PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536899

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536899

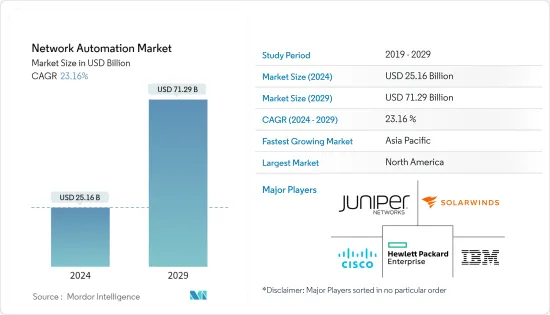

Network Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Network Automation Market size is estimated at USD 25.16 billion in 2024, and is expected to reach USD 71.29 billion by 2029, growing at a CAGR of 23.16% during the forecast period (2024-2029).

The network automation market has significantly grown in recent years, driven by the increasing complexity of networks and the need for efficient management solutions. The key driver behind this growth is the rising adoption of cloud computing and virtualization technologies, which has necessitated more agile and scalable network infrastructures.

Key Highlights

- Software-defined networking (SDN) is integrated with network functions virtualization (NFV) technology to configure and change the network according to business or service goals while using network automation with virtualization. The SDN controls how the hardware devices operate. Administrators can create virtual software networks between virtual machines or manage multiple physical networks with networking software.

- Network virtualization and network automation are especially useful for environments that experience unplanned usage surges because the automated network can accommodate these surges by automatically redirecting network traffic to servers in less impacted areas of the network.

- The proliferation of IoT devices and the demand for real-time data processing have further fueled the need for automation to handle the sheer volume of network traffic and devices. Enterprises are recognizing the cost-saving benefits of automation by reducing manual errors, improving operational efficiency, and enabling faster service deployment.

- The shortage of skilled professionals in the network automation market presents a significant restraint for industries seeking to adopt advanced networking technologies. The complexity of network automation systems presents a significant challenge, necessitating expertise in programming, network architecture, and cybersecurity.

- Several macroeconomic factors significantly influence the network automation market. These include economic growth, global trade dynamics, interest rates, labor market conditions, regulatory shifts, technological advancements, geopolitical stability, digital transformation efforts, and sustainability considerations. These trends collectively shape the adoption and evolution of network automation technologies, enabling businesses and policymakers to make informed decisions.

Network Automation Market Trends

IT and Telecom End-user Industry is Expected to Hold Significant Market Share

- The surge in smartphone adoption and the expanding web-connected device count have strained existing telecom networks. Consequently, network operators grapple with bandwidth shortages and congestion, resulting in call drops and erratic network performance. It is when the demand for network automation comes into play.

- The growth of the market studied in the IT and telecom industry is driven by the increasing complexity of networks due to the proliferation of connected devices and services. The rollout of 5G networks demands scalable and flexible solutions, which automation provides.

- Automation improves network security by enabling rapid threat detection and response. It also enhances service quality by ensuring consistent network performance and reliability, improving user experiences and customer satisfaction.

- In February 2024, Dell Technologies unveiled a suite of solutions tailored to assist communications service providers (CSPs) in streamlining their network cloud and operational transformations. Leveraging its widespread experience in digital transformation and robust industry collaborations, Dell is crafting telecom solutions to mitigate risks for CSPs. These solutions are designed to streamline deployment, automate operations, and simplify support and lifecycle management for disaggregated network cloud infrastructures.

- In May 2024, Tata Communications, a prominent player in the global communication technology sector, introduced Tata Communications CloudLyte. This advanced platform is fully automated and focuses on edge computing, aiming to equip enterprises for success in an increasingly data-centric environment. Tata Communications CloudLyte stands out in edge computing, offering a versatile architecture that is agnostic to access methods, cloud providers, and infrastructure, making it a fitting choice for enterprises globally.

- GSMA estimates that the total number of IoT connections will double between 2021 and 2030, reaching 37.4 billion. The expanding IoT ecosystem assists it. Licensed cellular IoT connections in the focus regions will double between 2021 and 2030, reaching 156 million. Therefore, rather than being a technology by itself, IoT deployment integrates various technologies related to sensing, automation, software, and cloud computing.

- With businesses embracing hyperconnectivity and technologies such as 5G and IoT gaining momentum, the demand for real-time data processing, low-latency applications, and smart decision-making has become paramount, driving the market's growth opportunities significantly.

North America is Expected to Hold Significant Market Share

- With the most significant market share in North America, the United States is at the forefront of the network automation market. This is underpinned by the robust presence of major solution providers such as Cisco, IBM, SolarWinds, VMWare, Extreme Networks, and Juniper Networks.

- The region is poised for a swift surge in the adoption and implementation of 5G technology. As per Ericsson's study, the total number of 5G subscriptions is projected to soar to an estimated 420 million by 2028, up from a mere 260 million in 2023. This rise in the adoption of 5G is set to fuel a greater need for advanced network services, subsequently spurring the need for increased network automation.

- The rise of various advanced technologies, such as SaaS-based applications, network analytics, DevOps, and virtualization, has spurred users and businesses in North America to adopt network automation solutions. These include intent-based networking, SD-WAN, and various network automation tools.

- By end-user industry, the IT and telecom industry is poised for the most significant growth in the North American network automation market. This surge is mainly driven by the growing demand for efficient network management, the rollout of 5G technology, and the expansion of cloud services. As data traffic and connected devices multiply, automated solutions become essential for handling complex network operations and ensuring cybersecurity.

Network Automation Industry Overview

The network automation market is highly fragmented, with major players like Cisco Systems Inc., Juniper Networks Inc., IBM Corporation, Hewlett Packard Enterprise, Development LP, and SolarWinds Inc. Market players adopt strategies like partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2024: IBM announced its acquisition of Pliant, a prominent network and IT infrastructure automation product provider. Pliant's capabilities are crucial for automating network and IT infrastructure tasks and abstracting these functions to the application layer. This gives applications and developers maximum control over simplified provisioning and infrastructure management directly within applications.

- January 2024: Juniper Networks unveiled the industry's pioneering AI-native networking platform. This platform is specifically engineered to harness AI, guaranteeing optimal experiences for operators and end-users. Juniper's platform is drawn from seven years of insights and data science. It is meticulously crafted to deliver reliability, measurability, and security across all connections, whether for devices, users, applications, or assets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Data Center Network

- 5.1.2 Rising Trend of Connected Devices

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Professional Across Industries

6 MARKET SEGMENTATION

- 6.1 By Network Type

- 6.1.1 Physical

- 6.1.2 Virtual

- 6.1.3 Hybrid

- 6.2 By Component

- 6.2.1 Solution Type

- 6.2.1.1 Network Automation Tools

- 6.2.1.2 SD-WAN and Network Virtualization

- 6.2.1.3 Intent-based Networking

- 6.2.2 Service Type

- 6.2.2.1 Managed Service

- 6.2.2.2 Professional Service

- 6.2.1 Solution Type

- 6.3 By Deployment

- 6.3.1 Cloud

- 6.3.2 On-premise

- 6.3.3 Hybrid

- 6.4 By End-user Industry

- 6.4.1 IT and Telecom

- 6.4.2 Manufacturing

- 6.4.3 Energy and Utility

- 6.4.4 Banking and Financial Services

- 6.4.5 Education

- 6.4.6 Other End-user Industries

- 6.5 By Geography***

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Juniper Networks Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Hewlett Packard Enterprise Company

- 7.1.5 Solarwinds Corporation

- 7.1.6 Fortra LLC

- 7.1.7 Open Text Corporation

- 7.1.8 NetBrain Technologies Inc.

- 7.1.9 Arista Networks Inc.

- 7.1.10 Extreme Networks Inc.

- 7.1.11 BMC Software Inc.

- 7.1.12 Fujitsu Limited

- 7.1.13 Broadcom Inc.

- 7.1.14 Nuage Networks (Nokia Corporation)

- 7.1.15 Forward Networks Inc.

- 7.1.16 AppViewX Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET