PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690869

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690869

Sickle Cell Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

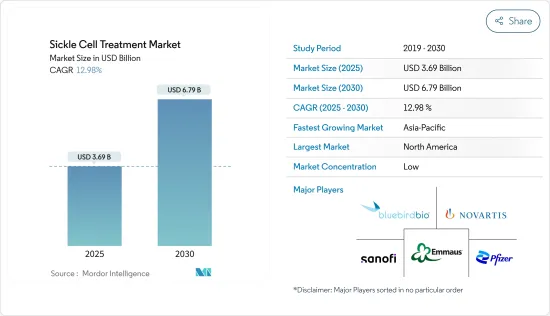

The Sickle Cell Treatment Market size is estimated at USD 3.69 billion in 2025, and is expected to reach USD 6.79 billion by 2030, at a CAGR of 12.98% during the forecast period (2025-2030).

Factors such as the increasing prevalence of sickle cell disease and the growing R&D activities regarding sickle cell disease are expected to boost the market's growth.

The significant burden of sickle cell disease is expected to boost the need for its treatment and drive market growth. For instance, according to an article published in Frontiers in Hematology in August 2024, sickle cell disease (SCD) is widespread, affecting around 300 thousand newborns annually in sub-Saharan Africa, India, and the Middle East. Additionally, the above-mentioned source reported that about 150 thousand infants are born annually with sickle cell disease in Nigeria alone. Thus, the high prevalence of sickle cell disease is expected to boost the market's growth during the forecast period.

The rising initiatives by various governments and private organizations to treat this disease are expected to drive the market in the coming years. For instance, in June 2024, the World Health Organization (WHO) for the African Region introduced innovative new guidelines to bolster efforts to tackle the increasing burden of sickle cell disease in the region. The SICKLE package was designed to offer a comprehensive and integrated strategy for managing sickle cell disease, facilitating access to essential interventions, promoting education and advocacy, improving the quality of care, and empowering both patients and communities. Thus, increasing government initiatives to enhance the awareness of sickle cell disease treatment are the key market drivers and contribute to market growth.

The increasing R&D activities for developing innovative sickle cell disease treatments may also drive the market. For instance, in October 2024, the Indian Council of Medical Research (ICMR) established a Memorandum of Agreement with Zydus Lifesciences Limited to commence phase-2 clinical trials for Desidustat in individuals with sickle cell disease. The company aims to guarantee that India remains at the forefront of developing innovative and cost-effective healthcare solutions for the treatment of sickle cell disease. Additionally, in June 2024, Vanderbilt University Medical Center (VUMC) researchers highlighted findings from a multicenter, international Phase 2 clinical trial that demonstrated a promising new curative treatment for sickle cell disease (SCD). The therapy, which involves a nonmyeloablative haploidentical bone marrow transplant (BMT) combined with thiotepa and posttransplant cyclophosphamide (PTCy), has shown similar effectiveness and costing only one-fifth of the Food and Drug Administration (FDA) approved myeloablative gene therapy alternatives. Thus, such increasing R&D efforts are likely to bolster the market growth.

Thus, factors such as the rising prevalence of sickle cell disease, the increasing awareness of government initiatives, and the rising R&D activities are expected to boost the market's growth. However, the high cost of treatment is expected to restrain this growth.

Sickle Cell Treatment Market Trends

Blood Transfusion Segment is Expected to Witness Significant Growth Over the Forecast Period

The blood transfusion segment is expected to witness healthy growth over the forecast period. This growth is attributed to the high demand for blood transfusion in sickle cell treatment and the increased prevalence of SCD. Blood transfusions enable the supply of normal red blood cells, which can enhance hemoglobin levels to improve oxygen delivery in the body. Thus, sickle cell blockage in blood vessels and the desire to make more sickle cells are reduced.

The growing need for blood transfusions to treat sickle cell disease is anticipated to contribute significantly to the segment growth. For instance, according to the data updated by the Centers for Disease Control and Prevention (CDC) in May 2024, individuals with sickle cell disease (SCD) may necessitate one or more blood transfusions (receiving healthy blood from a donor) at some point during their lifetime. During a blood transfusion, the patient's blood and the donated blood must have matching antigens or particular proteins on the surface of each red blood cell.

Additionally, the data published by the Canadian Blood Services in June 2023 highlighted that around 15,000 blood units are transfused every year to individuals in Canada who have sickle cell disease. Thus, blood transfusion is significantly adopted by the population affected with sickle disease to reduce its burden, which in turn drives the segment's growth.

Rising R&D for sickle cell disease is also expected to boost the segment's growth. For instance, according to data updated by clinicaltrials.gov, there are around 87 ongoing and active clinical trials for blood transfusion in sickle cell disease as of December 2024. Thus, the large number of clinical trials is expected to boost the adoption of blood transfusion for this treatment.

Thus, factors such as the increasing use of blood transfusion for its management and the rising R&D for sickle cell disease are expected to enhance the segment's growth.

North America is Expected to Hold a Significant Share in the Sickle Cell Treatment Market During the Forecast Period

North America is expected to hold a significant share of the overall sickle cell treatment market, with the United States being the major contributor. The growth in the region is attributed to improving access to sickle cell disease (SCD) treatment and potential pipeline candidates. The strong government support in the United States will further foster the market's development. The rising prevalence of sickle cell disease in the region, the increasing number of clinical trials, and the rising product launches are expected to boost the market's growth in the region.

The substantial burden of sickle cell disease in North American countries is expected to necessitate its treatment, thereby promoting market growth. For instance, according to the data updated by the Centers for Disease Control and Prevention (CDC) in May 2024, sickle cell disease (SCD) affects approximately 100,000 Americans every year, and SCD occurs among about 1 out of every 365 black or African American births. Similarly, according to the data published by the Canadian Blood Services in June 2023, sickle cell disease is Canada's most prevalent hereditary condition, with more than 6,000 individuals affected nationwide in 2023. Thus, the huge burden of sickle cell disease in the region fuels the need for its treatment products and drives the market growth over the forecast period.

The government's increasing initiatives are also expected to boost the market's growth in the region. For instance, in November 2024, the Clinton Health Access Initiative (CHAI) introduced a groundbreaking three-year grant of USD 8 million from Open Philanthropy, an advised fund associated with the Silicon Valley Community Foundation, to enhance initiatives to combat sickle cell disease (SCD). This funding will contribute to improving access to treatment and care for children affected by SCD in the United States.

Moreover, in October 2023, the Mount Sinai Health System awarded a USD 12 million grant from the National Heart, Lung, and Blood Institute to evaluate new treatment alternatives for sickle cell disease and identify the most effective options for individual patients. This research, titled REAL (Registry Expansion Analyses to Learn) Answers, involves collaboration among 10 sickle cell centers in the United States and will utilize an innovative observational study method known as target trial emulation. Thus, increasing initiatives to enhance research activities for developing innovative and effective treatments associated with sickle cell disease is anticipated to drive market growth in the country.

Thus, factors such as the rising prevalence of sickle cell disease, rising R&D activities, and government initiatives are expected to boost the market's growth in the region.

Sickle Cell Treatment Industry Overview

The sickle cell treatment market is fragmented, with the presence of several regional and global companies. Companies are taking initiatives to develop novel therapies in the market studied. Some of the players include Novartis AG, Emmaus Medical Inc., Sanofi SA, Pfizer, and Bluebird bio, Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Sickle Cell Disease

- 4.2.2 Increasing R&D Activity

- 4.3 Market Restraints

- 4.3.1 High Cost of Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Treatment Modality

- 5.1.1 Blood Transfusion

- 5.1.2 Bone Marrow Transplant

- 5.1.3 Pharmacotherapy

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Specialty Clinics

- 5.2.3 Other End-Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Novartis AG

- 6.1.2 Emmaus Medical Inc.

- 6.1.3 Agios Pharmaceuticals, Inc.

- 6.1.4 Medunik USA

- 6.1.5 Sarepta Therapeutics

- 6.1.6 Sanofi SA

- 6.1.7 Bluebird bio, Inc.

- 6.1.8 Pfizer Inc.

- 6.1.9 Aruvant Sciences Inc.

- 6.1.10 Glycomimetics Inc.

- 6.1.11 Editas Medicine Inc.

- 6.1.12 CRISPR Therapeutics

7 MARKET OPPORTUNITIES AND FUTURE TRENDS