PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444392

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444392

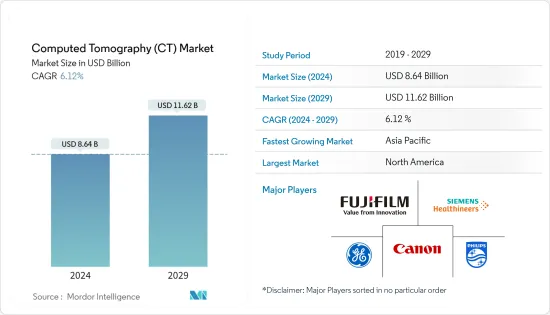

Computed Tomography (CT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Computed Tomography Market size is estimated at USD 8.64 billion in 2024, and is expected to reach USD 11.62 billion by 2029, growing at a CAGR of 6.12% during the forecast period (2024-2029).

The increasing number of COVID-19 cases has increased demand for CT scanners, which is expected to impact the market positively. For instance, in June 2020, the Abu Dhabi Health Services Company (SEHA) launched a 16-slice mobile CT scanner in the UAE for diagnosing pneumonia in COVID-19 patients, indicating that developing countries are using CT scanners for the detection of COVID-19. The CT examination played an important auxiliary role in the diagnosis and subsequent management of COVID-19 patients. CT scans can reduce the chance of false-negative results in the RT-PCR assay. These findings led to an increased demand for CT scans in the country during COVID-19. Governments worldwide are adopting policy measures to reduce the transmission of COVID-19, which is further decreasing the demand for imaging independent of COVID-19. Measures taken by hospitals to expand crisis capacity are further reducing the amount of appropriate medical imaging that can be safely performed.

CT scans are considered the most critical diagnostic tool, especially for lung cancer and traumatic brain injuries. The prevalence of these diseases is boosting the market's growth. Other market drivers are the rising geriatric population, increasing chronic diseases, shifting medical care toward image-guided interventions, and technological advancements. As per the data published by the American College of Chest Physicians in July 2020, lung cancer is one of the most frequently diagnosed cancers. It accounts for 11.6% of the total cancer cases globally. Worldwide lung cancer incidents are estimated to increase by 38%, to 2.89 million, by 2030. A CT scan provides 3D images of bones and helps in better diagnosis and surgeries for orthopedics. Thus, with the rising burden of orthopedic disorders, the demand for CT scanners is also expected to grow.

Major companies in the market are coming up with new CT devices, which are driving the growth of the market studied. For instance, in July 2022, Siemens Healthineers presented its newly launched CT imaging device at the European Congress of Radiology (ECR) 2022 held in Vienna. By presenting the new CT devices, the company has promoted its imaging portfolio across European countries. Hence, with the new launches coming from global companies, the market studied is expected to grow significantly during the coming years.

However, a lack of adequate reimbursement and a stringent regulatory framework are expected to hinder the market's growth.

Computed Tomography Market Trends

The High Slice Segment is Expected to Observe Healthy Growth

High-slice scanners have more than 128 slices, such as 256, 320, and 640 slices, the highest number of slices. Due to the COVID-19 outbreak, companies were developing new products and ramping up production, as CT scanners are used as a primary tool in many areas. In July 2022, Dr. LH Hiranandani Hospital, India, installed 384-slice cardiac CT scan devices by Siemens Heathineers. Cardiologists and cardiac surgeons can make more informed decisions about the next step in the patients' care owing to the modern, AI-based CT scanner that has three times greater diagnostic accuracy (compared to the previous 128 slices for cardiac).

A high-slice CT scanner helps reduce scan time, increase patient throughput, reduce radiation doses, and offer images with more detail and fewer artifacts. It is also preferred for advanced imaging, like in cardiovascular exams. On the other hand, patients with arrhythmias, fast heart rates, obesity, and pediatric patients are better suited for high-slice systems, which are faster and have a larger imaging area. High-slice CT is also quicker as no film images need to be developed. Radiologists can further optimize images using computers to detect microcalcifications that could be missed on low- and medium-slice CT scanners. Thus, the advantages of high-slice CT scanners may boost the market's growth.

These CT scanners are one of the most advanced, providing 3D images of virtually any patient, including those with cardiac or respiratory conditions, which are more complex than other conditions. As per the data provided by the British Heart Foundation report in January 2021, cardiovascular and circulatory diseases cause more than 27% of deaths in the United Kingdom, and about 7.6 million people in the country are living with heart diseases. Therefore, such factors are expected to drive the segment's growth in the future.

North America Accounted for the Largest Share in the Computed Tomography (CT) Market

The North American computed tomography (CT) market holds a significant share globally. The growth of the market in the region is due to an increasing burden of chronic diseases such as cancer and neurological diseases, the presence of a well-established healthcare system, and increased awareness about medical imaging.

The US market's growth can be attributed to the rising geriatric population. As the population ages, more cancer cases and chronic diseases are likely to be identified. According to the National Brain Tumor Society, in 2020, about 700,000 people in the United States had a brain tumor, and around 87,000 people are estimated to be diagnosed with it. Hence, the rising geriatric population is leading to a growing burden of chronic diseases, which may increase the demand for CT scans and drive the market.

According to the PubMed report, the estimated investment for cardiovascular diseases was USD 2,622 million in 2022, a significant increase from the 2021 figures of USD 2,499 million. CT rapidly creates detailed pictures of the heart and its arteries. The test can diagnose or detect plaque build-up in the coronary arteries to determine the risk of heart disease, leading to high demand for CT scans in disease management. The market players are focusing on growth strategies, such as product launches, innovations in existing products, and mergers and acquisitions. For instance, in May 2021, Siemens Healthineers launched SOMATOM X-ceed, which has a high-speed and high-resolution CT scanner with an intelligent operation approach that simplifies procedures for medical staff and patients.

Computed Tomography Industry Overview

The computed tomography (CT) market is consolidated due to the presence of a few major players, including Canon Medical Systems Corporation, Koninklijke Philips NV, GE Healthcare, and Siemens Healthineers. These major players hold a significant share of the industry. Most of the players focus on bringing technologically advanced products into the market to acquire the maximum market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric Population and Increasing Incidences of Chronic Diseases

- 4.2.2 Shifting Medical Care Toward Image-guided Interventions

- 4.2.3 Technological Advancements

- 4.3 Market Restraints

- 4.3.1 Lack of Adequate Reimbursement

- 4.3.2 Stringent Regulatory Framework

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Low Slice

- 5.1.2 Medium Slice

- 5.1.3 High Slice

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Neurology

- 5.2.3 Cardiovascular

- 5.2.4 Musculoskeletal

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Centers

- 5.3.3 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Canon Medical Systems Corporation

- 6.1.2 Fujifilm Holdings Corporation

- 6.1.3 GE Healthcare

- 6.1.4 Shimadzu Corporation

- 6.1.5 Koning Corporation

- 6.1.6 Koninklijke Philips NV

- 6.1.7 Neusoft Medical Systems Co. Ltd

- 6.1.8 Siemens Healthineers

- 6.1.9 Carestream Health

- 6.1.10 Planmeca Group (Planmed OY)

- 6.1.11 Stryker Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS