PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644434

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644434

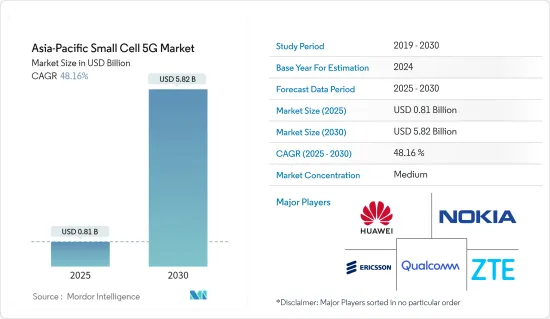

Asia-Pacific Small Cell 5G - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Asia-Pacific Small Cell 5G Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 5.82 billion by 2030, at a CAGR of 48.16% during the forecast period (2025-2030).

The trend of artificial intelligence (AI) and the Internet of Things (IoT) is observed in every sector, and to develop the urban outlook, Governments are working on smart city models.

Key Highlights

- Smart cities' essential features are robust optical fiber connectivity, Wi-Fi, intelligent traffic management, smart parking, and energy-efficient street lighting. Small cells will be crucial in developing these smart cities because they can offer next-generation solutions.

- In the Asia-Pacific region, dominant operator groups are absent, and different countries have different levels of telecom development. Some countries of the region lack appropriate fiber penetration, and most currently operational macro sites lack fiber backhaul connectivity. Fiber backhaul support is required to deploy small cells efficiently and raise the current fiberization levels of large cell sites.

- Since underground fiber installation is costly and time-consuming, aerial fibers have been implemented in Japan due to their comparatively quick and straightforward installation processes. The slow installation of 5G infrastructure will restrain the small cell 5G market.

- To offer better indoor coverage, in Feb 2023, Ericsson developed the IRU 8850 indoor radio unit that will provide better network performance and user experience, regardless of the size or complexity of the building. The company claims it delivers up to four times the capacity of its predecessors.

Asia-Pacific Small Cell 5G Market Trends

Telecom Operators are expected to Hold Significant Share

- The advent of 5G in the Asia-Pacific region has accelerated small-cell deployment for high-speed network connectivity. Many nations have created exemption standards that can be applied when deploying new Small Cells. For instance, in Singapore, The Infocomm Media Development Authority (IMDA) has directed the building developers and owners to provide rooftop spaces free of charge for telecommunication equipment the telecom providers.

- Japan's Government has granted permissions for installing 5G base stations on 208,000 traffic lights across the country. Local administrations and operators jointly shared the costs of using the traffic lights for 5G deployments. This will help with more deployment of the solution in less time, thereby circulating 5G connectivity faster throughout the country.

- In South Korea, 202,903 5G base stations were installed at the end of February 2022, and investments are being made to expand the network further. This has opened the door for ground-breaking 5G applications and services, like robotics integration into the workplace, smart city planning, and self-driving cars. For instance, SK Telecom and Samsung Electronics collaborated to develop 5G option 4 technology, which is an advanced option to the existing 5G Standalone technology.

China is Expected to Hold Major Share

- China is leading 5G development on a worldwide scale. More than 2.54 million 5G base stations have been built nationwide, and more than 575 million people now own 5G smartphones. The country further plans to invest 1.2 trillion yuan (174.2 billion USD) in 5G network construction by 2025. This growing demand for a 5G stable network is accelerating the deployment of small-cell solutions in the country.

- Along with 5G developments, research is ongoing for 6G technology. IMT-2030 (6G) Promotion Group has been formed in the country to speed up the R&D of 6G technology. Around 2030, the world is anticipated to witness the commercialization of 6G. China is leading the charge in supporting the commercialization of 5G, which will provide a strong basis for the development of 6G.

- The technology leaders like Huawei, ZTE, and (state-owned) Datang Telecom are the big beneficiaries of China's 5G infrastructure spending. For instance, the Beijing Branch of China Mobile, the China Mobile Research Institute, China Transport Telecommunications & Information Group, and ZTE all collaborated on the 5G non-terrestrial network (NTN) testing.

- Communication instances, including synchronization, broadcasting, accessing, and data transmission, were all successfully tested during this trial.

- In August 2022, China Mobile collaborated with Comba Telecom to deploy small cell base stations. These are designed for complex indoor locations to provide greater flexibility and efficiency for medium- and large-scale indoor radio networks.

Asia-Pacific Small Cell 5G Industry Overview

The Asia-Pacific small cell 5G market is moderately concentrated, with prominent players leading the overall market. Over the past few years, cellular network growth has increased, and new technologies like 5G are driving demand for fast and effective connectivity options. To cater to the needs of these emerging technologies, these technology providers are making significant investments in developing and improving solutions like small cells that enhance the performance of signals by avoiding obstructions. Some players dominating this market include Nokia Corporation, Huawei, Ericsson, ZTE Corporation, Samsung Electronics, Qualcomm, and more.

In October 2022, HFCL partnered with Qualcomm to develop 5G outdoor small-cell solutions. The 5G drive in India is taking an edge, and the telecom operators need small-cell solutions to complement their macro networks at public venues like airports, railway stations, stadiums, etc. These small-cell solutions will support 5G non-standalone (NSA) and standalone (SA) modes. These small cells will be installed on street poles, building walls, and rooftops to cover the traffic hotspot areas.

In October 2022, Singtel began to use Ericsson's radio cell on its 5G network. The AIR 3268 radio, used in Singtel's networks, reduces energy consumption by up to 18% and weight by around 40% compared to preceding generations of 5G radios. The solution provides real-time channel estimation and removes undesirable noise interferences, boosting capacity, coverage, and connectivity speeds. Singtel aims to become Singapore's greenest 5G network, achieving net-zero emissions by 2050. Adopting this solution will help telecom providers optimize power and energy utilization in their operations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Covid-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Mobile Data Traffic

- 5.1.2 Evolution of Network Technology and Connectivity Devices

- 5.2 Market Restraints

- 5.2.1 Poor Backhaul Connectivity

6 TECHNOLOGY SNAPSHOT

- 6.1 Femtocell

- 6.2 Picocell

- 6.3 Microcell

- 6.4 Metrocell

7 MARKET SEGMENTATION

- 7.1 Operating Environment

- 7.1.1 Indoor

- 7.1.2 Outdoor

- 7.2 End-User Vertical

- 7.2.1 Telecom Operators

- 7.2.2 Enterprises

- 7.2.3 Residential

- 7.3 Country

- 7.3.1 China

- 7.3.2 India

- 7.3.3 South Korea

- 7.3.4 Japan

- 7.3.5 Australia and New Zealand

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Qualcomm Technologies Inc.

- 8.1.2 Nokia Corporation

- 8.1.3 Huawei Technologies Co. Ltd.

- 8.1.4 Telefonaktiebolaget LM Ericsson

- 8.1.5 Airspan Networks Inc.

- 8.1.6 ZTE Corporation

- 8.1.7 CommScope Inc.

- 8.1.8 Cisco Systems Inc.

- 8.1.9 Qucell Inc.

- 8.1.10 Samsung Electronics Co. Ltd.

- 8.1.11 NEC Corporation

- 8.1.12 Baicells Technologies Co. Ltd.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET