PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1438443

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1438443

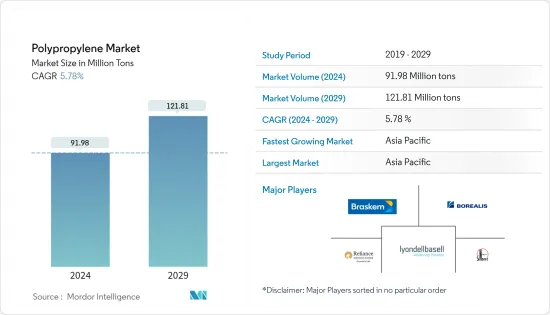

Polypropylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Polypropylene Market size is estimated at 91.98 Million tons in 2024, and is expected to reach 121.81 Million tons by 2029, growing at a CAGR of 5.78% during the forecast period (2024-2029).

A slight decline in the demand for polypropylene has been observed due to COVID-19. A drastic slowdown was witnessed in the construction and automotive sector, where polypropylene is in high demand. With the resumption of operations in major end-user industries, it significantly recovered in 2022.

Key Highlights

- Over the short term, major factors driving the market studied are the increasing usage of plastics to reduce vehicle weight and enhance fuel economy and the growing demand for flexible packaging.

- On the other hand, the presence of different substitute products in the market is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- The increasing trends of recycled polypropylene are likely to act as an opportunity in the future.

- The Asia-Pacific dominated the market across the world and is expected to dominate in the forecast period, with the largest consumption from countries such as China and India.

Polypropylene Market Trends

Increasing Demand for Injection Molding to Dominate the Application Segment

- Polypropylene is majorly used for injection molding and is mostly available for this application in the form of pellets. Polypropylene is easy to mold, and it flows very well because of its low melt viscosity.

- Injection molding technology is used to produce plastics that are used extensively in electrical and electronic applications. These plastics are widely used in the manufacturing of electrical and electronic devices.

- Polypropylene is well-suited to a wide range of product types due to its numerous flexible uses. One of the most frequent applications is the living hinge, a one-piece hinged design typically used in consumer items such as caps. Innumerable products made from the process include children's toys, sporting goods, closures, automotive applications, food trays, cups, to-go containers, household goods, and appliances like dishwashers.

- According to HUBS, a globally leading material manufacturing company, polypropylene accounts for 35-40% of worldwide injection molding output, followed by other materials such as ABS (25%), polyethylene (15%), and polystyrene (10%).

- The high growth of the packaging and chemical processing industries across the world is expected to offer a favorable market scenario for injection molding. Owing to the geographical advantage of distribution to the rapidly growing Asia-Pacific region, the consumption of injection-molded pallets may increase drastically.

- Moreover, the adoption of lightweight components for the automobile to increase fuel efficiency is expected to favor the demand for the market studied in the forecast period.

- All the aforementioned factors are expected to boost the market's demand.

Asia-Pacific to Register the Fastest Growth

- The Asia-pacific polypropylene market is growing at a fast pace, driven by countries like China and India. Polypropylene is widely used in the automotive, consumer products, electronics, and packaging industries. With robust growth in these industries and government support, the demand for polypropylene is projected to increase at a healthy pace during the forecast period.

- China is the world's largest vehicle market and will continue to be the largest market by both annual sales and manufacturing output, with domestic production expected to reach 35 million vehicles by 2025.

- Moreover, as per the OICA, Chinese automotive manufacturers manufactured 26,082,220 vehicles in 2021, registering a growth of 3% compared to 2020.

- In India, according to the Packaging Industry Association of India (PIAI), the sector is growing at 22% to 25% per annum and is expected to reach USD 204.81 billion by 2025. The Indian packaging industry made a mark with its exports and imports, driving technology and innovation growth in the country and adding value to the various manufacturing sectors.

- The packaging industry is enacting the role of catalyst in promoting the huge growth of the polypropylene market in India. Furthermore, the country has been exhibiting a significant demand for packed foods in the past few years, which is expected to continue during the forecast period, thus boosting the demand for the market studied.

- As per the National Investment Promotion & Facilitation Agency, the automobile industry contributes 7.1% of India's GDP and 49% of its manufacturing GDP. Moreover, according to Organisation Internationale des Constructeurs d'Automobiles, the Indian automotive industry manufactured 4,399,112 vehicles, which is almost 30% more than in 2020.

- Such growth in various industries is expected to drive the market for polypropylene in the Asia-Pacific region during the forecast period.

Polypropylene Industry Overview

The global polypropylene market is fragmented in nature. The top five companies hold around 35% of the global market share in terms of production capacities. Some of the major players in the market include China Petroleum & Chemical Corporation (SINOPEC), LyondellBasell Industries Holdings BV, Borealis AG, Braskem, and Reliance Industries Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Plastics to Reduce Vehicle Weight and Enhance Fuel Economy

- 4.1.2 Growing Demand for Flexible Packaging

- 4.2 Restraints

- 4.2.1 Availability of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trends

- 4.6 Import-Export Trends

- 4.7 Feedstock Analysis

- 4.8 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Homopolymer

- 5.1.2 Copolymer

- 5.2 Application

- 5.2.1 Injection Molding

- 5.2.2 Fiber

- 5.2.3 Film and Sheet

- 5.2.4 Other Applications (Extrusion Coating, Blow moulding)

- 5.3 End-user Industry

- 5.3.1 Packaging

- 5.3.2 Automotive

- 5.3.3 Consumer Products

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user industries (Textiles, Construction)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Borealis AG

- 6.4.2 Braskem

- 6.4.3 China National Petroleum Corporation

- 6.4.4 China Petrochemical Corporation (SINOPEC)

- 6.4.5 Daelim Co. Ltd

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Formosa Plastics Corporation

- 6.4.8 INEOS

- 6.4.9 LG Chem

- 6.4.10 Lotte Chemical Corporation

- 6.4.11 LyondellBasell Industries Holdings BV

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Mitsui Chemicals Inc. (Prime Polymer Co. Ltd)

- 6.4.14 Reliance Industries Limited

- 6.4.15 SABIC

- 6.4.16 SIBUR International GmbH

- 6.4.17 Sumitomo Chemical Co. Ltd

- 6.4.18 Total Energies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Recycled Polypropylene