PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642123

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642123

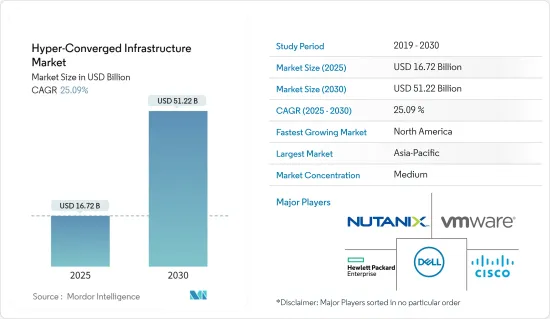

Hyper-Converged Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Hyper-Converged Infrastructure Market size is estimated at USD 16.72 billion in 2025, and is expected to reach USD 51.22 billion by 2030, at a CAGR of 25.09% during the forecast period (2025-2030).

Key Highlights

- Hyper-convergence infrastructure (HCI) has emerged as a transformative solution within the IT industry, revolutionizing the way organizations manage their data centers. The market for HCI has experienced significant growth and adoption as businesses seek to streamline their infrastructure, enhance operational efficiency, and embrace digital transformation.

- The increasing adoption of cloud computing has been a major driving factor for the hyper-converged infrastructure market. Enterprises across various industries are shifting their workloads to the cloud to leverage its scalability, cost-effectiveness, and flexibility. HCI solutions complement cloud environments by seamlessly integrating on-premises and cloud resources. With HCI, organizations can easily migrate workloads between private and public clouds, enabling hybrid cloud deployments that combine the benefits of both environments. This synergy between HCI and cloud computing has accelerated the market growth and is expected to continue driving the demand for hyper-converged infrastructure solutions.

- Data center virtualization and consolidation have become imperative for organizations seeking to optimize their IT infrastructure and reduce operational costs. Hyper-converged infrastructure offers a consolidated approach to data center management, enabling organizations to combine multiple components into a single, unified system. By leveraging virtualization technologies, HCI enables the efficient allocation and utilization of computing resources, leading to improved performance and reduced hardware footprint. The scalability and flexibility offered by HCI make it an ideal solution for data center consolidation and virtualization initiatives. As a result, the market for hyper-converged infrastructure is experiencing substantial growth driven by the demand for efficient data center operations.

- The global hyper-converged infrastructure market is experiencing increasing demand due to various applications, leading to greater efficiency in IT infrastructure. This surge in demand is fueled by the ability of hyper-converged infrastructure systems to safeguard data within on-premises data centers, offering features such as snapshots, replication, and encryption. Consequently, organizations across various sectors are seeking these solutions.

- However, the high initial investment cost of implementing HCI solutions is hampering the market. While HCI offers numerous benefits, including simplified management, improved scalability, and reduced operational costs, the upfront investment required to deploy these solutions can be significant. The costs of hardware, software licenses, and professional services can be challenging, particularly for small and medium-sized enterprises (SMEs) with limited IT budgets. The high initial investment cost is a barrier to adoption, hindering market growth. However, as the market matures and technology advancements occur, the cost of HCI solutions is expected to decline, making them more accessible to a broader range of organizations.

- The COVID-19 pandemic significantly accelerated digital transformation initiatives across industries. Organizations worldwide realized the importance of agile and resilient IT infrastructure to support remote work, online collaboration, and digital services. Hyper-converged infrastructure enabled these transformations by providing a scalable and flexible infrastructure foundation. The pandemic highlighted the need for businesses to be agile and adaptable, leading to increased adoption of HCI solutions. As a result, the post-COVID-19 era is expected to witness a further boost in the hyper-converged infrastructure market as organizations continue to invest in technologies that enhance their digital capabilities.

Hyper converged Infrastructure Market Trends

Growing Need for Enhanced Data Protection Driving the Market Growth

- Organizations today have a growing need for reliable and high-performance storage. Hyperconverged infrastructure (HCI) provides a secure and efficient solution by integrating networking, storage, and computation into a single system. This consolidation of resources streamlines management, reduces costs, and is considered crucial by many enterprises for their strategic IT priorities.

- The market for HCI is expanding due to the increasing adoption of HCI solutions, particularly in areas such as data security and disaster recovery. The widespread use of digital technology platforms like social media and knowledge platforms has also contributed to the growing demand for HCI. According to the IBM Data Breach's recent report, the average cost of data breaches has increased by 2.6% to USD 4.35 million, with penalties included. HCI systems mitigate the risk of data security breaches through their components and applications, and they often incorporate high-security AMD processors with security capabilities.

- Furthermore, HCI offers improved data security and scalability compared to traditional storage solutions. As the number of connected devices and the Internet of Things (IoT) continue to rise, the ability of HCI to gather and store analytics in a centralized management system becomes increasingly valuable. This feature aligns well with the future of 5G networks, where HCI's ability to view collected data through a unified interface proves advantageous. According to the GSMA, 5G connections are expected to surpass 1 billion this year and reach 2 billion by 2025, further driving the HCI market.

- HCI is optimized for virtual workloads, similar to public cloud-based services, and offers flexible, consumption-based infrastructure economics. It enables enterprises to rapidly scale their resources by adding HCI building blocks, allowing them to respond quickly to business demands and enhance IT service agility. With essential cloud computing services such as centralized administration, computation, storage, and data security embedded into hyper-converged systems, HCI becomes a comprehensive solution.

- Automation and machine learning are widely recognized as productivity boosters for businesses, enabling improved application performance and handling large amounts of data. HCI leverages AI to handle workload demands, optimize application workloads, and optimize storage. By bridging the gaps between on-premises private cloud, public cloud, and existing data center infrastructure, HCI in a hybrid multi-cloud model allows businesses to manage end-to-end data workflows and ensure easy accessibility of data for AI applications. The increasing corporate investment in AI, as highlighted by the Artificial Intelligence Index previous year's report, also drives the HCI market forward, with last year's global investment reaching almost USD 94 billion, a significant increase from the prior year's acquisition of USD 67.85 billion.

North America is Expected to Register the Fastest Growth

- The expansion of hyper-scale cloud service providers in the region primarily drives the growth of the HCI market in North America. Colocation services have also experienced growth in both the wholesale and retail sectors. The demand for infrastructure to support virtual desktops has increased due to rising mobile data usage and the implementation of bring-your-own-device (BYOD) regulations. As a result, HCI's market share is expected to increase in North America.

- Several data center companies have made significant investments in hyperscale data centers. Equinix, for instance, has announced plans to build 32 hyperscale data centers in major global markets. With a substantial investment of over USD 6.9 billion and a total capacity of 600 megawatts, Equinix aims to expand its presence and capitalize on the growing hyper-scale data center landscape. The increasing number of regional data centers will drive the HCI market further.

- Partnerships and collaborations are also shaping the HCI market in North America. For instance, Lenovo and Kyndryl expanded their collaboration to develop and deliver scalable hybrid and advanced computing implementations and cloud solutions. Leveraging Lenovo's expertise in PCs, storage, and server performance, along with Kyndryl's IT infrastructure services, the partnership aims to provide customers with comprehensive solutions across the hybrid cloud, HCI, and advanced computing applications.

- Moreover, the surge in enterprise deployments of HCI has led to a growing demand for software-defined storage. In response to this trend, DataCore Software acquired Caringo Inc., a specialist in object storage. This acquisition enables DataCore Software to offer a unified block, file, and object storage package. Caringo's Swarm platform, designed for hyperscale data access and storage, addresses data governance needs and reduces reliance on hardware. The latest version of DataCore's data management solution expands data access capabilities across distributed storage resources.

Hyper converged Infrastructure Industry Overview

The hyper-converged infrastructure market is moderately competitive and has a few major players. Some of the players currently dominate the market in terms of market share. However, with the advancement in infrastructure services across the cloud platform, new players are increasing their market presence, expanding their business footprint across emerging economies. The Key players in the market are continuously making partnerships, mergers, and investments to retain their market position.

In February 2023, Huawei announced its plans to accelerate the digital transformation of enterprises by implementing advanced technologies such as big data, artificial intelligence, edge computing, and intelligent manufacturing. In this context, hyper-converged infrastructure is evolving rapidly, shifting from traditional data centers to the edge, from structured to unstructured data, and from single general-purpose computing power to diversified computing power. This evolution has become one of the mainstream approaches for constructing data centers.

Moreover, to support this trend, Huawei is preparing to launch its hyper-convergence strategy and new products like Kunpeng Hyperconvergence, Blue Whale Application Mall, hyper-convergence software, and supporting tools. These offerings will comprehensively upgrade ecosystem development, user experience, and business capabilities.

In April 2022, Equinix and Dell expanded their partnership to provide hyper-converged data center offerings. As part of this expansion, Equinix extended its Equinix Metal line of bare metal appliances. Moreover, the expansion includes introducing several new offerings, including Dell PowerStore on Equinix Metal, Dell VxRail on Equinix Metal, and Dell EMC PowerProtect DDVE on Equinix Metal. These new solutions aimed to deliver enhanced capabilities and performance by combining Dell's advanced hardware with Equinix's robust bare metal infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for Enhanced Data Protection

- 5.1.2 Rising Demand for Integration Over Cloud Platform

- 5.2 Market Restraints

- 5.2.1 Loss of Data Privacy Over the Business Eco-system

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Professional

- 6.1.2 Managed

- 6.2 By Organization Type

- 6.2.1 Large Enterprise

- 6.2.2 Small & Medium Enterprise

- 6.3 By End-user Industry

- 6.3.1 IT & Telecommunication

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Government and Defence

- 6.3.6 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nutanix Inc.

- 7.1.2 Dell Inc.

- 7.1.3 VMware Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Cisco System Inc.

- 7.1.6 Oracle Corp.

- 7.1.7 Microsoft Corp.

- 7.1.8 NetApp Inc.

- 7.1.9 IBM Corp. (Red Hat Inc.)

- 7.1.10 Huawei Technologies Co. Ltd

- 7.1.11 StarWind Software Inc.

- 7.1.12 Datacore Software Corp.

- 7.1.13 Maxta Inc.

- 7.1.14 Pivot3 Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS