PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692515

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692515

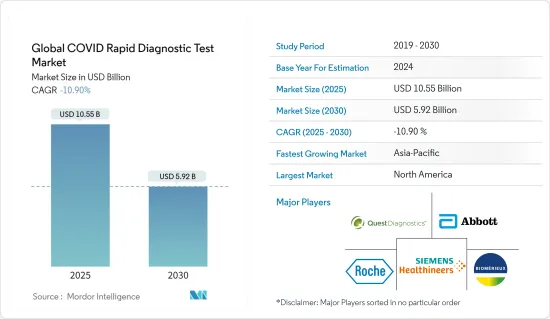

Global COVID Rapid Diagnostic Test - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Global COVID Rapid Diagnostic Test Market size is estimated at USD 10.55 billion in 2025, and is expected to decline to USD 5.92 billion by 2030.

Factors such as rising cases of COVID-19 and its new variants and the increasing number of approvals for new and advanced COVID-19 rapid diagnostic tests" are boosting the market growth.

The increasing number of COVID-19 cases and the emergence of different variants across the globe is creating the need for early detection of the symptoms. For instance, according to the data published by the WHO, in January 2023, about 753 million confirmed cases of COVID-19 were reported globally, "compared to over 645 million confirmed cases in December 2022. As per the same source, the highest number of new weekly cases in 2023 were reported from Japan (4,19,033), followed by China (1,58,687), South Korea (1,48,261), Germany (64,545), and Brazil (51,176). Also, in November 2021, the WHO identified the SARS-CoV-2 coronavirus variant omicron and listed it as a variant of concern. The recent increase in COVID-19 cases has been linked to cases of the extremely contagious variety, including a subvariant known as BA.2, or ","tealth omicron,", particularly in places where safety procedures have been lax. Hence, this supports market growth.

The rapid diagnostic test provides quick results and is also easy to use. Additionally, during the pandemic, the companies were engaged in product developments in the rapid diagnostic segment for COVID-19, continuously increasing market growth. For instance, in May 2022, BD launched a new high-throughput molecular diagnostic combination test for SARS-CoV-2 and Influenza A/B on BD SARS-CoV-2/Flu assay for the BD COR System, an automated multiplexed real-time RT-PCR (reverse transcriptase - polymerase chain reaction) test to detect and differentiate SARS-CoV-2 and influenza A, and influenza B from a single nasal sample from patients who are showing signs of respiratory viral infection.

Furthermore, the growing number of government and ororganizations'nitiatives in developing affordable test kits for COVID-19 are also expected to increase the mamarket'srowth over the forecast period. For instance, in June 2021, the Union Minister of State for Education, Communications, Electronics and IT launched an 'affordable" and "accurate" Rapid Antigen Test kit for COVID at the Indian Institute of Technology (IIT).

Moreover, the technological advancements in COVID-19 diagnostics tests and new product approvals increase the availability of novel diagnostic products in the market. This, in turn, is anticipated to fuel market growth. For instance, in June 2022, Kaneka Corporation, a Japan-based company, received authorization to manufacture and sell "Kaneka Immunochromatography SARS-CoV-2 Ag," a COVID-19 antigen test kit.

However, the increasing product recalls due to quality control issues, stringent regulations and policies related to COVID-19 testing, and product approvals are likely to impede the growth of the COVID rapid diagnostic tests market over the forecast period.

COVID Rapid Diagnostic Test Market Trends

Molecular Tests Segment is Expected to Register a Significant CAGR Over the Forecast Period

Molecular tests are generally referred to as RT-PCR or nucleic acid amplification tests (NAATs). Bits of viral RNA is amplified by molecular tests to enable the detection of viral infection by specialized testing. Molecular tests primarily include polymerase chain reaction (PCR) tests, loop-mediated isothermal amplification (LAMP), and clustered, regularly interspaced short palindromic repeat (CRISPR)-based assays. Molecular testing offers a higher level of selectivity and is highly precise compared to other tests for COVID-19. Hence, RT-PCR is recommended as the gold standard for COVID-19 testing by several authorities such as WHO, EU, and FDA, among others.

Furthermore, the companies offering COVID-19 detection tests are largely focused on providing highly efficient and precision testing through their innovation, thereby leading to the launch and approval of several molecular diagnostic products, which is expected to positively impact the market. For instance, in May 2022, Belgium-based miDiagnostics launched an ultrafast COVID-19 PCR test based on silicon chip technology. The company's latest test can provide results in about 30 minutes. Also, in March 2022, Sense Biodetection received CE Marking for Veros COVID-19 from the European Authority. Veros COVID-19 is a fully integrated, easy-to-use molecular diagnostic test that provides laboratory-quality results in 15 minutes.

Therefore, due to the high efficacy of molecular tests, and new product launches in the area, the molecular test segment is expected to have a healthy market share.

North America is Expected to Hold Significant Market Share Over the Forecast Period

North America is expected to witness significant growth in the COVID rapid diagnostics tests market over the forecast period owing to the factors such as the high prevalence of COVID-19 infections and advanced research and development structure. In addition, the presence of key players as well as rising product launches in the region is also expected to boost the market growth over the forecast period.

As per WHO COVID-19 Dashboard, as of 18th January 2023, there were about 100.1 million confirmed COVID-19 cases in the United States, which was the highest in the world. This high number of cases creates a demand for COVID-19 detection kits for the rapid detection of the disease, thereby contributing to market growth. Also, as per the same source, about 4,539,229 confirmed cases of COVID-19 in Canada and 7,342,764 confirmed cases of COVID-19 in Mexico were reported from 3rd January 2020 to 27th January 2023. Thus, the high burden of coronavirus infection cases among the population raises the demand for rapid diagnostic tests, thereby propelling market growth.

Additionally, as per an article published in MDPI, in May 2022, it has been observed that, in Mexico, the COVISTIX antigen rapid test is extremely sensitive and specific for detecting Omicron SARS-CoV-2 variant carriers. Also, the test is sufficient for screening both asymptomatic and symptomatic people, including those who have passed the peak of viral shedding and carriers of the extremely common Omicron SARS-CoV-2 subtype. Thus, such a study is anticipated to fuel the demand for rapid antigen test products for detecting emerging variants of COVID-19, hence bolstering market growth.

Moreover, the rising regulatory approvals and new product launches increase the availability of novel diagnostic test kits and devices which in turn is anticipated to propel the market growth over the forecast period. For instance, in December 2022, the Government of Canada approved Btnx's Rapid Response COVID-19 Antigen Self-test Kit. Also, in July 2022, the United States FDA issued an emergency use authorization to Watming's Speedy Swab Rapid COVID-19 Antigen Self-Test, a non-prescription home use for the qualitative detection of nucleocapsid protein antigen from the SARS-CoV-2 virus.

Therefore, owing to the factors, such as the high burden of coronavirus infections and its emerging variants, increasing research studies as well as new product launches, the studied market is anticipated to grow over the forecast period.

COVID Rapid Diagnostic Test Industry Overview

The COVID rapid diagnostic test market is moderately fragmented, with the presence of key players in the market. Some of the key companies in the market are Abbott Laboratories, F. Hoffmann-La Roche Ltd, Siemens Healthcare GmbH, bioMerieux SA, Quest Diagnostics Incorporated, and Danaher Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Approvals for New and Advanced COVID-19 Rapid Diagnostic Tests

- 4.2.2 Rising Cases of COVID-19 and its New Variants

- 4.3 Market Restraints

- 4.3.1 Product Recalls Due to Quality Control Issues

- 4.3.2 Stringent Regulations and Policy

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Molecular Tests

- 5.1.2 Antigen Tests

- 5.1.3 Other Tests

- 5.2 By End User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Laboratories and Diagnostics Centers

- 5.2.3 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Thermo Fisher Scientific Inc.

- 6.1.3 Cue Health Inc.

- 6.1.4 Acon Laboratories, Inc.

- 6.1.5 Danaher Corporation (Beckman Coulter, Inc.)

- 6.1.6 F. Hoffmann-La Roche Ltd

- 6.1.7 Siemens Healthcare AG

- 6.1.8 Quidel Corporation

- 6.1.9 bioMerieux SA

- 6.1.10 Quest Diagnostics Incorporated

- 6.1.11 PerkinElmer Inc.

- 6.1.12 Creative Diagnostics

- 6.1.13 CTK Biotech

- 6.1.14 QIAGEN

7 MARKET OPPORTUNITIES AND FUTURE TRENDS