PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690101

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690101

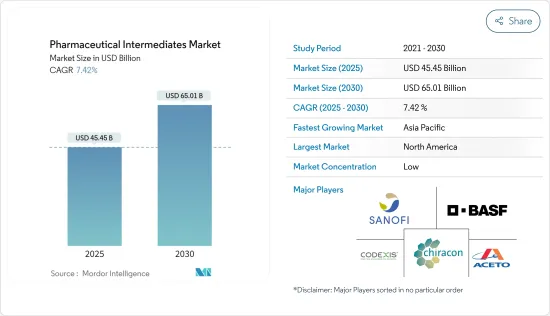

Pharmaceutical Intermediates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Pharmaceutical Intermediates Market size is estimated at USD 45.45 billion in 2025, and is expected to reach USD 65.01 billion by 2030, at a CAGR of 7.42% during the forecast period (2025-2030).

COVID-19 pandemic had a significant impact on the market studied. According to a study that was published in the American Chemical Society Pharmacology and Translational Science, 2020, new potential therapeutics for COVID-19 were discovered using a combined virtual and experimental screening strategy. Furthermore, they choose among the medications that were already in use and were examined to check for structural similarity against a library of almost 4,000 medications that were already in use, with hydroxychloroquine (HCQ) serving as a reference medication. The study suggested remdesivir and favipiravir therapies as prospective adjuvants in COVID-19 treatment and zuclopenthixol, nebivolol, and amodiaquine as potential candidates for clinical trials against the early phase of the SARS-CoV-2 infection. Thus, the pharmaceutical intermediates market witnessed significant growth during the covid pandemic and it is observed that even after the pandemic, the demand for pharmaceutical intermediates is high in the global market.

Specific factors that are driving the market growth include the increasing prevalence of chronic diseases and growing R&D initiatives and activities in the pharmaceutical industry. Given that these pharma intermediates are used in the treatment of cancer detection and a variety of chronic diseases, the rise in the prevalence of chronic diseases is projected to propel market expansion in the area under study. For instance, chronic diseases account for around 41 million annual fatalities, or 71% of all fatalities worldwide, according to the WHO's key facts on non-communicable diseases published in April 2021. The high fatality rate from these diseases increases the demand for early intervention, which in turn propels the market's expansion.

The market is expected to develop due to the rising prevalence of respiratory ailments such as lung cancer, chronic obstructive pulmonary diseases, and others. For instance, the WHO stated in its January 2022 report that Chronic Obstructive Pulmonary Disease (COPD) is the 3rd most common cause of morbidity and mortality globally. Low- and middle-income nations (LMIC) countries contribute largely to the global rise in prevalence of COPD. The necessity for effective treatment of the disease is brought on by the increasing prevalence of chronic obstructive pulmonary disease which is expected to increase the market growth.

There has been an upsurge in the usage of advanced technologies, such as high throughput, bioinformatics, and combinatorial chemistry for better drug candidate identification. The discovery and development of novel drugs to treat, prevent, or cure several diseases, including cancer, diabetes, cardiovascular disorders, and chronic kidney disease, has been accelerated by the significant rise in disease incidence rates around the world. The United States health care spending climbed 9.7% to reach USD 4.3 trillion in 2021, a substantially greater rate than the 4.2% increase recorded in 2020, according to the CMS data published in March 2022. Additionally, increased investments in R&D are a significant driver of market expansion. For instance, JSR life sciences introduced a corporate venture fund in March 2021 with a focus on small and developing biotech, attracting clients to its range of life sciences services. Hence, owing to the rising R&D activities in the pharmaceutical industry, the usage of pharmaceutical intermediates is expected to observe strong growth as well.

However, stringent regulatory issues regarding certain pharmaceutical intermediate substances are expected to hinder market growth.

Pharmaceutical Intermediates Market Trends

Cardiovascular Drugs Hold Significant Share in the Global Pharmaceutical Intermediates Market

The burden of heart disease on the global healthcare system is on the rise. One of the main elements driving the market expansion of pharmaceutical intermediates is the increase in the incidence of chronic cardiovascular disorders such as heart failure and coronary artery diseases. Ischemic heart disease (IHD) is a primary cause of death worldwide, according to a report published in the Cureus Journal of Medical Science in July 2021. The same report stated that around 126 million people worldwide (1,655 per 100,000), or roughly 1.72% of the world's population are affected by ischemic heart disease. By 2030, it is anticipated that there would be more than 1,845 cases of ischemic heart disease per 100,000 people worldwide.

Furthermore, risk factors associated with heart disease are on the rise across several countries which is boosting the prevalence. For instance, as of the year 2022, around 11.10% of men and 3.10% of women in France are alcoholics, as per the data from World Population Review. As alcoholism increases the chances of heart disease, it has a significant impact on market growth. Similarly, the UK Factsheet by the British Heart Foundation, released in July 2021, estimated that 7.6 million people in the United Kingdom were affected by heart and circulation disorders. Additionally, according to the same source, heart and circulation illnesses are responsible for more than 1,60,000 deaths annually in the United Kingdom, or 25% of all fatalities in the country. This high prevalence of cardiovascular diseases is generating a huge demand for cardiovascular drugs, which, in turn, is expected to propel the growth in the need for various pharmaceutical intermediates.

Hence, owing to the aforementioned factors, the concerned segment of the pharmaceutical intermediates market is expected to observe steady growth over the forecast period.

North America Dominates the Global Pharmaceutical Intermediates Market

North America dominates the Pharmaceutical Intermediates products market primarily due to the advanced research and development facilities mainly across the United States and Canada. In addition, the rising prevalence of various chronic conditions is also fueling market growth across the region.

Growing government support for healthcare in the United States is one element contributing to the market's expansion in that country. For instance, the National Institutes of Health (NIH) received more than USD 700 billion in public funding over the past few decades, according to a 2021 study from the Congressional Budget Office. Six grants were given out by the Food and Drug Administration (FDA) in 2020 to fund new clinical trials and advance the creation of pharmaceuticals for the treatment of uncommon diseases. The need for pharmaceutical intermediates, which are widely used in the drug discovery process, will increase as a result. According to "clinicaltrials.gov," there were 443,207 registered clinical studies in the United States as of November 2022. Similarly, according to ClinicalTrial.gov, Canadian pharmaceutical companies and research institutions have strong R&D pipelines as of the year 2022. Of the 5,659 new studies in the pipeline at that time that were in various stages of evaluation, 1,397 (24%) were in Phase III clinical trials that had received the Food and Drug Administration (FDA) or European Medicines Evaluation Agency (EMA) approval, covering a wide range of therapeutic areas.

As infectious diseases become more widespread, attention is being paid more and more to their diagnosis and treatment. The Centers for Disease Control and Prevention (CDC) estimated that in 2020, there were approximately 7,174 tuberculosis cases discovered in the United States, translating to a rate of 2.2 per 100,000 people. Thus, a high prevalence of tuberculosis patients drives up the demand for therapy, which in turn drives the market for pharmaceutical intermediates. The CDC reported in a February 2022 article that each year in the United States, Salmonella bacteria causes around 1.35 million infections, 26,500 hospitalizations, and 420 fatalities. The nation's healthcare system is burdened by the large number of infectious infections that are reported each year. As a result, the market under study may experience growth due to the extraordinary rise in demand for treatments for these diseases. Thus, the abovementioned factors are expected to increase market growth.

Pharmaceutical Intermediates Industry Overview

The global pharmaceutical intermediates market is competitive and consists of a few major players. Companies like Aceto Corporation, BASF SE, Chiracon GmbH, Yin-sheng Bio-tech Co., Ltd., Dishman Group, Green Vision Life Sciences, Codexis, Inc., Sanofi SAIS, Vertellus Holdings LLC., among others, hold the substantial market share in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases

- 4.2.2 Growing R&D Initiatives and Activities in the Pharmaceutical Industry

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Issues Regarding Certain Pharmaceutical Intermediate Substances

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Chemical Intermediate

- 5.1.2 Bulk Drug Intermediate

- 5.1.3 Others

- 5.2 By Application

- 5.2.1 Analgesics

- 5.2.2 Anti-Infective Drugs

- 5.2.3 Cardiovascular Drugs

- 5.2.4 Oral Antidiabetic Drugs

- 5.2.5 Antimicrobial Drugs

- 5.2.6 Others

- 5.3 By End-User

- 5.3.1 Biotech and Pharma Companies

- 5.3.2 Research Institutions

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 A.R. Life Science

- 6.1.2 Aceto Corporation

- 6.1.3 BASF SE

- 6.1.4 Chiracon GmbH

- 6.1.5 Codexis, Inc.

- 6.1.6 Dishman Group

- 6.1.7 Green Vision Life Sciences

- 6.1.8 Lianhetech

- 6.1.9 Midas Pharma GmbH

- 6.1.10 Sanofi SAIS

- 6.1.11 Vertellus Holdings LLC

- 6.1.12 Yin-sheng Bio-tech Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS