PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2072267

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2072267

Automotive Interior Market by Component (HUD, Door Panel, Dome Module, Seat, Headliner, Center Console, Center Stack), Material Type, Level of Autonomy, Electric Vehicle, Passenger Car Class, ICE Vehicle Type, and Region - Global Forecast to 2033

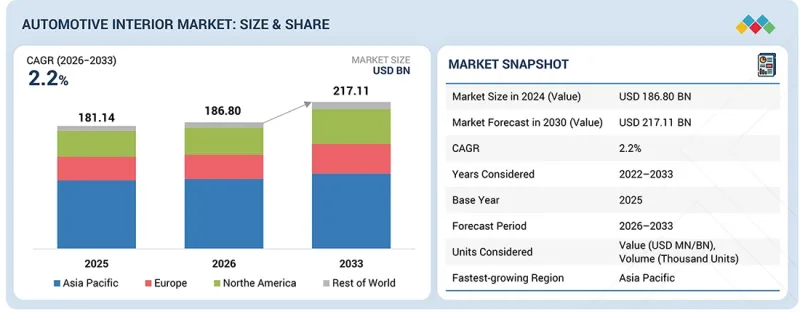

The global automotive interior market size is projected to grow from USD 186.80 billion in 2026 to USD 217.11 billion by 2033, at a CAGR of 2.2%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by Component, Material Type, Level of Autonomy, Electric Vehicle, Passenger Car Class, ICE Vehicle Type, and Region |

| Regions covered | Asia Pacific, Europe, North America, and the Rest of the World |

The automotive interior market is experiencing growth driven by various factors. The automotive industry is currently pushing OEMs to adapt to new changes due to advancements in in-cabin technologies and evolving consumer expectations for comfort, connectivity, and personalization. Vehicle interiors are undergoing rapid change, driven by increasing demand for safety, comfort, and digital experiences. OEMs are prioritizing the integration of next-generation cockpit technologies, AI-enabled infotainment systems, and head-up displays (AR-HUDs), while also using lightweight, sustainable, and recyclable materials to meet regulatory requirements and improve overall vehicle efficiency. As consumers increasingly demand seamless digital experiences and premium interior environments, industry players are investing in innovative, modular, and connected interior solutions, positioning interiors as a key differentiator in the future mobility landscape.

The seating segment is expected to account for the largest market share during the forecast period.

The seating segment is expected to account for the largest share of the automotive interior market, driven by its role in occupant comfort, safety, and overall in-cabin experience. Seating systems consist of components such as frames, foam, trim covers, and adjustment mechanisms, making them a key focus area for OEMs and suppliers. Premium consumers' demand for premium cabin aesthetics and enhanced comfort is accelerating innovation, with features such as ventilated and heated seats, massage functions, memory settings, and advanced support systems becoming common across mid-range and premium vehicles. At the same time, OEMs are focusing on lightweighting and modular interior architectures, driving the adoption of advanced materials such as carbon fiber composites in premium vehicles and glass fiber composites in mid-segment cars, balancing performance and durability. These materials are used across components such as seat structures, dashboards, door panels, and interior trims, contributing to improved efficiency and design flexibility. Technological advancements, including smart sensors, occupant monitoring systems, and electrified seat adjustments, are further transforming seating into a connected and intelligent system. Additionally, rising demand for fuel-efficient vehicles, stringent emission regulations, and the need for noise reduction and durability are driving manufacturers to adopt sustainable, lightweight solutions such as recyclable materials and bio-based foams. Overall, as automakers continue to prioritize comfort, lightweighting, and premium interior experiences, the seating segment is expected to maintain its dominant position in the automotive interior market.

The passenger cars segment is expected to witness strong growth during the forecast period.

The mid-range passenger car segment is the fastest-growing in the automotive interior market, driven by strong demand across Asia Pacific, which accounted for 50-55% of global passenger vehicle production in 2025. Markets like China and India are rapidly expanding, while Europe and North America are also witnessing steady growth as OEMs gain pricing flexibility to integrate advanced features. This segment enables automakers to offer cost-effective HUDs, heated and ventilated seats, ADAS features, and connected infotainment systems, making it the most competitive and volume-driven category. Within the mid-range category, compact and mid-size SUVs are leading demand across regions, prompting OEMs to integrate comfort, safety, and digital features such as ambient lighting, large touchscreens, and smart seating into high-volume models. This shift is transforming mid-segment vehicles into feature-rich cabins, positioning them as the core driver of interior market growth.

The premium passenger car segment is the second-fastest-growing, supported by rising demand for luxury interiors and advanced technologies, and accounts for an estimated 15-20% share globally. This segment is characterized by high-end materials, multi-screen cockpits, AR-HUDs, and immersive in-cabin experiences, with strong competition among global luxury OEMs to differentiate through interior innovation. The economy segment remains largely volume-driven with basic interior features, though OEMs are gradually incorporating entry-level digital displays and improved aesthetics to enhance market appeal at lower costs. Overall, the automotive interior market is primarily driven by the mid-range segment due to high-volume adoption of advanced features, while the premium segment drives innovation and luxury experiences, together shaping overall market growth.

Asia Pacific to hold the largest market share during the forecast period.

Asia Pacific dominates the automotive interior market, led by China and India, followed by Japan and South Korea, driven by high vehicle production, strong domestic demand, and rapid adoption of advanced interior technologies. As of 2025, the passenger car market in the region is largely skewed toward the mid-range segment (50-55%), followed by the economy segment (20-25%) and the premium segment (15-20%), reflecting the region's volume-driven yet feature-oriented market structure.

Across vehicle classes, OEMs are standardizing interior offerings: economy vehicles focus on basic functionality and cost efficiency, while mid-range vehicles integrate a mix of basic and advanced features, such as infotainment systems, connected interfaces, and comfort enhancements. This shift is particularly evident in China, where OEMs are aggressively offering large displays, ADAS, and smart cockpit features even in mid-segment vehicles, whereas in India, adoption is more cost-sensitive with gradual integration of essential digital and comfort features.

In commercial vehicles, interior adoption varies by country, with China leading in advanced cabin integration for both LCVs and HCVs, including telematics, driver monitoring, and digital dashboards, while India is witnessing gradual improvements focused on driver comfort, safety, and basic connectivity. Looking ahead to 2033, OEMs are expected to expand the use of ADAS, connected systems, and enhanced cabin ergonomics in HCVs, driven by regulatory push and fleet efficiency requirements. Overall, OEMs and suppliers are increasingly collaborating on R&D, localization, and technology integration to develop scalable, cost-effective interior solutions tailored to regional demand, reinforcing Asia Pacific's position as the largest and fastest-evolving automotive interior market.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 30%, and Tier I - 70%

- By Designation: CXOs - 20%, Directors - 30%, and Others - 50%

- By Region: North America - 30%, Europe - 20%, Asia Pacific- 40%, and RoW- 10%

The automotive interior market is dominated by global players such as FORVIA Faurecia (France), Adient plc. (Ireland), Robert Bosch GmbH (Germany), Lear Corporation (US), and Antolin (Spain). These companies adopted product launches, deals, and other strategies to gain traction in the automotive interior market.

Research Coverage:

The market study covers the Automotive Interior Market by Component (Center Stack, Head-Up Display, Instrument Cluster, Rear Seat Entertainment, Dome Module, Headliner, Seat, Interior Lighting, Door Panel, Center Console, Adhesives & Tapes, Upholstery), Material Type (Leather, Fabric, Vinyl, Wood, Glass Fiber Composite, Carbon Fiber Composite, Metal), Level of Autonomy (Semi-Autonomous, Autonomous, Non-autonomous), Electric Vehicle (BEV, FCEV, HEV, PHEV), Passenger Car Class (Economic Cars, Mid Segment Cars, Luxury Segment Cars), ICE Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), and Region (Asia Pacific, Europe, North America, RoW). It also covers the competitive landscape and company profiles of the major players in the automotive interior market ecosystem.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

The report will help market leaders and new entrants with information on the closest approximations of revenue numbers for the overall automotive interior market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of

- Key Drivers (Software-defined cabin evolution, EV-driven interior innovation & premiumization of mid-segment vehicles, and smart cabin sensing & occupant monitoring integration), Restraints (Software-hardware integration bottlenecks and Over-the-air (OTA) reliability & cybersecurity risks), Opportunities (Rising demand for reconfigurable and lounge-style interiors, smart surfaces replacing mechanical controls, and sustainable material traceability as a premium feature), and Challenges (Managing seamless integration of multiple digital interfaces and cost-pressure vs premiumization conflict) influencing the growth of the automotive interior market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the automotive interior market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the automotive interior market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the automotive interior market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like FORVIA (France), Adient plc. (Ireland), Robert Bosch GmbH (Germany), Lear Corporation (US), and Antolin (Spain), among others, in the automotive interior market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AUTOMOTIVE INTERIOR MARKET

- 2.4 HIGH-GROWTH SEGMENTS IN AUTOMOTIVE INTERIOR MARKET

- 2.5 ASIA PACIFIC TO HOLD THE LARGEST MARKET SHARE IN TERMS OF VALUE DURING THE FORECAST PERIOD

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE INTERIOR MARKET

- 3.2 AUTOMOTIVE INTERIOR MARKET, BY REGION

- 3.3 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE

- 3.4 AUTOMOTIVE INTERIOR MARKET, BY MATERIAL TYPE

- 3.5 AUTOMOTIVE INTERIOR MARKET, BY LEVEL OF AUTONOMY

- 3.6 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS

- 3.7 AUTOMOTIVE INTERIOR MARKET, BY ELECTRIC VEHICLE TYPE

- 3.8 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Software-defined cabin evolution

- 4.2.1.2 EV-driven interior innovation and premiumization of mid-segment vehicles

- 4.2.1.3 Smart cabin sensing and occupant monitoring integration

- 4.2.2 RESTRAINTS

- 4.2.2.1 Software-hardware integration bottlenecks

- 4.2.2.2 Over-the-air reliability & cybersecurity risks

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising demand for reconfigurable and lounge-style interiors

- 4.2.3.2 Smart surfaces replacing mechanical controls

- 4.2.3.3 Sustainable material traceability as a premium feature

- 4.2.4 CHALLENGES

- 4.2.4.1 Managing seamless integration of multiple digital interfaces

- 4.2.4.2 Cost-pressure vs. premiumization conflict

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.2 INTRODUCTION

- 5.3 GDP TRENDS AND FORECAST

- 5.4 TRENDS IN GLOBAL AUTOMOTIVE INTERIOR INDUSTRY

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.5.1 STRATEGIC SUPPLY CHAIN TRENDS IN AUTOMOTIVE INTERIORS

- 5.6 PRICING ANALYSIS

- 5.7 AVERAGE SELLING PRICE TREND OF COMPONENTS, BY VEHICLE TYPE, 2025

- 5.8 AVERAGE SELLING PRICE TREND OF COMPONENTS, BY REGION, 2025

- 5.9 ECOSYSTEM ANALYSIS

- 5.10 TRENDS/DISRUPTIONS IMPACTING AUTOMOTIVE INTERIOR MARKET

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT SCENARIO OF AUTOMOTIVE INTERIOR MARKET

- 5.11.2 EXPORT SCENARIO OF AUTOMOTIVE INTERIOR MARKET

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 DEVELOPMENT OF INTEGRATED DIGITAL COCKPIT & CENTER STACK PLATFORM

- 5.12.2 DEVELOPMENT OF AUGMENTED REALITY HEAD-UP DISPLAY (AR-HUD)

- 5.12.3 CONCEPT AND SERIAL DEVELOPMENT OF HIGH-END AUTOMOTIVE DOOR PANELS

- 5.12.4 INCORPORATION OF HIDDEN LIGHTING WITHIN TRIM PIECES AND GLOVEBOX

- 5.12.5 DINETTE SEATING FOR WINNEBAGO MPV MODELS

- 5.12.6 ACCENTURE LEVERAGES AI TO DESIGN CAR SEATS WITH INTELLIGENCE-DRIVEN FEATURES

- 5.12.7 DESIGNING REAR INTERIOR COMPARTMENT TRI WITH AESTHETICS AND REDUCED NVH IN CABINS

- 5.12.8 DESIGN AND DEVELOPMENT OF MODULAR CAR INTERIOR SYSTEM TO REDUCE CYCLE TIME

- 5.13 SUPPLIER ANALYSIS

- 5.13.1 SEAT

- 5.13.2 HEAD-UP DISPLAY (HUD)

- 5.13.3 INSTRUMENT CLUSTER

- 5.13.4 DOME MODULE

- 5.13.5 HEADLINER

- 5.13.6 INTERIOR LIGHTING

- 5.13.7 DOOR PANEL

- 5.13.8 CENTER CONSOLE

- 5.13.9 UPHOLSTERY

- 5.13.10 OTHERS

- 5.14 INVESTMENT SCENARIO

- 5.15 PATENT ANALYSIS

- 5.16 KEY CONFERENCES AND EVENTS IN 2026-2027

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE STRATEGIC APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Intelligent ambient lighting using integrated sensors and smart LED controllers

- 6.1.1.2 Active motion & wellness seating systems

- 6.1.1.3 AR HUDs

- 6.1.1.4 Curved and flexible display technologies

- 6.1.1.5 Multi-display and integrated cockpit systems

- 6.1.1.6 Transparent and headliner displays

- 6.1.1.7 High-resolution and high-dynamic-range (HDR) displays

- 6.1.1.8 3D printing materials for vehicle interior parts

- 6.1.1.9 Adaptive lighting

- 6.1.2 ADJACENT TECHNOLOGIES

- 6.1.2.1 Networked lighting controllers

- 6.1.2.2 Lighting control system network with AI

- 6.1.2.3 Connected lighting

- 6.1.3 COMPLEMENTARY TECHNOLOGIES

- 6.1.3.1 Human-centric lighting

- 6.1.3.2 Integrated wellness features

- 6.1.3.3 Multi-material smart surfaces in car interiors

- 6.1.1 KEY TECHNOLOGIES

- 6.2 IMPACT OF AI/GEN AI ON AUTOMOTIVE INTERIOR MARKET

- 6.3 IMPACT OF EU-INDIA FTA TRADE DEAL ON AUTOMOTIVE INTERIOR MARKET

- 6.4 IMPACT OF ISRAEL-IRAN WAR ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 6.5 IMPACT OF FUTURE COCKPIT EVOLUTION

- 6.6 IMPACT OF AUTONOMOUS DRIVING LEVELS ON INTERIOR SPACE RECONFIGURATION

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 SUSTAINABILITY INITIATIVES

- 7.1.3.1 Sustainable materials and lightweight interiors

- 7.1.3.2 Low-emission and health-focused interior technologies

- 7.1.3.3 Circular economy and recyclability initiatives

- 7.1.3.4 Smart and energy-efficient interior systems

- 7.1.3.5 Digitalization and sustainable manufacturing

- 7.1.3.6 Low-carbon supply chain and sourcing

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE

- 9.1 INTRODUCTION

- 9.2 CENTER STACK

- 9.2.1 EVOLUTION TOWARD SOFTWARE-DEFINED AND MULTI-FUNCTIONAL COCKPITS TO DRIVE MARKET

- 9.3 HEAD-UP DISPLAY (HUD)

- 9.3.1 INCREASING ADOPTION OF AR-BASED, DRIVER-CENTRIC DIGITAL INTERFACES TO DRIVE MARKET

- 9.4 INSTRUMENT CLUSTER

- 9.4.1 RISING DEMAND FOR DIGITAL INSTRUMENT CLUSTERS TO DRIVE MARKET

- 9.5 REAR-SEAT ENTERTAINMENT

- 9.5.1 RISING DEMAND FOR CONNECTED AND EXPERIENCE-CENTRIC IN-CABIN ENTERTAINMENT TO DRIVE MARKET

- 9.6 DOME MODULE

- 9.6.1 GROWING POPULARITY OF CONNECTED CARS TO DRIVE MARKET

- 9.7 HEADLINER

- 9.7.1 INCREASING FOCUS ON LIGHTWEIGHT, ACOUSTIC, AND PREMIUM INTERIOR MATERIALS TO DRIVE MARKET

- 9.8 SEAT

- 9.8.1 INCREASING DEMAND FOR PREMIUM AND SMART SEATING SYSTEMS TO DRIVE MARKET

- 9.8.1.1 Bucket seats

- 9.8.1.2 Bench seats

- 9.8.1.3 Split bench seats (60/40, 40/20/40)

- 9.8.1.4 Power seats

- 9.8.1.5 Heated & ventilated seats

- 9.8.1.6 Memory seats

- 9.8.1.7 Massage seats

- 9.8.1.8 Captain seats

- 9.8.1.9 Folding/Flat-fold seats

- 9.8.1.10 Sport seats

- 9.8.1.11 Luxury seats (executive/recliner seats)

- 9.8.1.12 Smart/Connected seats (with sensors & monitoring systems)

- 9.8.1 INCREASING DEMAND FOR PREMIUM AND SMART SEATING SYSTEMS TO DRIVE MARKET

- 9.9 INTERIOR LIGHTING

- 9.9.1 RISING DEMAND FOR PERSONALIZED AND INTELLIGENT AMBIENT LIGHTING TO DRIVE MARKET

- 9.9.2 AUTOMOTIVE INTERIOR LIGHTING APPLICATIONS

- 9.9.2.1 Dashboard lights

- 9.9.2.2 Glovebox lights

- 9.9.2.3 Reading lights

- 9.9.2.4 Dome lights

- 9.9.2.5 Rear-view mirror interior lights

- 9.9.2.6 Engine compartment lights

- 9.9.2.7 Passenger area lights

- 9.9.2.8 Driver area lights

- 9.9.2.9 Footwell lights

- 9.10 DOOR PANEL

- 9.10.1 INCREASING DEMAND FOR PREMIUM INTERIORS AND SMART SURFACE INTEGRATION TO DRIVE MARKET

- 9.11 CENTER CONSOLE

- 9.11.1 INCREASING DEMAND FOR INTEGRATED DIGITAL COCKPIT CONTROLS TO DRIVE MARKET

- 9.12 OTHERS

- 9.13 ADHESIVES & TAPES

- 9.14 UPHOLSTERY

- 9.14.1 INCREASING DEMAND FOR SUSTAINABLE AND PREMIUM INTERIOR MATERIALS TO DRIVE MARKET

- 9.15 KEY INDUSTRY INSIGHTS

10 AUTOMOTIVE INTERIOR MARKET, BY ELECTRIC VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 BATTERY ELECTRIC VEHICLE (BEV)

- 10.2.1 SOFTWARE-DEFINED AND SCREEN-CENTRIC CABIN ARCHITECTURES TO DRIVE MARKET

- 10.3 FUEL CELL ELECTRIC VEHICLE (FCEV)

- 10.3.1 SUSTAINABILITY-FOCUSED PREMIUM INTERIORS TO DRIVE MARKET

- 10.4 HYBRID ELECTRIC VEHICLE (HEV)

- 10.4.1 PREMIUM FEATURE MIGRATION INTO HIGH-VOLUME VEHICLE SEGMENTS TO DRIVE MARKET

- 10.5 PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

- 10.5.1 MULTI-MODE DRIVING AND LONG-DISTANCE COMFORT REQUIREMENTS TO DRIVE MARKET

- 10.6 KEY INDUSTRY INSIGHTS

11 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE

- 11.1 INTRODUCTION

- 11.2 PASSENGER CAR (PC)

- 11.2.1 PREMIUMIZATION AND DIGITAL COCKPIT DIFFERENTIATION IN ICE VEHICLES TO DRIVE MARKET

- 11.3 LIGHT COMMERCIAL VEHICLE (LCV)

- 11.3.1 LAST-MILE DELIVERY OPTIMIZATION AND FLEET DIGITALIZATION TO DRIVE MARKET

- 11.4 HEAVY COMMERCIAL VEHICLE (HCV)

- 11.4.1 FLEET EFFICIENCY AND LONG-HAUL UTILIZATION DEMAND TO DRIVE MARKET

- 11.5 KEY INDUSTRY INSIGHTS

12 AUTOMOTIVE INTERIOR MARKET, BY LEVEL OF AUTONOMY

- 12.1 INTRODUCTION

- 12.2 AUTONOMOUS VEHICLES LAUNCHED

- 12.3 NON-AUTONOMOUS CAR

- 12.3.1 PREMIUMIZATION AND DIGITAL COCKPIT ADOPTION TO DRIVE MARKET

- 12.4 SEMI-AUTONOMOUS CAR

- 12.4.1 EXPANSION OF LEVEL 2+ ADAS AND DRIVER-HMI INTEGRATION TO DRIVE MARKET

- 12.5 AUTONOMOUS CAR

- 12.5.1 SHIFT TOWARD PASSENGER-CENTRIC CABIN EXPERIENCE TO DRIVE MARKET

- 12.6 KEY INDUSTRY INSIGHTS

13 AUTOMOTIVE INTERIOR MARKET, BY MATERIAL TYPE

- 13.1 INTRODUCTION

- 13.2 POLYCARBONATE AND ACRYLONITRILE BUTADIENE STYRENE

- 13.2.1 INCREASING ADOPTION OF DIGITAL COCKPITS AND ADVANCED DISPLAY SYSTEMS TO DRIVE MARKET

- 13.3 POLYPROPYLENE (PP)

- 13.3.1 GROWING DEMAND FOR LIGHTWEIGHT AND COST-EFFICIENT INTERIOR COMPONENTS TO DRIVE MARKET

- 13.4 POLYURETHANE (PU)

- 13.4.1 RISING ADOPTION OF COMFORT-FOCUSED SEATING AND SOFT-TOUCH INTERIORS TO DRIVE MARKET

- 13.5 COMPOSITES

- 13.5.1 INCREASING FOCUS ON LIGHTWEIGHT AND SUSTAINABLE INTERIOR STRUCTURES TO DRIVE MARKET

- 13.6 PVC/THERMOPLASTICS

- 13.6.1 GROWING DEMAND FOR DURABLE AND COST-EFFECTIVE INTERIOR TRIM MATERIALS TO DRIVE MARKET

- 13.7 LEATHER/LEATHERETTE

- 13.7.1 RISING DEMAND FOR PREMIUM INTERIORS AND PERSONALIZED CABIN EXPERIENCES TO DRIVE MARKET

- 13.8 FABRIC/TEXTILE

- 13.8.1 INCREASING PREFERENCE FOR SUSTAINABLE AND COMFORT-ORIENTED UPHOLSTERY MATERIALS TO DRIVE MARKET

- 13.9 METAL

- 13.9.1 GROWING USE OF PREMIUM DECORATIVE TRIMS AND LIGHTWEIGHT STRUCTURAL COMPONENTS TO DRIVE MARKET

- 13.10 KEY INDUSTRY INSIGHTS

14 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS

- 14.1 INTRODUCTION

- 14.2 ECONOMY CAR

- 14.2.1 PREMIUM FEATURE DEMOCRATIZATION AND DIGITAL CONNECTIVITY TO DRIVE MARKET

- 14.3 MID-SEGMENT CAR

- 14.3.1 BALANCED PREMIUMIZATION AND ADVANCED DIGITAL COCKPIT INTEGRATION TO DRIVE MARKET

- 14.4 LUXURY CAR

- 14.4.1 EXPERIENCE-LED INTERIORS AND HYPER-PERSONALIZATION TO DRIVE MARKET

- 14.5 KEY INDUSTRY INSIGHTS

15 AUTOMOTIVE INTERIOR MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 ASIA PACIFIC

- 15.2.1 CHINA

- 15.2.1.1 Smart cockpit innovation and digital cabin experiences to drive market

- 15.2.2 JAPAN

- 15.2.2.1 Focus on cabin refinement and passenger comfort to drive market

- 15.2.3 SOUTH KOREA

- 15.2.3.1 Premium technology adoption across mainstream vehicles to drive market

- 15.2.4 INDIA

- 15.2.4.1 Premium feature expansion into mass-market vehicles to drive market

- 15.2.5 THAILAND

- 15.2.5.1 Strong pickup truck production supports interior demand

- 15.2.6 REST OF ASIA PACIFIC

- 15.2.6.1 Expanding vehicle ownership and interior feature upgrades to drive market

- 15.2.1 CHINA

- 15.3 EUROPE

- 15.3.1 LUXURY VEHICLE INNOVATION AND SUSTAINABLE INTERIOR TECHNOLOGIES TO DRIVE MARKET

- 15.3.2 GERMANY

- 15.3.2.1 Luxury cabin innovation and premium interior technologies to drive market

- 15.3.3 FRANCE

- 15.3.3.1 Sustainable interior materials and electrification trends to drive market

- 15.3.4 UK

- 15.3.4.1 Growing demand for luxury and personalized cabin experiences to drive market

- 15.3.5 SPAIN

- 15.3.5.1 Growing demand for feature-rich mainstream vehicles to drive market

- 15.3.6 ITALY

- 15.3.6.1 Growing demand for premium craftsmanship and design-led interiors to drive market

- 15.3.7 RUSSIA

- 15.3.7.1 Growing demand for durable and comfort-oriented vehicle interiors to drive market

- 15.3.8 TURKEY

- 15.3.8.1 Expanding vehicle production and rising demand for feature-rich vehicles to drive market

- 15.3.9 REST OF EUROPE

- 15.3.9.1 Growing automotive manufacturing and EV investments to drive market

- 15.4 NORTH AMERICA

- 15.4.1 US

- 15.4.1.1 Growing demand for premium seating and luxury cabin experiences to drive market

- 15.4.2 CANADA

- 15.4.2.1 Rising demand for comfort-oriented cabin technologies to drive market

- 15.4.3 MEXICO

- 15.4.3.1 Expanding vehicle production and feature-rich passenger vehicles to drive market

- 15.4.1 US

- 15.5 REST OF THE WORLD (ROW)

- 15.5.1 BRAZIL

- 15.5.1.1 Growing demand for compact SUVs and enhanced cabin experiences to drive market

- 15.5.2 IRAN

- 15.5.2.1 Growing demand for improved cabin comfort and interior quality to drive market

- 15.5.3 SOUTH AFRICA

- 15.5.3.1 Rising adoption of premium pickup and SUV interiors to drive market

- 15.5.1 BRAZIL

- 15.6 KEY INDUSTRY INSIGHTS

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 16.3 MARKET SHARE ANALYSIS, 2025

- 16.4 REVENUE ANALYSIS, 2022-2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 EV type footprint

- 16.7.5.4 Component type footprint

- 16.7.5.5 Vehicle type footprint

- 16.7.5.6 Material type footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING

- 16.8.5.1 List of startups/SMEs

- 16.8.5.2 Competitive benchmarking of startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 FORVIA

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Expansions

- 17.1.1.3.4 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 YANFENG

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.3.4 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key Strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 LEAR CORPORATION

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Expansions

- 17.1.3.3.4 Other developments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 ADIENT PLC.

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Expansions

- 17.1.4.3.4 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key Strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 CONTINENTAL AG

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Expansions

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 ANTOLIN

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 MOTHERSON

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Expansions

- 17.1.7.3.4 Other developments

- 17.1.8 TOYOTA BOSHOKU CORPORATION

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Products offered

- 17.1.8.3.2 Deals

- 17.1.8.3.3 Expansions

- 17.1.8.3.4 Other Developments

- 17.1.9 ROBERT BOSCH GMBH

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Deals

- 17.1.9.3.3 Expansions

- 17.1.10 HYUNDAI MOBIS

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.10.3.3 Expansions

- 17.1.10.3.4 Other Developments

- 17.1.11 DENSO CORPORATION

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.12 ZF FRIEDRICHSHAFEN AG

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product launches

- 17.1.12.3.2 Deals

- 17.1.12.3.3 Other Developments

- 17.1.13 PANASONIC HOLDINGS CORPORATION

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product launches

- 17.1.13.3.2 Deals

- 17.1.14 VALEO

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Product launches

- 17.1.14.3.2 Deals

- 17.1.14.3.3 Expansions

- 17.1.14.3.4 Other developments

- 17.1.15 DRAXLMAIER GROUP

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product launches

- 17.1.15.3.2 Deals

- 17.1.15.3.3 Expansions

- 17.1.1 FORVIA

- 17.2 OTHER KEY PLAYERS

- 17.2.1 NIPPON SEIKI CO., LTD.

- 17.2.2 YAZAKI CORPORATION

- 17.2.3 RENESAS ELECTRONICS CORPORATION

- 17.2.4 JAPAN DISPLAY, INC.

- 17.2.5 MAGNA INTERNATIONAL INC.

- 17.2.6 HARMAN INTERNATIONAL

- 17.2.7 SAINT-GOBAIN

- 17.2.8 PIONEER CORPORATION

- 17.2.9 VISTEON CORPORATION

- 17.2.10 FUJITSU LIMITED

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Breakdown of primaries

- 18.1.2.2 Primary participants

- 18.1.2.3 Objectives of primary research

- 18.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 KEY INSIGHTS OF INDUSTRY EXPERTS

- 19.2 DISCUSSION GUIDE

- 19.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.4 CUSTOMIZATION OPTIONS

- 19.5 RELATED REPORTS

- 19.6 AUTHOR DETAILS

List of Tables

- TABLE 1 AUTOMOTIVE INTERIOR MARKET DEFINITION, BY COMPONENT TYPE

- TABLE 2 AUTOMOTIVE INTERIOR MARKET DEFINITION, BY ICE VEHICLE TYPE

- TABLE 3 AUTOMOTIVE INTERIOR MARKET DEFINITION, BY MATERIAL TYPE

- TABLE 4 AUTOMOTIVE INTERIOR MARKET DEFINITION, BY ELECTRIC VEHICLE TYPE

- TABLE 5 AUTOMOTIVE INTERIOR MARKET DEFINITION, BY LEVEL OF AUTONOMY

- TABLE 6 AUTOMOTIVE INTERIOR MARKET DEFINITION, BY PASSENGER CAR CLASS

- TABLE 7 AUTOMOTIVE INTERIOR MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 8 CURRENCY EXCHANGE RATES

- TABLE 9 OEMS OFFERING SOFTWARE-DEFINED VEHICLE TECHNOLOGIES IN EV VEHICLES

- TABLE 10 OEMS OFFERING SOFTWARE-DEFINED VEHICLE TECHNOLOGIES IN ICE VEHICLES

- TABLE 11 PREMIUM INTERIOR OEM MODELS (2026)

- TABLE 12 SUSTAINABLE MATERIALS USED IN AUTOMOTIVE INTERIORS

- TABLE 13 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- TABLE 14 REAL GDP PERCENTAGE CHANGE, BY COUNTRY, 2022-2031

- TABLE 15 AUTOMOTIVE INDUSTRY TRENDS SHAPING THE FUTURE OF AUTOMOTIVE INTERIORS

- TABLE 16 STRATEGIC SUPPLY CHAIN TRENDS IN AUTOMOTIVE INTERIORS

- TABLE 17 AVERAGE PRICING ANALYSIS OF COMPONENTS, BY VEHICLE TYPE, 2025 (USD)

- TABLE 18 AVERAGE PRICING ANALYSIS OF COMPONENTS, BY REGION, 2025 (USD)

- TABLE 19 AUTOMOTIVE INTERIOR MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 20 IMPORT DATA FOR HS CODE 940120, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 21 EXPORT DATA FOR HS CODE 940120, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 22 SEAT: OEM MODELS AND SUPPLIER DATA

- TABLE 23 HEAD-UP DISPLAY (HUD): OEM MODELS AND SUPPLIER DATA

- TABLE 24 INSTRUMENT CLUSTER: OEM MODELS AND SUPPLIER DATA

- TABLE 25 DOME MODULE: OEM MODELS AND SUPPLIER DATA

- TABLE 26 HEADLINER: OEM MODELS AND SUPPLIER DATA

- TABLE 27 INTERIOR LIGHTING: OEM MODELS AND SUPPLIER DATA

- TABLE 28 DOOR PANEL: OEM MODELS AND SUPPLIER DATA

- TABLE 29 CENTER CONSOLE: OEM MODELS AND SUPPLIER DATA

- TABLE 30 UPHOLSTERY: OEM MODELS AND SUPPLIER DATA

- TABLE 31 OTHERS: OEM MODELS AND SUPPLIER DATA

- TABLE 32 AUTOMOTIVE INTERIOR: PATENT REGISTRATIONS, 2022-2026

- TABLE 33 AUTOMOTIVE INTERIOR MARKET: KEY CONFERENCES AND EVENTS

- TABLE 34 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 35 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 36 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 37 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 38 REGULATIONS AND INITIATIVES

- TABLE 39 REGULATIONS FOR DISPLAY SYSTEMS

- TABLE 40 AUTONOMOUS VEHICLE REGULATION ACTIVITIES

- TABLE 41 SAFETY REGULATIONS RELATED TO AUTOMOTIVE SEATS, BY COUNTRY/REGION

- TABLE 42 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR COMPONENTS

- TABLE 43 KEY BUYING CRITERIA FOR AUTOMOTIVE INTERIOR COMPONENTS

- TABLE 44 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- TABLE 45 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 46 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 47 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 48 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 49 CENTER STACK: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 50 CENTER STACK: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 51 CENTER STACK: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 52 CENTER STACK: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 53 HEAD-UP DISPLAY: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 54 HEAD-UP DISPLAY: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 55 HEAD-UP DISPLAY: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 56 HEAD-UP DISPLAY: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 57 INSTRUMENT CLUSTER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 58 INSTRUMENT CLUSTER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 59 INSTRUMENT CLUSTER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 60 INSTRUMENT CLUSTER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 61 REAR-SEAT ENTERTAINMENT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 62 REAR-SEAT ENTERTAINMENT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 63 REAR-SEAT ENTERTAINMENT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 64 REAR-SEAT ENTERTAINMENT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 65 DOME MODULE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 66 DOME MODULE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 67 DOME MODULE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 68 DOME MODULE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 69 HEADLINER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 70 HEADLINER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 71 HEADLINER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 72 HEADLINER: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 73 SEAT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 74 SEAT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 75 SEAT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 76 SEAT: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 77 CHINA: MODELS WITH ADVANCED SEATING TECHNOLOGY, 2025

- TABLE 78 INDIA: MODELS WITH ADVANCED SEATING TECHNOLOGY, 2025

- TABLE 79 JAPAN: MODELS WITH ADVANCED SEATING TECHNOLOGY, 2025

- TABLE 80 INTERIOR LIGHTING: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 81 INTERIOR LIGHTING: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 82 INTERIOR LIGHTING: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 83 INTERIOR LIGHTING: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 84 DOOR PANEL: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 85 DOOR PANEL: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 86 DOOR PANEL: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 87 DOOR PANEL: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 88 CENTER CONSOLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 89 CENTER CONSOLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 90 CENTER CONSOLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 91 CENTER CONSOLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 92 OTHERS: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 93 OTHERS: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 94 OTHERS: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 95 OTHERS: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 96 ELECTRIC VEHICLE INTERIORS MARKET, BY VEHICLE TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 97 ELECTRIC VEHICLE INTERIORS MARKET, BY VEHICLE TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 98 ELECTRIC VEHICLE INTERIORS MARKET, BY VEHICLE TYPE, 2022-2025 (USD MILLION)

- TABLE 99 ELECTRIC VEHICLE INTERIORS MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 100 BATTERY ELECTRIC VEHICLE INTERIORS MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 101 BATTERY ELECTRIC VEHICLE INTERIORS MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 102 BATTERY ELECTRIC VEHICLE INTERIORS MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 103 BATTERY ELECTRIC VEHICLE INTERIORS MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 104 FUEL CELL ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE 2022-2025 (THOUSAND UNITS)

- TABLE 105 FUEL CELL ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 106 FUEL CELL ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 107 FUEL CELL ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 108 HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 109 HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 110 HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 111 HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 112 PLUG-IN HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 113 PLUG-IN HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 114 PLUG-IN HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 115 PLUG-IN HYBRID ELECTRIC VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 116 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 117 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 118 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE, 2022-2025 (USD MILLION)

- TABLE 119 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 120 PASSENGER CAR: INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 121 PASSENGER CAR: INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 122 PASSENGER CAR: INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 123 PASSENGER CAR: INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 124 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 125 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 126 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 127 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 128 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 129 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 130 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 131 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 132 AUTOMOTIVE INTERIOR MARKET, BY LEVEL OF AUTONOMY, 2022-2025 (USD MILLION)

- TABLE 133 AUTOMOTIVE INTERIOR MARKET, BY LEVEL OF AUTONOMY, 2026-2033 (USD MILLION)

- TABLE 134 AUTONOMOUS VEHICLES LAUNCHED, 2025

- TABLE 135 AUTONOMOUS VEHICLES LAUNCHED, 2024

- TABLE 136 EXPECTED TECHNOLOGY VS. CURRENT TECHNOLOGY READINESS LEVEL OF AUTONOMOUS VEHICLES

- TABLE 137 NON-AUTONOMOUS CAR: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 138 NON-AUTONOMOUS CAR: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 139 SEMI-AUTONOMOUS CAR: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 140 SEMI-AUTONOMOUS CAR: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 141 AUTONOMOUS CAR: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 142 AUTONOMOUS CAR: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 143 AUTOMOTIVE INTERIOR MARKET, BY MATERIAL TYPE, 2022-2025 (USD MILLION)

- TABLE 144 AUTOMOTIVE INTERIOR MARKET, BY MATERIAL TYPE, 2026-2033 (USD MILLION)

- TABLE 145 POLYCARBONATE AND ACRYLONITRILE BUTADIENE STYRENE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 146 POLYCARBONATE AND ACRYLONITRILE BUTADIENE STYRENE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 147 POLYPROPYLENE (PP): AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 148 POLYPROPYLENE (PP): AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 149 POLYURETHANE (PU): AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 150 POLYURETHANE (PU): AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 151 COMPOSITES: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 152 COMPOSITES: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 153 PVC/THERMOPLASTICS: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 154 PVC/THERMOPLASTICS: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 155 LEATHER/LEATHERETTE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 156 LEATHER/LEATHERETTE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 157 FABRIC/TEXTILE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 158 FABRIC/TEXTILE: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 159 METAL: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 160 METAL: AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 161 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS, 2022-2025 (THOUSAND UNITS)

- TABLE 162 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS, 2026-2033 (THOUSAND UNITS)

- TABLE 163 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS, 2022-2025 (USD MILLION)

- TABLE 164 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS, 2026-2033 (USD MILLION)

- TABLE 165 ECONOMY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 166 ECONOMY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 167 ECONOMY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 168 ECONOMY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 169 MID-SEGMENT CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 170 MID-SEGMENT CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 171 MID-SEGMENT CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 172 MID-SEGMENT CARS: INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 173 LUXURY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 174 LUXURY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 175 LUXURY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 176 LUXURY CAR: INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 177 AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 178 AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 179 AUTOMOTIVE INTERIOR MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 180 AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 181 ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 182 ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 183 ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 184 ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 185 CHINA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 186 CHINA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 187 CHINA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 188 CHINA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 189 JAPAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 190 JAPAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 191 JAPAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 192 JAPAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 193 SOUTH KOREA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 194 SOUTH KOREA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 195 SOUTH KOREA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 196 SOUTH KOREA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 197 INDIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 198 INDIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 199 INDIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 200 INDIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 201 THAILAND: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 202 THAILAND: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 203 THAILAND: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 204 THAILAND: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 205 REST OF ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 206 REST OF ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 207 REST OF ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 208 REST OF ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 209 EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 210 EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 211 EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 212 EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 213 GERMANY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 214 GERMANY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 215 GERMANY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 216 GERMANY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 217 FRANCE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 218 FRANCE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 219 FRANCE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 220 FRANCE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 221 UK: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 222 UK: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 223 UK: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 224 UK: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 225 SPAIN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 226 SPAIN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 227 SPAIN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 228 SPAIN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 229 ITALY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 230 ITALY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 231 ITALY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 232 ITALY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 233 RUSSIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 234 RUSSIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 235 RUSSIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 236 RUSSIA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 237 TURKEY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 238 TURKEY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 239 TURKEY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 240 TURKEY: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 241 REST OF EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 242 REST OF EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 243 REST OF EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 244 REST OF EUROPE: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 245 NORTH AMERICA: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 246 NORTH AMERICA: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 247 NORTH AMERICA: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 248 NORTH AMERICA: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 249 US: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 250 US: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 251 US: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 252 US: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 253 CANADA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 254 CANADA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 255 CANADA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 256 CANADA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 257 MEXICO: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 258 MEXICO: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 259 MEXICO: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 260 MEXICO: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 261 REST OF THE WORLD: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 262 REST OF THE WORLD: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 263 REST OF THE WORLD: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 264 REST OF THE WORLD: AUTOMOTIVE INTERIOR MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 265 BRAZIL: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 266 BRAZIL: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 267 BRAZIL: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 268 BRAZIL: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 269 IRAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 270 IRAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 271 IRAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 272 IRAN: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 273 SOUTH AFRICA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 274 SOUTH AFRICA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 275 SOUTH AFRICA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2022-2025 (USD MILLION)

- TABLE 276 SOUTH AFRICA: AUTOMOTIVE INTERIOR MARKET, BY COMPONENT TYPE, 2026-2033 (USD MILLION)

- TABLE 277 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- TABLE 278 AUTOMOTIVE INTERIOR MANUFACTURERS, MARKET SHARE ANALYSIS, 2025

- TABLE 279 AUTOMOTIVE INTERIOR MARKET: REGION FOOTPRINT

- TABLE 280 AUTOMOTIVE INTERIOR MARKET: EV TYPE FOOTPRINT

- TABLE 281 AUTOMOTIVE INTERIOR MARKET: COMPONENT TYPE FOOTPRINT

- TABLE 282 AUTOMOTIVE INTERIOR MARKET: VEHICLE TYPE FOOTPRINT

- TABLE 283 AUTOMOTIVE INTERIOR MARKET: MATERIAL TYPE FOOTPRINT

- TABLE 284 AUTOMOTIVE INTERIOR MARKET: KEY STARTUPS/SMES

- TABLE 285 AUTOMOTIVE INTERIOR MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 286 PRODUCT LAUNCHES, 2022-2026

- TABLE 287 AUTOMOTIVE INTERIOR MARKET: DEALS, 2022-2026

- TABLE 288 AUTOMOTIVE INTERIOR MARKET: EXPANSIONS, 2022-2026

- TABLE 289 AUTOMOTIVE INTERIOR MARKET: OTHER DEVELOPMENTS, 2022-2026

- TABLE 290 FORVIA: KEY CUSTOMERS

- TABLE 291 FORVIA: COMPANY OVERVIEW

- TABLE 292 FORVIA: PRODUCTS OFFERED

- TABLE 293 FORVIA: PRODUCT LAUNCHES

- TABLE 294 FORVIA (FAURECIA): DEALS

- TABLE 295 FORVIA FAURECIA: EXPANSIONS

- TABLE 296 FORVIA FAURECIA: OTHER DEVELOPMENTS

- TABLE 297 YANFENG: KEY CUSTOMERS

- TABLE 298 YANFENG: COMPANY OVERVIEW

- TABLE 299 YANFENG: PRODUCTS OFFERED

- TABLE 300 YANFENG: PRODUCT LAUNCHES

- TABLE 301 YANFENG: DEALS

- TABLE 302 YANFENG: EXPANSIONS

- TABLE 303 YANFENG: OTHER DEVELOPMENTS

- TABLE 304 LEAR CORPORATION: KEY CUSTOMERS

- TABLE 305 LEAR CORPORATION: COMPANY OVERVIEW

- TABLE 306 LEAR CORPORATION: PRODUCTS OFFERED

- TABLE 307 LEAR CORPORATION: PRODUCT LAUNCHES

- TABLE 308 LEAR CORPORATION: DEALS

- TABLE 309 LEAR CORPORATION: EXPANSIONS

- TABLE 310 LEAR CORPORATION: OTHER DEVELOPMENTS

- TABLE 311 ADIENT PLC.: KEY CUSTOMERS

- TABLE 312 ADIENT PLC.: COMPANY OVERVIEW

- TABLE 313 ADIENT PLC.: PRODUCTS OFFERED

- TABLE 314 ADIENT PLC: PRODUCT LAUNCHES

- TABLE 315 ADIENT PLC: DEALS

- TABLE 316 ADIENT PLC: EXPANSIONS

- TABLE 317 ADIENT PLC: OTHER DEVELOPMENTS

- TABLE 318 CONTINENTAL AG: KEY CUSTOMERS

- TABLE 319 CONTINENTAL AG: COMPANY OVERVIEW

- TABLE 320 CONTINENTAL AG: PRODUCTS OFFERED

- TABLE 321 CONTINENTAL AG: PRODUCT LAUNCHES

- TABLE 322 CONTINENTAL AG: DEALS

- TABLE 323 CONTINENTAL AG: EXPANSIONS

- TABLE 324 ANTOLIN: KEY CUSTOMERS

- TABLE 325 ANTOLIN: COMPANY OVERVIEW

- TABLE 326 ANTOLIN: PRODUCTS OFFERED

- TABLE 327 ANTOLIN: PRODUCT LAUNCHES

- TABLE 328 ANTOLIN: DEALS

- TABLE 329 ANTOLIN: EXPANSIONS

- TABLE 330 MOTHERSON: KEY CUSTOMERS

- TABLE 331 MOTHERSON: COMPANY OVERVIEW

- TABLE 332 MOTHERSON (DEUTSCHLAND GMBH): PRODUCTS OFFERED

- TABLE 333 MOTHERSON: PRODUCT LAUNCHES

- TABLE 334 MOTHERSON: DEALS

- TABLE 335 MOTHERSON: EXPANSIONS

- TABLE 336 MOTHERSON: OTHER DEVELOPMENTS

- TABLE 337 TOYOTA BOSHOKU CORPORATION: KEY CUSTOMERS

- TABLE 338 TOYOTA BOSHOKU CORPORATION: COMPANY OVERVIEW

- TABLE 339 TOYOTA BOSHOKU CORPORATION: PRODUCTS OFFERED

- TABLE 340 TOYOTA BOSHOKU CORPORATION: PRODUCT LAUNCHES

- TABLE 341 TOYOTA BOSHOKU CORPORATION: DEALS

- TABLE 342 TOYOTA BOSHOKU CORPORATION: EXPANSIONS

- TABLE 343 TOYOTA BOSHOKU CORPORATION: OTHER DEVELOPMENTS

- TABLE 344 ROBERT BOSCH GMBH: KEY CUSTOMERS

- TABLE 345 ROBERT BOSCH GMBH: COMPANY OVERVIEW

- TABLE 346 ROBERT BOSCH GMBH: PRODUCTS OFFERED

- TABLE 347 ROBERT BOSCH GMBH: PRODUCT LAUNCHES

- TABLE 348 ROBERT BOSCH GMBH: DEALS

- TABLE 349 ROBERT BOSCH GMBH: EXPANSIONS

- TABLE 350 HYUNDAI MOBIS: KEY CUSTOMERS

- TABLE 351 HYUNDAI MOBIS: COMPANY OVERVIEW

- TABLE 352 HYUNDAI MOBIS: PRODUCTS OFFERED

- TABLE 353 HYUNDAI MOBIS: PRODUCT LAUNCHES

- TABLE 354 HYUNDAI MOBIS: DEALS

- TABLE 355 HYUNDAI MOBIS: EXPANSIONS

- TABLE 356 HYUNDAI MOBIS: OTHER DEVELOPMENTS

- TABLE 357 DENSO CORPORATION: KEY CUSTOMERS

- TABLE 358 DENSO CORPORATION: COMPANY OVERVIEW

- TABLE 359 DENSO CORPORATION: PRODUCTS OFFERED

- TABLE 360 ZF FRIEDRICHSHAFEN AG: KEY CUSTOMERS

- TABLE 361 ZF FRIEDRICHSHAFEN AG: COMPANY OVERVIEW

- TABLE 362 ZF FRIEDRICHSHAFEN AG: PRODUCTS OFFERED

- TABLE 363 ZF FRIEDRICHSHAFEN AG: PRODUCT LAUNCHES

- TABLE 364 ZF FRIEDRICHSHAFEN AG: DEALS

- TABLE 365 ZF FRIEDRICHSHAFEN AG: OTHER DEVELOPMENTS

- TABLE 366 PANASONIC HOLDINGS CORPORATION: KEY CUSTOMERS

- TABLE 367 PANASONIC HOLDINGS CORPORATION: COMPANY OVERVIEW

- TABLE 368 PANASONIC HOLDINGS CORPORATION: PRODUCTS OFFERED

- TABLE 369 PANASONIC HOLDINGS CORPORATION: PRODUCTS LAUNCHES

- TABLE 370 PANASONIC HOLDINGS CORPORATION: DEALS

- TABLE 371 VALEO: KEY CUSTOMERS

- TABLE 372 VALEO: COMPANY OVERVIEW

- TABLE 373 VALEO: PRODUCTS OFFERED

- TABLE 374 VALEO: PRODUCTS LAUNCHES

- TABLE 375 VALEO: DEALS

- TABLE 376 VALEO: EXPANSIONS

- TABLE 377 VALEO: OTHER DEVELOPMENTS

- TABLE 378 DRAXLMAIER GROUP: COMPANY OVERVIEW

- TABLE 379 DRAXLMAIER GROUP: PRODUCTS OFFERED

- TABLE 380 DRAXLMAIER GROUP: PRODUCT LAUNCHES

- TABLE 381 DRAXLMAIER GROUP: DEALS

- TABLE 382 DRAXLMAIER GROUP: EXPANSIONS

- TABLE 383 NIPPON SEIKI CO., LTD.: COMPANY OVERVIEW

- TABLE 384 YAZAKI CORPORATION: COMPANY OVERVIEW

- TABLE 385 RENESAS ELECTRONICS CORPORATION: COMPANY OVERVIEW

- TABLE 386 JAPAN DISPLAY, INC.: COMPANY OVERVIEW

- TABLE 387 MAGNA INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 388 HARMAN INTERNATIONAL: COMPANY OVERVIEW

- TABLE 389 SAINT-GOBAIN: COMPANY OVERVIEW

- TABLE 390 PIONEER CORPORATION: COMPANY OVERVIEW

- TABLE 391 VISTEON CORPORATION: COMPANY OVERVIEW

- TABLE 392 FUJITSU LIMITED: COMPANY OVERVIEW

List of Figures

- FIGURE 1 AUTOMOTIVE INTERIOR MARKET SEGMENTATION

- FIGURE 2 MARKET SCENARIO

- FIGURE 3 AUTOMOTIVE INTERIOR MARKET, BY PC CLASS, 2022-2033

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN AUTOMOTIVE INTERIOR MARKET

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF AUTOMOTIVE INTERIOR MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN AUTOMOTIVE INTERIOR MARKET, 2026

- FIGURE 7 AUTOMOTIVE INTERIOR MARKET, BY REGION, 2026-2033

- FIGURE 8 GROWING DEMAND FOR ENHANCED INTERIOR COMPONENTS, SAFETY, AND CONVENIENCE FEATURES TO DRIVE AUTOMOTIVE INTERIOR MARKET GROWTH

- FIGURE 9 ASIA PACIFIC TO DOMINATE AUTOMOTIVE INTERIOR MARKET IN 2026 AND 2033

- FIGURE 10 HEAD-UP DISPLAY TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 11 POLYCARBONATE AND ACRYLONITRILE BUTADIENE STYRENE TO BE LARGEST MATERIAL TYPE SEGMENT

- FIGURE 12 SEMI-AUTONOMOUS CARS - TO BE MARKET LEADER IN 2026 AND 2033

- FIGURE 13 MID-SEGMENT PASSENGER CARS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 14 BATTERY ELECTRIC VEHICLE SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 15 PASSENGER CARS TO BE MAJOR SEGMENT DURING FORECAST PERIOD

- FIGURE 16 AUTOMOTIVE INTERIOR MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 17 AUTOMOTIVE INTERIOR MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 18 AUTOMOTIVE INTERIOR MARKET: ECOSYSTEM ANALYSIS

- FIGURE 19 TRENDS IMPACTING AUTOMOTIVE INTERIOR MARKET

- FIGURE 20 IMPORT DATA FOR HS CODE 940120, BY COUNTRY, 2021-2025 (USD MILLION)

- FIGURE 21 EXPORT DATA FOR HS CODE 940120, BY COUNTRY, 2021-2025 (USD MILLION)

- FIGURE 22 INVESTMENT SCENARIO, 2022-2026

- FIGURE 23 PATENT ANALYSIS, 2016-2026

- FIGURE 24 CRUDE OIL PRICE SURGE FOLLOWING ISRAEL-IRAN CONFLICT, 2026

- FIGURE 25 INCREASE IN DIESEL PRICES ACROSS KEY COUNTRIES, 2026

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR COMPONENTS

- FIGURE 27 KEY BUYING CRITERIA FOR AUTOMOTIVE INTERIOR COMPONENTS

- FIGURE 28 AUTOMOTIVE INTERIOR MARKET, BY COMPONENT, 2026 VS 2033 (USD MILLION)

- FIGURE 29 ELECTRIC VEHICLE INTERIORS MARKET, BY VEHICLE TYPE, 2026 VS 2033 (USD MILLION)

- FIGURE 30 AUTOMOTIVE INTERIOR MARKET, BY ICE VEHICLE TYPE, 2026 VS 2033 (USD MILLION)

- FIGURE 31 ADAS MARKET GROWTH PROJECTIONS

- FIGURE 32 AUTOMOTIVE INTERIOR MARKET, BY LEVEL OF AUTONOMY, 2026 VS 2033 (USD MILLION)

- FIGURE 33 AUTOMOTIVE INTERIOR MARKET, BY MATERIAL TYPE, 2026 VS 2033 (USD MILLION)

- FIGURE 34 AUTOMOTIVE INTERIOR MARKET, BY PASSENGER CAR CLASS, 2026 VS 2033 (USD MILLION

- FIGURE 35 ASIA PACIFIC TO HOLD LARGEST SHARE IN AUTOMOTIVE INTERIOR MARKET DURING FORECAST PERIOD

- FIGURE 36 ASIA PACIFIC: AUTOMOTIVE INTERIOR MARKET SNAPSHOT

- FIGURE 37 EUROPE: AUTOMOTIVE INTERIOR MARKET SNAPSHOT

- FIGURE 38 NORTH AMERICA: AUTOMOTIVE INTERIOR MARKET SNAPSHOT

- FIGURE 39 BRAZIL TO HOLD LARGEST MARKET SHARE IN REST OF THE WORLD

- FIGURE 40 AUTOMOTIVE INTERIOR MANUFACTURER, MARKET SHARE ANALYSIS, 2025

- FIGURE 41 REVENUE ANALYSIS OF TOP 5 PLAYERS, 2022-2025

- FIGURE 42 COMPANY VALUATION OF KEY PLAYERS, 2025

- FIGURE 43 FINANCIAL METRICS OF KEY PLAYERS, 2025

- FIGURE 44 BRAND/PRODUCT COMPARISON

- FIGURE 45 AUTOMOTIVE INTERIOR MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 46 AUTOMOTIVE INTERIOR MARKET: COMPANY FOOTPRINT

- FIGURE 47 AUTOMOTIVE INTERIOR MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 48 FORVIA: COMPANY SNAPSHOT

- FIGURE 49 YANFENG: COMPANY SNAPSHOT

- FIGURE 50 LEAR CORPORATION: COMPANY SNAPSHOT

- FIGURE 51 ADIENT PLC.: COMPANY SNAPSHOT

- FIGURE 52 CONTINENTAL AG: COMPANY SNAPSHOT

- FIGURE 53 ANTOLIN: COMPANY SNAPSHOT

- FIGURE 54 MOTHERSON: COMPANY SNAPSHOT

- FIGURE 55 TOYOTA BOSHOKU CORPORATION: COMPANY SNAPSHOT

- FIGURE 56 ROBERT BOSCH GMBH: COMPANY SNAPSHOT

- FIGURE 57 HYUNDAI MOBIS: COMPANY SNAPSHOT

- FIGURE 58 DENSO CORPORATION: COMPANY SNAPSHOT

- FIGURE 59 ZF FRIEDRICHSHAFEN AG: COMPANY SNAPSHOT

- FIGURE 60 PANASONIC HOLDINGS CORPORATION: COMPANY SNAPSHOT

- FIGURE 61 VALEO: COMPANY SNAPSHOT

- FIGURE 62 RESEARCH DESIGN

- FIGURE 63 RESEARCH DESIGN MODEL

- FIGURE 64 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 65 DETAILED ILLUSTRATION OF BOTTOM-UP APPROACH

- FIGURE 66 BOTTOM-UP APPROACH

- FIGURE 67 TOP-DOWN APPROACH

- FIGURE 68 DATA TRIANGULATION