITTAL: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 122 RITTAL: DEALS

- TABLE 123 LEGRAND: COMPANY OVERVIEW

- TABLE 124 LEGRAND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 125 LEGRAND: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 126 RACK RENEW: COMPANY OVERVIEW

- TABLE 127 RACK RENEW: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 128 RACK RENEW: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 129 BELDEN: COMPANY OVERVIEW

- TABLE 130 BELDEN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 131 CHEVAL GROUP: COMPANY OVERVIEW

- TABLE 132 CHEVAL GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

List of Figures

- FIGURE 1 OCP RACK MARKET SEGMENTATION

- FIGURE 2 STUDY YEARS CONSIDERED

- FIGURE 3 OCP RACK MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 5 AVERAGE SELLING PRICE, 2020-2025 (USD)

- FIGURE 6 OTHERS TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 7 AI (TRAINING & INFERENCE) TO BE LARGEST APPLICATION OF OCP RACKS DURING FORECAST PERIOD

- FIGURE 8 NORTH AMERICA TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 9 NORTH AMERICA: OCP RACK MARKET SNAPSHOT

- FIGURE 10 ASIA PACIFIC: OCP RACK MARKET SNAPSHOT

- FIGURE 11 SANMINA CORPORATION: COMPANY SNAPSHOT

- FIGURE 12 DELL TECHNOLOGIES: COMPANY SNAPSHOT

- FIGURE 13 WIWYNN: COMPANY SNAPSHOT

- FIGURE 14 GIGABYTE: COMPANY SNAPSHOT

- FIGURE 15 EATON: COMPANY SNAPSHOT

- FIGURE 16 LEGRAND: COMPANY SNAPSHOT

- FIGURE 17 BELDEN: COMPANY SNAPSHOT