PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1438095

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1438095

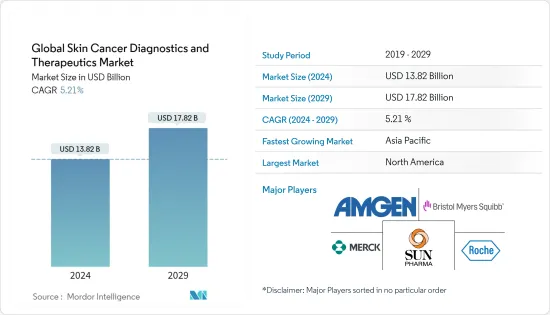

Global Skin Cancer Diagnostics and Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Global Skin Cancer Diagnostics and Therapeutics Market size is estimated at USD 13.82 billion in 2024, and is expected to reach USD 17.82 billion by 2029, growing at a CAGR of 5.21% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic had a significant impact on the market studied. After the pandemic began, the World Health Organization (WHO) guidelines suggested that chronic disease patients remain indoors. Hence, this hampered the skin cancer diagnostic market. However, the surge in the number of research for studying the impact of the treatment delay on patients with non-melanoma skin cancer (NMSC) or melanoma cancer amid Covid-19 increased. A study, 'The impact of the Covid-19 pandemic on quality of life in skin cancer patients' published in August 2021, mentioned that due to an immunocompromised/-suppressed status and dependent on the underlying tumor disease and burden, cancer patients might be at an increased risk of developing severe Covid-19 disease and requiring treatment in an intensive care setting. Thus, the increased skin cancer incidences during the pandemic increased the diagnostics for the same and created demand for new advanced therapeutics for treatment. Therefore, the pandemic is predicted to have a positive impact on skin cancer diagnostics and therapeutics during the pandemic phase.

Certain factors driving the market growth include increasing incidence of skin cancer, extensive research and development (R&D) pipelines, and rising awareness about skin cancer. For instance, updated in February 2022 by the American Society of Clinical Oncology, an estimated 324,635 people were diagnosed with melanoma in 2020, and in 2020, about 2,400 cases of melanoma were estimated to be diagnosed in people aged 15 to 29 in the United States. Thus, the prevalence of skin cancer among the population is augmenting the growth of the market studied.

Moreover, the increased R&D is predicted to drive the demand for skin cancer therapeutics over the forecast period. For instance, in January 2022, Immunocore, a commercial-stage biotechnology company pioneering the development of a novel class of T cell receptor (TCR) bispecific immunotherapies designed to treat a broad range of diseases, including cancer, received approval from the United States Food and Drug Administration (FDA) for KIMMTRAK (tebentafusp-tebn) for the treatment of HLA-A*02:01-positive adult patients with unresectable or metastatic uveal melanoma (mUM). Additionally, In April 2022, barnaclanic+ launched its Dermatological Diagnosis Unit for the diagnosis and treatment of skin cancer, and the new unit will also have the latest technology on the market in dermatological diagnosis and skin cancer. Thus, this increasing R&D is expected to drive the growth of the studied market.

Therefore, the factors mentioned above are attributed collectively to the studied market growth over the forecast period. However, the excessive cost associated with therapies and stringent regulatory frameworks is expected to hinder the market growth over the forecast period.

Skin Cancer Diagnostics and Therapeutics Market Trends

Non-Melanoma by Cancer Type Segment is Expected to Grow Over the Forecast Period

Non-melanoma skin cancer starts in skin cells, and a cancerous (malignant) growth is a group of cancer cells that can grow into and destroy nearby tissue. It can also spread (metastasize) to other parts of the body, but this is rare with non-melanoma skin cancer. Thus, the increasing cases of non-melanoma are anticipated to drive the growth of the segment.

The research increased during the pandemic to analyze the impact of a pandemic on all skin cancers. A study 'The impact of treatment delay on skin cancer in COVID-19 era: a case-control study' published in December 2021 mentioned in their discussion that the COVID-19 pandemic is associated with an increased skin cancer incidence and more skin cancer operations were performed in the post-lockdown period which was significant only for squamous cell carcinoma (SCC) a type of non-melanoma cancer. Thus, the demand for diagnostics and improved therapeutics increased during the pandemic, marking a positive impact on the non-melanoma segment.

The Skin Cancer Foundation data updated in May 2022 shows that about 90% of non-melanoma skin cancers are associated with exposure to ultraviolet (UV) radiation from the sun. As per the estimates of the Skin cancer Foundation, basal cell carcinoma (BCC) is the most generic form of skin cancer, and an estimated 3.6 million cases of BCC are diagnosed in the United States each year. And the source mentioned above also reported that the annual cost of treating skin cancers in the United States is estimated at USD 8.1 billion, which is about USD 4.8 billion for non-melanoma skin cancers and USD 3.3 billion for melanoma. Thus, the incidence of non-melanoma type skin cancer and associated treatment costs is anticipated to create opportunities for advanced therapeutics and diagnostics in the United States and other counties across the globe. Thereby, it is expected to boost the overall segment growth.

The insights on increased R&D in the segment are also predicted to drive segment growth. For instance, in December 2021, researchers and radiologists at Northampton General Hospital NHS Trust introduced Skin Brachytherapy, a highly targeted radiotherapy technique used to treat certain types of basal cell or squamous cell skin cancers.

Hence, the non-melanoma segment is growing, and it is expected to have significant growth over the forecast period. Hence, driving the growth of the studied market.

North America is Expected to Dominate the Market Over the Forecast Period

North America is expected to dominate the overall skin cancer and therapeutics market throughout the forecast period. The market growth is due to factors like the increasing prevalence and incidence of skin cancers. The United States is expected to be the largest market in this region.

The well-established healthcare infrastructure-focused market players in research and development (R&D) for cancer therapeutics, coupled with recent product launches and the rising burden of skin cancer in the United States, are primary growth factors for the market in the country. For instance, in July 2021, Merck, known as MSD outside the United States and Canada, received approval from the Food and Drug Administration (FDA) for its expanded label for KEYTRUDA, Merck's anti-PD-1 therapy, as monotherapy for the treatment of patients with locally advanced cutaneous squamous cell carcinoma (cSCC) that is not curable by surgery or radiation. Additionally, in May 2022, Labcorp., one of the leading global life sciences companies, launched a new assay for treatment options for melanoma. The new test enables the measurement of Lymphocyte-activation gene 3 (LAG-3) expression levels by immunohistochemistry (IHC) in tumor tissue. LAG-3 is an immune-oncology target with demonstrable clinical benefits in patients with melanoma. The test is available for use in both clinical trials and the care and treatment of patients. These recent developments are expected to drive the skin cancer diagnostics and therapeutics demand in the country, driving the overall market growth in the region.

Furthermore, the Skin Cancer Foundation data updated in May 2022 shows that an estimated 197,700 cases of melanoma will be diagnosed in the United States in 2022. Among those, 97,920 cases will be in situ (noninvasive), confined to the epidermis (the top layer of skin), and 99,780 cases will be invasive, penetrating the epidermis into the skin's second layer (the dermis). Of the invasive cases, 57,180 will be men and 42,600 women. Thus, the incidence and prevalence of skin cancer in the country are demanding the development of advanced diagnostics and therapeutics in the country for treatment, propelling the overall market growth in the region.

Hence, as per the factors mentioned above, the skin cancer cases in the United States is anticipated to create opportunity for advanced skin cancer diagnostics and therapeutics, driving the overall market growth in the country.

Skin Cancer Diagnostics and Therapeutics Industry Overview

The skin cancer diagnostics and therapeutics market is competitive globally and regionally. The market consists of several major players who are engaged in continuous product development and launches. Some companies currently dominating the market are Abbott, Pfizer Inc., Sanofi SA, F. Hoffmann-La Roche Ltd, Labcorp., and sun pharmaceuticals industries limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Skin Cancer

- 4.2.2 Rising Awareness About Skin Cancer

- 4.2.3 Extensive Research and Developments

- 4.3 Market Restraints

- 4.3.1 High Cost Associated with Therapy

- 4.3.2 Stringent Regulatory Framework

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Cancer Type

- 5.1.1 Melanoma

- 5.1.2 Non-melanoma

- 5.2 By Type

- 5.2.1 Diagnosis

- 5.2.1.1 Dermatoscopy

- 5.2.1.2 Biopsy

- 5.2.1.3 Genetic Tests

- 5.2.1.4 Others

- 5.2.2 Therapeutics

- 5.2.2.1 Chemotherapy

- 5.2.2.2 Immunotherapy

- 5.2.2.3 Targeted Therapy

- 5.2.2.4 Others

- 5.2.1 Diagnosis

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Amgen, Inc.

- 6.1.3 Pfizer Inc.

- 6.1.4 Bristol-Myers Squibb Company

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 Sanofi

- 6.1.7 Merck & Co., Inc.

- 6.1.8 Novartis AG

- 6.1.9 QIAGEN

- 6.1.10 Sun Pharmaceutical Industries Ltd

- 6.1.11 Daiichi Sankyo Company, Limited

- 6.1.12 Labcorp

- 6.1.13 Sirnaomics, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS