PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2060322

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2060322

Electronic Toll Collection Market by Technology (GNSS/GPS), Offering (Hardware, Software, Services), Type (Open Road Tolling, Barrier-based ETC, Hybrid Systems), Application (Bridges & Tunnels), and Region - Global Forecast to 2032

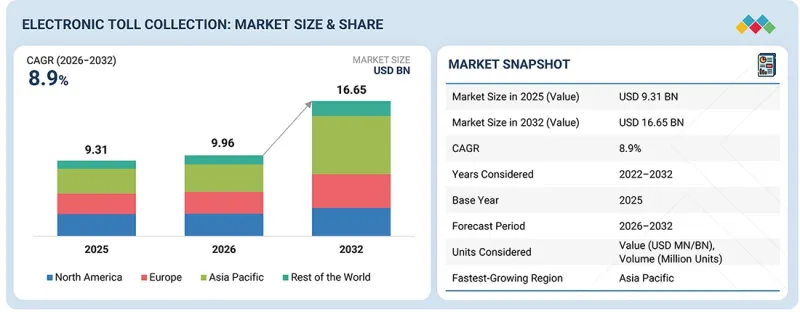

The global electronic toll collection market is projected to grow from USD 9.31 billion in 2025 to USD 16.65 billion by 2032 at a CAGR of 8.9% during the forecast period. Market growth is being driven by increasing investments in intelligent transportation infrastructure, growing demand for frictionless vehicle movement, and rising adoption of digital toll payment ecosystems across highways, urban corridors, bridges, and tunnels.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Technology, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

The transition toward automated and barrier-free toll collection systems is accelerating the deployment of technologies such as RFID, GNSS, automatic number plate recognition (ANPR), and cloud-based toll management platforms.

Additionally, the increasing focus on reducing traffic congestion, improving toll revenue efficiency, and enhancing commuter convenience is supporting large-scale ETC implementation. Continuous advancements in connected mobility, real-time analytics, AI-enabled traffic management, and interoperable payment systems are further strengthening scalability and operational performance, while growing investments in smart city infrastructure and integrated transportation networks are expanding deployment opportunities, positioning electronic toll collection as a critical enabler of next-generation intelligent mobility and road infrastructure modernization.

"The ANPR cameras segment is projected to grow at the highest CAGR during the forecast period."

The ANPR cameras segment for electronic toll collection is projected to achieve the highest CAGR during the forecast period. This growth is supported by the increasing adoption of free-flow and barrier-free tolling systems that require accurate, real-time vehicle identification capabilities. ANPR camera technologies enable automatic capture and recognition of vehicle license plates, supporting seamless toll transactions without requiring physical tags or vehicle stoppage. These systems are increasingly being integrated into highways, urban road pricing networks, bridges, and smart transportation corridors to improve toll collection efficiency, traffic throughput, and enforcement accuracy. Additionally, rising demand for interoperable tolling infrastructure, violation management, and automated vehicle classification is accelerating innovation in camera systems, edge processing, and AI-based image analytics. Growing investments in intelligent transportation systems, cloud-connected toll platforms, and digital mobility infrastructure are further driving deployment. Continuous advancements in imaging performance, analytics software, and system integration capabilities are enabling scalable implementation and operational optimization, positioning the ANPR cameras segment as a key growth driver in the electronic toll collection market.

"Transaction Processing Software is projected to account for a significant share of the ETC market in 2025."

Transaction Processing Software is projected to account for the highest market share of the electronic toll collection market in 2032. This growth is driven by increasing deployment of digital tolling infrastructure and the rising need for real-time, secure, and high-volume transaction management across toll networks. Transaction processing software serves as the operational backbone of ETC systems by enabling toll calculation, payment authorization, account management, interoperability, reconciliation, and centralized data processing. There is strong adoption of tolling systems across highways, urban tolling programs, bridges, and open-road environments, accelerating their deployment as transportation authorities aim to improve both operational efficiency and the user experience. These platforms enable faster transaction execution, seamless integration with RFID, GNSS, and ANPR technologies, and greater toll revenue accuracy than conventional toll collection approaches. Additionally, advancements in cloud architecture, AI-enabled analytics, cybersecurity capabilities, and integrated payment ecosystems are expanding software functionality and enabling scalable deployment in complex, high-traffic transportation environments.

"The US is projected to capture the largest share in the ETC market in 2032."

The US is projected to capture the largest share in the electronic toll collection market in 2032, supported by the extensive deployment of electronic and cashless tolling infrastructure across highways, bridges, and urban mobility corridors. The country benefits from early adoption of open road tolling, strong investments in intelligent transportation systems, and growing implementation of RFID, ANPR, and cloud-based toll management platforms. Increasing focus on reducing traffic congestion, improving toll collection efficiency, and enhancing commuter convenience is accelerating ETC adoption across transportation networks. Additionally, the presence of established toll operators, continuous infrastructure modernization initiatives, and integration of AI-driven traffic analytics and digital payment ecosystems continue to strengthen the US position as a leading market for electronic toll collection globally.

Extensive primary interviews were conducted with key industry experts in the electronic toll collection market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type - Tier 1-35%, Tier 2-45%, Tier 3 -20%

By Designation- C-level Executives - 40%, Directors - 30%, Others - 30%

By Region North America - 40%, Europe - 30%, Asia Pacific - 20%, RoW - 10%

The electronic toll collection market is dominated by a few globally established players, such as Kapsch TrafficCom AG (Austria), Conduent Incorporated (US), ST Engineering (TransCore) (Singapore), Thales (France), and Siemens (Germany).

Research Coverage:

The report segments the electronic toll collection market and forecasts its size by application (highways, urban areas), type (transponder/tag-based tolling systems, other types), offering (hardware, back-office & other services), and technology (RFID, DSRC, other technologies). It also discusses the market's drivers, restraints, opportunities, and challenges. It gives a detailed view of the market across regions (North America, Europe, Asia Pacific, RoW). The report includes a supply chain analysis of key players and a competitive analysis of the electronic toll collection ecosystem.

Key Benefits of Buying the Report:

Analysis of key drivers (Urgent need to mitigate traffic congestion and reduce road accidents, strong government support to deploy advanced tolling solutions, high convenience of automated toll payment options, technological advancements in transportation infrastructure), restraints (overreliance on technologies and susceptibility to technical failure, ETC implementation constraints in developing countries, requirement for high initial investments in GPS- and GNSS-based ETC systems), opportunities (significant focus on minimizing fuel consumption and emissions for economic and environmental gains, integration of blockchain technology into toll collection systems, rising number of public-private partnership agreements in transportation sector, increasing adoption of all-electronic tolling systems), and challenges (data privacy concerns, interoperability issues associated with tolling systems)

Service Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and new product launches in the electronic toll collection market

Market Development: Comprehensive information about lucrative markets - the report analyses the electronic toll collection market across varied regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the electronic toll collection market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Kapsch TrafficCom AG (Austria), Conduent Incorporated (US), ST Engineering (TransCore) (US), Thales (France), Cubic Corporation (US), Siemens (Germany), EFKON GmbH (Austria), Neology, Inc. (US), FEIG ELECTRONIC (Germany), and Q-Free (Norway), among others in the electronic toll collection market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 UNIT CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ELECTRONIC TOLL COLLECTION MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRONIC TOLL COLLECTION MARKET

- 3.2 ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY

- 3.3 ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING

- 3.4 ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE

- 3.5 ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION

- 3.6 ELECTRONIC TOLL COLLECTION MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Urgent need to mitigate traffic congestion and reduce road accidents

- 4.2.1.2 Strong government support to deploy advanced tolling solutions across highways and urban areas

- 4.2.1.3 High convenience of automated toll payment options

- 4.2.1.4 Technological advancements in transportation infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 Susceptibility of ETC solutions to technical failures and vulnerability to cybertattacks

- 4.2.2.2 Implementation constraints in developing countries

- 4.2.2.3 Requirement for high initial investments in GPS- and GNSS-based ETC systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Significant focus on minimizing fuel consumption and emissions for economic and environmental gains

- 4.2.3.2 Integration of blockchain technology into toll collection systems

- 4.2.3.3 Rising number of public-private partnership agreements in transportation sector

- 4.2.3.4 Increasing adoption of all-electronic tolling systems

- 4.2.4 CHALLENGES

- 4.2.4.1 Data privacy concerns

- 4.2.4.2 Interoperability issues associated with tolling systems

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ELECTRONIC TOLL COLLECTION INDUSTRY

- 5.2.4 TRENDS IN ROADWAY TRANSPORTATION INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF RFID TAGS AND READERS, BY KEY PLAYER, 2022-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF ELECTRONIC TOLL COLLECTION SYSTEMS, BY REGION, 2022-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8530)

- 5.6.2 EXPORT SCENARIO (HS CODE 8530)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 WESTERN DIGITAL AND THEOBROMA SYSTEMS PROVIDES CUSTOMIZED TOLL COLLECTION SYSTEM FOR EUROPEAN PROJECT

- 5.10.2 SICE UPGRADES HUMBER BRIDGE TOLLING SYSTEM FOR OPTIMIZED TRAFFIC MANAGEMENT AND REVENUE GENERATION

- 5.10.3 MASSACHUSETTS DEPARTMENT OF TRANSPORTATION SELECTED TRANSCORE FOR E-ZPASS CUSTOMER SERVICE ENHANCEMENT

- 5.10.4 ERC SELECTS CLOUD-BASED TOLLING SOLUTION FROM COGNIZANT TO MAXIMIZE REVENUE

- 5.10.5 PLUS MALAYSIA USES TAPWAY'S AI AND NVIDIA'S GPUS IN RFID TOLL TRACKING SYSTEM BASED ON ANPR TECHNOLOGY

- 5.11 IMPACT OF US TARIFF - OVERVIEW

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON APPLICATION

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 GNSS/GPS-BASED TOLLING SYSTEMS

- 6.1.2 AI-POWERED TRAFFIC ANALYTICS AND AUTOMATED ENFORCEMENT

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 IOT SENSORS AND ROADSIDE UNITS

- 6.2.2 CYBERSECURITY SOLUTIONS

- 6.2.3 BIG DATA ANALYTICS PLATFORMS

- 6.2.4 DIGITAL PAYMENT AND FINTECH INTEGRATION

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI/GEN AI ON ELECTRONIC TOLL COLLECTION MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY OEMS IN ELECTRONIC TOLL COLLECTION MARKET

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN ELECTRONIC TOLL COLLECTION MARKET

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ELECTRONIC TOLL COLLECTION MARKET

7 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

9 PAYMENT METHODS ADOPTED TO PAY TOLLS

- 9.1 INTRODUCTION

- 9.2 PREPAID

- 9.3 POST-PAID

10 TOLLING ARCHITECTURES DEPLOYED IN ELECTRONIC TOLL COLLECTION

- 10.1 INTRODUCTION

- 10.2 HARDWARE PROVIDERS

- 10.3 SOFTWARE & PLATFORM PROVIDERS

- 10.4 SYSTEM INTEGRATORS

- 10.5 TOLL OPERATORS/CONCESSIONAIRES

- 10.6 MANAGED SERVICE PROVIDERS

11 ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE

- 11.1 INTRODUCTION

- 11.2 OPEN ROAD TOLLING (ORT)

- 11.2.1 INCLINATION TOWARD REDUCING CONGESTION AND IMPROVING FUEL EFFICIENCY TO BOOST ADOPTION

- 11.3 BARRIER-BASED ETC

- 11.3.1 LOW DEPLOYMENT COMPLEXITY AND HIGH TRANSACTION ACCURACY TO ACCELERATE IMPLEMENTATION

- 11.4 HYBRID SYSTEMS

- 11.4.1 GROWING EMPHASIS ON DIGITAL PAYMENTS AND SMART MOBILITY INITIATIVES TO DRIVE INSTALLATION

12 ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 RFID

- 12.2.1 EASY INTEGRATION INTO ANY INFRASTRUCTURE AND LOW OPERATING COST TO FUEL SEGMENTAL GROWTH

- 12.3 DSRC

- 12.3.1 GROWING DEMAND FOR SECURE AND PRIVACY-CENTRIC ETC SOLUTIONS TO FOSTER SEGMENTAL GROWTH

- 12.4 GNSS/GPS

- 12.4.1 SUPPORT FOR DISTANCE-BASED CHARGING WITHOUT EXTENSIVE ROADSIDE INFRASTRUCTURE TO BOOST MARKET

- 12.5 OTHER TECHNOLOGIES

13 ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING

- 13.1 INTRODUCTION

- 13.2 HARDWARE

- 13.2.1 ROADSIDE INFRASTRUCTURE

- 13.2.1.1 Growing preference for automated mobility environments to create roadside infrastructure requirements

- 13.2.2 ANPR CAMERAS

- 13.2.2.1 Increasing adoption of open road tolling and congestion management programs to facilitate segmental growth

- 13.2.3 RFID/DSRC READERS

- 13.2.3.1 Increasing demand for low-latency tolling and traffic management systems to augment segmental growth

- 13.2.4 TRANSPONDERS/OBUS

- 13.2.4.1 Expansion of national and regional interoperability initiatives to stimulate segmental growth

- 13.2.5 SENSORS & CONTROLLERS

- 13.2.5.1 Potential to improve detection accuracy and system visibility to promote segmental growth

- 13.2.1 ROADSIDE INFRASTRUCTURE

- 13.3 SOFTWARE

- 13.3.1 TRANSACTION PROCESSING

- 13.3.1.1 Rising investments in high-speed, low-latency processing infrastructure to contribute to segmental growth

- 13.3.2 VIOLATION ENFORCEMENT

- 13.3.2.1 Need to identify and manage unpaid toll transactions to promote segmental growth

- 13.3.3 TOLL MANAGEMENT

- 13.3.3.1 Surging deployment of multi-corridor toll networks and interoperable transportation infrastructure to accelerate segmental growth

- 13.3.4 REVENUE MANAGEMENT

- 13.3.4.1 Requirement to identify leakage points and optimize collection efficiency to encourage market expansion

- 13.3.5 INTEROPERABILITY PLATFORMS

- 13.3.5.1 Ability to facilitate transaction exchange, account synchronization, payment coordination, across toll operators to boost deployment

- 13.3.1 TRANSACTION PROCESSING

- 13.4 SERVICES

- 13.4.1 MANAGED SERVICES

- 13.4.1.1 Elevating use of performance-based delivery models to promote segmental growth

- 13.4.2 INTEGRATION & DEPLOYMENT

- 13.4.2.1 Increasing adoption of multi-technology toll environments to contribute to segmental growth

- 13.4.3 MAINTENANCE & SUPPORT

- 13.4.3.1 Necessity to maintain compliance with operational requirements and service-level agreements to encourage segmental growth

- 13.4.4 CONSULTING

- 13.4.4.1 Growing complexity of tolling environments to create need for consulting services

- 13.4.1 MANAGED SERVICES

14 ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 HIGHWAYS/EXPRESSWAYS

- 14.2.1 URGENT NEED TO IMPROVE TRAFFIC FLOW AND REDUCE CONGESTION AND HARMFUL EMISSIONS ACROSS HIGHWAYS TO UPTAKE GROWTH

- 14.3 URBAN CONGESTION CHARGING

- 14.3.1 SMART CITY DEVELOPMENT INITIATIVES TO SPUR DEMAND

- 14.4 BRIDGES & TUNNELS

- 14.4.1 GROWING ADOPTION OF AUTOMATED TOLLING ACROSS BRIDGES AND TUNNELS TO FACILITATE SEGMENTAL GROWTH

- 14.5 CROSS-BORDER TOLLING

- 14.5.1 INCREASING INTERNATIONAL TRANSPORTATION CONNECTIVITY AND REGIONAL MOBILITY PROGRAMS TO DRIVE SEGMENTAL GROWTH

15 ELECTRONIC TOLL COLLECTION MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Growing emphasis on modernizing road infrastructure to accelerate market growth

- 15.2.2 CANADA

- 15.2.2.1 Rising installation of ETC systems on major highways and bridges to drive market

- 15.2.3 MEXICO

- 15.2.3.1 Increasing number of projects for connecting with neighboring countries to contribute to market growth

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 UK

- 15.3.1.1 Adoption of advanced tolling technologies to enhance traffic efficiency to fuel market growth

- 15.3.2 GERMANY

- 15.3.2.1 Strong technological expertise and advanced tolling infrastructure to support market growth

- 15.3.3 FRANCE

- 15.3.3.1 Rising deployment of electronic tolling in environmental charging zones to reinforce market growth

- 15.3.4 ITALY

- 15.3.4.1 Expanding toll road network and digitally enabled heavy-vehicle tolling to contribute to market growth

- 15.3.5 SPAIN

- 15.3.5.1 Surging installation of automated and MLFF-ready ETC solutions across highways to foster market growth

- 15.3.6 NORDICS

- 15.3.6.1 Advancing digital road-charging through GNSS, ANPR, and eco-focused pricing models to drive market

- 15.3.7 NORWAY

- 15.3.7.1 HIGH adoption of free-flow tolling and digital mobility infrastructure to strengthen market expansion

- 15.3.8 REST OF EUROPE

- 15.3.1 UK

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Rising government support for automating toll payments to augment market growth

- 15.4.2 JAPAN

- 15.4.2.1 Increasing need to reduce traffic at toll gates to fuel market growth

- 15.4.3 SOUTH KOREA

- 15.4.3.1 Expansion of smart mobility initiatives and digital transportation programs to spur demand

- 15.4.4 AUSTRALIA

- 15.4.4.1 Leveraging free-flow tolling to improve urban mobility and transport efficiency to support market growth

- 15.4.5 SINGAPORE

- 15.4.5.1 Pioneering urban-centric digital tolling through GNSS-based ERP framework to foster market growth

- 15.4.6 INDIA

- 15.4.6.1 Accelerating nationwide toll digitization through RFID expansion and expressway development projects to expedite market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 ROW

- 15.5.1 SOUTH AMERICA

- 15.5.1.1 Brazil

- 15.5.1.1.1 Transition toward automated and free-flow toll collection environments to improve traffic throughput to drive market

- 15.5.1.2 Argentina

- 15.5.1.2.1 Greater adoption of digital toll collection models supported by infrastructure upgrades to propel market

- 15.5.1.3 Rest of South America

- 15.5.1.1 Brazil

- 15.5.2 MIDDLE EAST & AFRICA

- 15.5.2.1 GCC countries

- 15.5.2.1.1 Government initiatives to regulate traffic and curb over-speeding to support market growth

- 15.5.2.2 Rest of Middle East & Africa

- 15.5.2.1 GCC countries

- 15.5.1 SOUTH AMERICA

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2021-2026

- 16.2.1 PRODUCT PORTFOLIO

- 16.2.2 REGIONAL FOCUS

- 16.2.3 MANUFACTURING FOOTPRINT

- 16.2.4 ORGANIC/INORGANIC GROWTH STRATEGIES

- 16.3 MARKET SHARE ANALYSIS, 2025

- 16.4 REVENUE ANALYSIS, 2021-2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND COMPARISON

- 16.6.1 KAPSCH TRAFFICCOM AG (AUSTRIA)

- 16.6.2 CONDUENT, INC. (US)

- 16.6.3 ST ENGINEERING (TRANSCORE) (US)

- 16.6.4 THALES GROUP (FRANCE)

- 16.6.5 SIEMENS AG (GERMANY)

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Offering footprint

- 16.7.5.4 Tolling architecture footprint

- 16.7.5.5 Technology footprint

- 16.7.5.6 Application footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 16.9.2 DEALS

- 16.9.3 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 KAPSCH TRAFFICCOM AG

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Expansions

- 17.1.1.3.4 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths/Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses/Competitive threats

- 17.1.2 CONDUENT INCORPORATED

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths/Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses/Competitive threats

- 17.1.3 EFKON GMBH

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Other developments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths/Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses/Competitive threats

- 17.1.4 ST ENGINEERING (TRANSCORE)

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Expansions

- 17.1.4.3.4 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths/Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses/Competitive threats

- 17.1.5 THALES

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Other developments

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths/Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses/Competitive threats

- 17.1.6 SIEMENS

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.7 Q-FREE

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Services/Solutions offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Developments

- 17.1.8 CUBIC CORPORATION

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.9 NEOLOGY

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Deals

- 17.1.9.3.3 Other developments

- 17.1.10 FEIG ELECTRONIC

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.11 TOSHIBA CORPORATION,

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.12 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Developments

- 17.1.13 QUARTERHILL INC.

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product launches

- 17.1.13.3.2 Deals

- 17.1.13.3.3 Other developments

- 17.1.14 PERCEPTICS, LLC

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Solutions/Services offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Product launches

- 17.1.15 SKYTOLL

- 17.1.15.1 Business overview

- 17.1.15.2 Products/Solutions/Services offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Expansions

- 17.1.15.3.2 Other developments

- 17.1.1 KAPSCH TRAFFICCOM AG

- 17.2 OTHER PLAYERS

- 17.2.1 EMOVIS

- 17.2.2 STAR SYSTEMS INTERNATIONAL

- 17.2.3 GEA

- 17.2.4 ADAPTIVE RECOGNITION INC.

- 17.2.5 SICE

- 17.2.6 JENOPTIK

- 17.2.7 FAR EASTERN GROUP

- 17.2.8 TOLL COLLECT GMBH

- 17.2.9 GEOTOLL

- 17.2.10 INDRA

- 17.2.11 KISTLER GROUP

- 17.2.12 VERRA MOBILITY

- 17.3 CONCESSIONAIRES

- 17.3.1 VINCI HIGHWAYS

- 17.3.2 TRANSURBAN GROUP

- 17.3.3 ABERTIS

- 17.3.4 EGIS

- 17.3.5 ROADIS

- 17.3.6 IRB INFRASTRUCTURE DEVELOPERS LTD.

18 RESEARCH METHODOLOGY

- 18.1 INTRODUCTION

- 18.2 RESEARCH DATA

- 18.2.1 SECONDARY DATA

- 18.2.1.1 Key data from secondary sources

- 18.2.2 PRIMARY DATA

- 18.2.2.1 Primary interview participants

- 18.2.2.2 Breakdown of primaries

- 18.2.2.3 Key data from primary sources

- 18.2.2.4 Key industry insights

- 18.2.1 SECONDARY DATA

- 18.3 FACTOR ANALYSIS

- 18.3.1 SUPPLY-SIDE ANALYSIS

- 18.3.2 DEMAND-SIDE ANALYSIS

- 18.4 MARKET SIZE ESTIMATION METHODOLOGY

- 18.4.1 BOTTOM-UP APPROACH

- 18.4.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 18.4.2 TOP-DOWN APPROACH

- 18.4.2.1 Approach to arrive at market size using top-down approach (supply side)

- 18.4.3 GROWTH PROJECTION AND FORECAST-RELATED ASSUMPTIONS

- 18.4.1 BOTTOM-UP APPROACH

- 18.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.6 RESEARCH ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

- 18.8 RISK ASSESSMENT

19 APPENDIX

- 19.1 INSIGHTS FROM INDUSTRY EXPERTS

- 19.2 DISCUSSION GUIDE

- 19.3 KNOWLEDGE STORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.4 CUSTOMIZATION OPTIONS

- 19.5 RELATED REPORTS

- 19.6 AUTHOR DETAILS

List of Tables

- TABLE 1 REPORT INCLUSIONS AND EXCLUSIONS

- TABLE 2 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- TABLE 3 STRATEGIC FOCUS OF KEY COMPANIES AND ACTION TAKEN BY THEM

- TABLE 4 PORTER'S FIVE FORCES ANALYSIS

- TABLE 5 GDP PERCENTAGE CHANGE, BY COUNTRY, 2021-2030

- TABLE 6 ROLE OF COMPANIES IN ELECTRONIC TOLL COLLECTION ECOSYSTEM

- TABLE 7 AVERAGE SELLING PRICE TREND OF RFID TAGS AND READERS PROVIDED BY KEY PLAYERS, 2022-2025 (USD)

- TABLE 8 AVERAGE SELLING PRICE TREND OF ELECTRONIC TOLL COLLECTION SYSTEMS, BY REGION, 2022-2025 (USD)

- TABLE 9 IMPORT DATA FOR HS CODE 8530-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 10 EXPORT DATA FOR HS CODE 8530-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 11 LIST OF KEY CONFERENCES AND EVENTS, 2026

- TABLE 12 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 13 ELECTRONIC TOLL COLLECTION MARKET: TECHNOLOGY ROADMAP

- TABLE 14 LIST OF MAJOR PATENTS, 2022-2024

- TABLE 15 KEY USE CASES AND MARKET POTENTIAL

- TABLE 16 BEST PRACTICES: COMPANIES IMPLEMENTING AI AND OTHER ADVANCED TECHNOLOGIES

- TABLE 17 ELECTRONIC TOLL COLLECTION MARKET: CASE STUDIES RELATED TO AI IMPLEMENTATION

- TABLE 18 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 19 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 STANDARDS: ELECTRONIC TOLL COLLECTION

- TABLE 24 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR APPLICATIONS

- TABLE 25 KEY BUYING CRITERIA FOR APPLICATIONS

- TABLE 26 UNMET NEEDS IN ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION

- TABLE 27 ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2022-2025 (USD MILLION)

- TABLE 28 ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2026-2032 (USD MILLION)

- TABLE 29 OPEN ROAD TOLLING (ORT): ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 30 OPEN ROAD TOLLING (ORT): ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 31 BARRIER-BASED ETC: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 32 BARRIER-BASED ETC: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 33 HYBRID SYSTEMS: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 34 HYBRID SYSTEMS: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 35 ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 36 ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 37 RFID TAGS: ELECTRONIC TOLL COLLECTION MARKET, 2022-2025 (MILLION UNITS)

- TABLE 38 RFID TAGS: ELECTRONIC TOLL COLLECTION MARKET, 2026-2032 (MILLION UNITS)

- TABLE 39 ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 40 ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 41 HARDWARE: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 42 HARDWARE: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 43 HARDWARE: ELECTRONIC TOLL COLLECTION MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 44 HARDWARE: ELECTRONIC TOLL COLLECTION MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 45 SOFTWARE: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 46 SOFTWARE: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 47 SOFTWARE: ELECTRONIC TOLL COLLECTION MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 48 SOFTWARE: ELECTRONIC TOLL COLLECTION MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 49 SERVICES: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 50 SERVICES: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 51 SERVICES: ELECTRONIC TOLL COLLECTION MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 52 SERVICES: ELECTRONIC TOLL COLLECTION MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 53 ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 54 ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 55 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 56 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 57 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 58 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 59 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 60 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 61 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 62 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 63 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 64 HIGHWAYS/EXPRESSWAYS: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 65 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 66 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 67 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 68 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 69 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 70 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 71 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 72 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 73 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 74 URBAN CONGESTION CHARGING: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 75 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 76 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 77 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 78 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 79 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 80 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 81 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 82 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 83 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 84 BRIDGES & TUNNELS: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 85 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 86 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 87 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 88 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 89 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 90 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 91 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 92 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 93 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 94 CROSS-BORDER TOLLING: ELECTRONIC TOLL COLLECTION MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 95 ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 96 ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 97 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 98 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 99 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2022-2025 (USD MILLION)

- TABLE 100 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2026-2032 (USD MILLION)

- TABLE 101 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 102 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 103 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 104 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 105 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 106 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 107 US: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 108 US: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 109 CANADA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 110 CANADA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 111 MEXICO: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 112 MEXICO: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 113 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 114 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 115 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2022-2025 (USD MILLION)

- TABLE 116 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2026-2032 (USD MILLION)

- TABLE 117 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 118 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 119 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 120 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 121 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 122 EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 123 UK: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 124 UK: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 125 GERMANY: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 126 GERMANY: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 127 FRANCE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 128 FRANCE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 129 ITALY: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 130 ITALY: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 131 SPAIN: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 132 SPAIN: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 133 NORDICS: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 134 NORDICS: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 135 NORWAY: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 136 NORWAY: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 137 REST OF EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 138 REST OF EUROPE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 139 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 140 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 141 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2022-2025 (USD MILLION)

- TABLE 142 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2026-2032 (USD MILLION)

- TABLE 143 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 144 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 145 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 146 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 147 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 148 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 149 CHINA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 150 CHINA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 151 JAPAN: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 152 JAPAN: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 153 SOUTH KOREA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 154 SOUTH KOREA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 155 AUSTRALIA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 156 AUSTRALIA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 157 SINGAPORE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 158 SINGAPORE: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 159 INDIA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 160 INDIA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 161 REST OF ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 162 REST OF ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 163 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 164 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 165 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2022-2025 (USD MILLION)

- TABLE 166 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY TOLLING ARCHITECTURE, 2026-2032 (USD MILLION)

- TABLE 167 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 168 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 169 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 170 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 171 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 172 ROW: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 173 SOUTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 174 SOUTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 175 SOUTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 176 SOUTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 177 MIDDLE EAST & AFRICA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 178 MIDDLE EAST & AFRICA: ELECTRONIC TOLL COLLECTION MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 179 MIDDLE EAST & AFRICA: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 180 MIDDLE EAST & AFRICA: ELECTRONIC TOLL COLLECTION MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 181 ELECTRONIC TOLL COLLECTION MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2021-2026

- TABLE 182 ELECTRONIC TOLL COLLECTION MARKET: DEGREE OF COMPETITION, 2025

- TABLE 183 ELECTRONIC TOLL COLLECTION MARKET: REGION FOOTPRINT

- TABLE 184 ELECTRONIC TOLL COLLECTION MARKET: OFFERING FOOTPRINT

- TABLE 185 ELECTRONIC TOLL COLLECTION MARKET: TOLLING ARCHITECTURE FOOTPRINT

- TABLE 186 ELECTRONIC TOLL COLLECTION MARKET: TECHNOLOGY FOOTPRINT

- TABLE 187 ELECTRONIC TOLL COLLECTION: APPLICATION FOOTPRINT

- TABLE 188 ELECTRONIC TOLL COLLECTION MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 189 ELECTRONIC TOLL COLLECTION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 190 ELECTRONIC TOLL COLLECTION MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, JANUARY 2021-APRIL 2026

- TABLE 191 ELECTRONIC TOLL COLLECTION MARKET: DEALS, JANUARY 2021-APRIL 2026

- TABLE 192 ELECTRONIC TOLL COLLECTION MARKET: OTHER DEVELOPMENTS, JANUARY 2021-APRIL 2026

- TABLE 193 KAPSCH TRAFFICCOM AG: COMPANY OVERVIEW

- TABLE 194 KAPSCH TRAFFICCOM AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 195 KAPSCH TRAFFICCOM AG: PRODUCT LAUNCHES

- TABLE 196 KAPSCH TRAFFICCOM AG: DEALS

- TABLE 197 KAPSCH TRAFFICCOM AG: EXPANSIONS

- TABLE 198 KAPSCH TRAFFICCOM AG: OTHER DEVELOPMENTS

- TABLE 199 CONDUENT INCORPORATED: COMPANY OVERVIEW

- TABLE 200 CONDUENT INCORPORATED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 201 CONDUENT INCORPORATED: PRODUCT LAUNCHES

- TABLE 202 CONDUENT INCORPORATED: OTHER DEVELOPMENTS

- TABLE 203 EFKON GMBH: COMPANY OVERVIEW

- TABLE 204 EFKON GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 205 EFKON GMBH: PRODUCT LAUNCHES

- TABLE 206 EFKON GMBH: OTHER DEVELOPMENTS

- TABLE 207 ST ENGINEERING (TRANSCORE): COMPANY OVERVIEW

- TABLE 208 ST ENGINEERING (TRANSCORE): PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 209 ST ENGINEERING (TRANSCORE): PRODUCT LAUNCHES

- TABLE 210 ST ENGINEERING (TRANSCORE): DEALS

- TABLE 211 ST ENGINEERING (TRANSCORE): EXPANSIONS

- TABLE 212 ST ENGINEERING (TRANSCORE): OTHER DEVELOPMENTS

- TABLE 213 THALES: COMPANY OVERVIEW

- TABLE 214 THALES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 THALES: OTHER DEVELOPMENTS

- TABLE 216 SIEMENS: COMPANY OVERVIEW

- TABLE 217 SIEMENS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 218 Q-FREE: COMPANY OVERVIEW

- TABLE 219 Q-FREE: PRODUCT/SERVICE/SOLUTION OFFERED

- TABLE 220 Q-FREE: DEVELOPMENTS

- TABLE 221 CUBIC CORPORATION: COMPANY OVERVIEW

- TABLE 222 CUBIC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 223 CUBIC CORPORATION: PRODUCT LAUNCHES

- TABLE 224 NEOLOGY: COMPANY OVERVIEW

- TABLE 225 NEOLOGY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 NEOLOGY: PRODUCT LAUNCHES

- TABLE 227 NEOLOGY: DEALS

- TABLE 228 NEOLOGY: OTHER DEVELOPMENTS

- TABLE 229 FEIG ELECTRONIC: COMPANY OVERVIEW

- TABLE 230 FEIG ELECTRONIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 231 FEIG ELECTRONIC: PRODUCT LAUNCHES

- TABLE 232 FEIG ELECTRONIC: DEALS

- TABLE 233 TOSHIBA CORPORATION: COMPANY OVERVIEW

- TABLE 234 TOSHIBA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 235 MITSUBISHI HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 236 MITSUBISHI HEAVY INDUSTRIES, LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 237 MITSUBISHI HEAVY INDUSTRIES, LTD.: DEVELOPMENTS

- TABLE 238 QUARTERHILL INC: COMPANY OVERVIEW

- TABLE 239 QUARTERHILL INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 240 QUARTERHILL INC: PRODUCT LAUNCHES

- TABLE 241 QUARTERHILL INC.: DEALS

- TABLE 242 QUARTERHILL INC.: OTHER DEVELOPMENTS

- TABLE 243 PERCEPTICS, LLC: COMPANY OVERVIEW

- TABLE 244 PERCEPTICS, LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 245 PERCEPTICS, LLC: PRODUCT LAUNCHES

- TABLE 246 SKYTOLL: COMPANY OVERVIEW

- TABLE 247 SKYTOLL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 248 SKYTOLL: EXPANSIONS

- TABLE 249 SKYTOLL: OTHER DEVELOPMENTS

- TABLE 250 LIST OF MAJOR SECONDARY SOURCES

- TABLE 251 LIST OF KEY PARTICIPANTS IN PRIMARY INTERVIEW

- TABLE 252 ELECTRONIC TOLL COLLECTION MARKET GROWTH ASSUMPTIONS

- TABLE 253 ELECTRONIC TOLL COLLECTION MARKET: RESEARCH ASSUMPTIONS

- TABLE 254 ELECTRONIC TOLL COLLECTION MARKET: RISK ASSESSMENT

List of Figures

- FIGURE 1 MARKETS COVERED AND REGIONAL SCOPE

- FIGURE 2 DURATION COVERED

- FIGURE 3 MARKET SCENARIO

- FIGURE 4 GLOBAL ELECTRONIC TOLL COLLECTION MARKET, 2022-2032

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN ELECTRONIC TOLL COLLECTION MARKET, 2021-2026

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF ELECTRONIC TOLL COLLECTION MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN ELECTRONIC TOLL COLLECTION MARKET, 2026-2032

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN ELECTRONIC TOLL COLLECTION MARKET, IN TERMS OF VALUE, DURING FORECAST PERIOD

- FIGURE 9 RISING ADOPTION OF CASHLESS TOLLING AND INTELLIGENT TRANSPORTATION SYSTEMS TO DRIVE ELECTRONIC TOLL COLLECTION MARKET

- FIGURE 10 RFID TECHNOLOGY TO ACCOUNT FOR LARGEST SHARE OF ELECTRONIC TOLL COLLECTION MARKET IN 2032

- FIGURE 11 SERVICES SEGMENT TO HOLD LARGEST SHARE OF ELECTRONIC TOLL COLLECTION MARKET IN 2026

- FIGURE 12 ORT TOLLING ARCHITECTURE TO ACCOUNT FOR LARGEST SHARE OF ELECTRONIC TOLL COLLECTION MARKET IN 2026

- FIGURE 13 HIGHWAYS/EXPRESSWAYS TO DOMINATE ELECTRONIC TOLL COLLECTION MARKET IN 2026

- FIGURE 14 NORTH AMERICA CAPTURED SECOND-LARGEST SHARE OF ELECTRONIC TOLL COLLECTION MARKET IN 2025

- FIGURE 15 ELECTRONIC TOLL COLLECTION MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 16 IMPACT ANALYSIS OF DRIVERS

- FIGURE 17 IMPACT ANALYSIS OF RESTRAINTS

- FIGURE 18 IMPACT ANALYSIS OF OPPORTUNITIES

- FIGURE 19 IMPACT ANALYSIS OF CHALLENGES

- FIGURE 20 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 21 VALUE CHAIN ANALYSIS

- FIGURE 22 ELECTRONIC TOLL COLLECTION REALITY ECOSYSTEM

- FIGURE 23 AVERAGE SELLING PRICE OF RFID TAGS AND READERS OFFERED BY KEY PLAYER, 2025

- FIGURE 24 REGION-WISE DATA FOR AVERAGE SELLING PRICE TREND OF ELECTRONIC TOLL COLLECTION SYSTEMS, 2022-2025

- FIGURE 25 IMPORT SCENARIO FOR HS CODE 8530-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2021-2025

- FIGURE 26 EXPORT SCENARIO FOR HS CODE 8530-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2021-2025

- FIGURE 27 TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

- FIGURE 28 INVESTMENT AND FUNDING SCENARIO, 2019-2025

- FIGURE 29 PATENTS APPLIED AND GRANTED, 2016-2025

- FIGURE 30 ELECTRONIC TOLL COLLECTION MARKET DECISION-MAKING FACTORS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR APPLICATIONS

- FIGURE 32 KEY BUYING CRITERIA FOR APPLICATIONS

- FIGURE 33 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 34 BARRIER-BASED ETC SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 35 RFID SEGMENT TO HOLD PROMINENT SHARE OF ELECTRONIC TOLL COLLECTION MARKET IN 2032

- FIGURE 36 SERVICES SEGMENT TO ACCOUNT FOR MAJORITY OF MARKET SHARE IN 2032

- FIGURE 37 ROADSIDE INFRASTRUCTURE SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 38 TRANSACTION PROCESSING SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 39 MANAGED SERVICES SEGMENT TO DOMINATE MARKET THROUGOUT FORECAST PERIOD

- FIGURE 40 HIGHWAYS/EXPRESSWAYS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 41 US TO LEAD ELECTRONIC TOLL COLLECTION MARKET FOR HIGHWAYS/EXPRESSWAYS IN 2032

- FIGURE 42 NORDICS TO ACCOUNT FOR LARGEST SHARE OF EUROPEAN MARKET FOR URBAN CONGESTION CHARGING IN 2032

- FIGURE 43 CHINA TO ACCOUNT FOR LARGEST MARKET SHARE FOR BRIDGES & TUNNELS SEGMENT BY 2032

- FIGURE 44 US TO ACCOUNT FOR LARGEST SHARE OF NORTH AMERICAL ELECTRONIC TOLL COLLECTION MARKET FOR CROSS-BORDER TOLLING IN 2032

- FIGURE 45 ASIA PACIFIC TO DOMINATE ELECTRONIC TOLL COLLECTION MARKET IN 2032

- FIGURE 46 NORTH AMERICA: ELECTRONIC TOLL COLLECTION MARKET SNAPSHOT

- FIGURE 47 EUROPE: ELECTRONIC TOLL COLLECTION MARKET SNAPSHOT

- FIGURE 48 ASIA PACIFIC: ELECTRONIC TOLL COLLECTION MARKET SNAPSHOT

- FIGURE 49 ROW: ELECTRONIC TOLL COLLECTION MARKET SNAPSHOT

- FIGURE 50 MARKET SHARE ANALYSIS OF ELECTRONIC TOLL COLLECTION MARKET, 2025

- FIGURE 51 ELECTRONIC TOLL COLLECTION MARKET: REVENUE ANALYSIS OF FIVE KEY PLAYERS, 2021-2025

- FIGURE 52 COMPANY VALUATION

- FIGURE 53 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 54 BRAND COMPARISON

- FIGURE 55 ELECTRONIC TOLL COLLECTION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 56 ELECTRONIC TOLL COLLECTION MARKET: COMPANY FOOTPRINT

- FIGURE 57 ELECTRONIC TOLL COLLECTION MARKET: STARTUPS/SMES EVALUATION MATRIX, 2025

- FIGURE 58 KAPSCH TRAFFICCOM AG: COMPANY SNAPSHOT

- FIGURE 59 CONDUENT INCORPORATED: COMPANY SNAPSHOT

- FIGURE 60 ST ENGINEERING (TRANSCORE): COMPANY SNAPSHOT

- FIGURE 61 THALES: COMPANY SNAPSHOT

- FIGURE 62 SIEMENS: COMPANY SNAPSHOT

- FIGURE 63 TOSHIBA CORPORATION: COMPANY SNAPSHOT

- FIGURE 64 MITSUBISHI HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

- FIGURE 65 QUARTERHILL INC: COMPANY SNAPSHOT

- FIGURE 66 ELECTRONIC TOLL COLLECTION MARKET: RESEARCH DESIGN

- FIGURE 67 ELECTRONIC TOLL COLLECTION MARKET: RESEARCH APPROACH

- FIGURE 68 PRIMARY INTERVIEW BREAKUP: BY COMPANY TYPE, DESIGNATION, REGION

- FIGURE 69 DATA OBTAINED FROM PRIMARY SOURCES

- FIGURE 70 CORE INSIGHTS FROM EXPERTS

- FIGURE 71 REVENUE GENERATED FROM SALES OF ELECTRONIC TOLL COLLECTIONS

- FIGURE 72 ELECTRONIC TOLL COLLECTION MARKET: DEMAND-SIDE ANALYSIS

- FIGURE 73 ELECTRONIC TOLL COLLECTION MARKET: SUPPLY-SIDE ANALYSIS

- FIGURE 74 ELECTRONIC TOLL COLLECTION MARKET: BOTTOM-UP APPROACH

- FIGURE 75 ELECTRONIC TOLL COLLECTION MARKET: TOP-DOWN APPROACH

- FIGURE 76 ELECTRONIC TOLL COLLECTION MARKET: DATA TRIANGULATION

- FIGURE 77 EXPERT INSIGHTS