PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689953

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689953

Phosphoric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

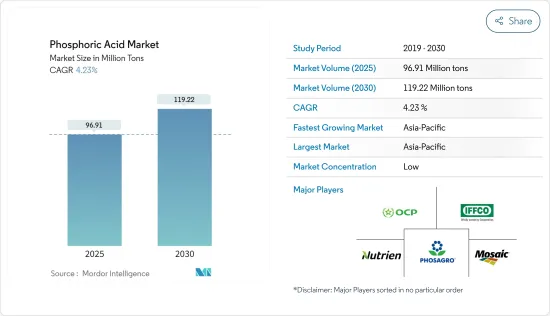

The Phosphoric Acid Market size is estimated at 96.91 million tons in 2025, and is expected to reach 119.22 million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 pandemic as it disrupted the main supply and manufacturing lines, leading to acute shortages. The main use of phosphoric acid is for producing fertilizers. The pandemic also led to a decrease in crop production, accompanied by a shortage of food and other essentials among people. After the pandemic, the market picked up speed, and the demand grew as major industries got back to work.

Key Highlights

- Since most phosphoric acid is used to make fertilizer, the rising demand from the fertilizer industry and increasing usage in the food and beverage industry are expected to drive market demand.

- Health hazards caused by phosphoric acid and the high price of fertilizers are expected to hinder the market's growth.

- Nevertheless, the recovery of rare earth elements from phosphoric acid and the commercialization of chiral phosphoric acid as a catalyst are expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Phosphoric Acid Market Trends

Fertilizer Industry to Dominate the Market

- Phosphoric acid is basically an intermediate used to produce fertilizers. Fertilizers like monoammonium phosphate (MAP), diammonium phosphate (DAP), and trisodium phosphate (TSP) are produced from phosphoric acid.

- Phosphoric acid forms a key component for many fertilizers as it is a multi-function agent used for plant nutrition, pH adjustment, and cleansing irrigation equipment from lime precipitation. It is a rich source of phosphorus for plants.

- Phosphorus fertilizers are extremely important for the plant and provide better activities than organic fertilizers. Phosphorus accelerates the maturation of the plant and also provides the development of the roots. This is particularly important for dry areas.

- According to the Essential Chemical Industry, annually, more than 43 million metric tons of phosphoric acid are produced worldwide, of which about 90% are used to make fertilizers.

- According to the USDA Foreign Agricultural Service, China, Russia, the United States, India, and Canada produce more than 60% of the world's fertilizer nutrients combined. Russia and the United States each produce less than 10% of global fertilizers, while China produces approximately 25%.

- In September 2022, the US government announced programs worth USD 500 million to boost domestic fertilizer production, and the European Union is being urged to take similar action. Canada, already the world's largest supplier of potash fertilizers, announced in November 2022 that it will boost its fertilizer exports by 20% annually, filling a gap left by blocked shipments from other countries.

- According to the International Fertilizer Association (IFA), China is the largest user of fertilizer, consuming nearly one-quarter of global fertilizer supplies. In 2022, a total of 55.7 million tons of NPK fertilizer was produced in China. This was 55.44 million tons in 2021 and 54.96 million tons in 2020.

- Therefore, considering the growth trends and production of fertilizers in different regions worldwide, the fertilizer industry is likely to dominate the market, which, in turn, is expected to enhance the demand for phosphoric acid during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the phosphoric acid market in 2022 with a considerable volume share, and it is expected to maintain its dominance during the forecast period.

- This is due to China being the world's largest producer and consumer of fertilizer. In countries like China, India, and Southeast Asian nations, the demand for phosphoric acid has been increasing continuously.

- China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for phosphoric acid, which is used in fertilizers, is rapidly increasing owing to the large-scale agricultural activities in the country.

- Phosphoric acid is also used extensively in the production of lithium-iron-phosphate batteries, and China is the dominant country in this field. In 2022, 44% of the total electric vehicles sold in China used LFP batteries, followed by 6% in Europe and 3% in the United States and Canada.

- India, another large fertilizer producer, is the second largest user. Much of India's usage is fueled by the Indian government's heavy subsidization of fertilizers. In the financial year 2022, over 42 million metric tons of fertilizers were produced in India. Fertilizer production in India peaked in the financial year 2020 at over 46 million metric tons. During the last few years, there has been a favorable policy facilitating investments in the public, cooperative, and private sectors.

- Phosphoric acid is also used in the food and beverage industries to acidify foods and beverages, such as various colas and jams, providing a tangy or sour taste. According to the US Department of Agriculture (USDA), the Indian food industry ranks as the third-largest food industry globally. The industry has been experiencing steady growth over the past several years, with India anticipated to become the largest food producer in the world. The country's food and grocery (F&G) retail market is projected to surpass USD 850 billion in sales by 2025.

- Hence, the reasons mentioned above are likely to fuel the growth of the phosphoric acid market in Asia-Pacific over the forecast period.

Phosphoric Acid Industry Overview

The phosphoric acid market is partially consolidated, with several companies operating on both global and regional levels. Some of the major players in the market (not in any particular order) include OCP Group, Mosaic, PhosAgro Group of Companies, Nutrien Ltd, and IFFCO, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Drivers

- 4.1.1 High Demand for Fertilizer Industry

- 4.1.2 Increasing Usage in the Food and Beverage Industry

- 4.2 Market Restraints

- 4.2.1 Health Hazards Caused by Phosphoric Acid

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Supplier

- 4.4.2 Bargaining Power of Buyer

- 4.4.3 Threat of New Entrant

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Price Trend Analysis of Phosphoric Acid (2018-2023)

- 4.6 Technological Snapshot

5 Market Segmentation (Market Size in Volume)

- 5.1 By End-user Industry

- 5.1.1 Fertilizer

- 5.1.2 Food and Beverages

- 5.1.3 Chemicals

- 5.1.4 Medicine

- 5.1.5 Metallurgy

- 5.1.6 Other End-user Industries

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Merger and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 Agropolychim

- 6.4.3 EuroChem Group

- 6.4.4 ICL

- 6.4.5 IFFCO

- 6.4.6 Innophos

- 6.4.7 J.R. Simplot Company

- 6.4.8 Mosaic

- 6.4.9 Nutrien Ltd

- 6.4.10 Phosagro

- 6.4.11 Sterlite Copper (A Unit of Vedanta Limited)

7 Market Opportunities and Future Trends

- 7.1 Recovery of Rare Earth Elements from Phosphoric Acid

- 7.2 Commercialization of Chiral Phosporic Acid as a Catalyst