PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444151

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444151

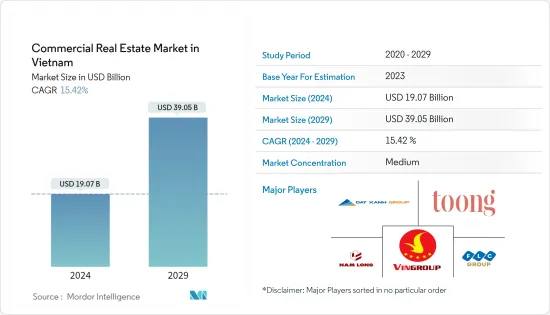

Commercial Real Estate in Vietnam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Commercial Real Estate Market in Vietnam Market size is estimated at USD 19.07 billion in 2024, and is expected to reach USD 39.05 billion by 2029, growing at a CAGR of 15.42% during the forecast period (2024-2029).

The COVID-19 pandemic caused a slowdown in the Vietnamese property market. However, many companies believe this is only temporary and hoping for a rebound once the virus is under control. Meanwhile, the government has identified public investment as a key solution to boost growth. A better infrastructure system could be seen as welcoming news for the real estate market for further development in the coming years.

Despite the signs of cyclical moderation in growth, Vietnam's economic outlook remains positive. Vietnam's economy saw strong growth, with laws that made foreigners invest in its development. As a result, there has been a surge in high-end real estate developments in the country.

The improvement in infrastructure supporting the tourism industry, which has always been one of the prioritized investment areas by Vietnam, has boosted the growth of many tourist cities in recent years. Local demand in Vietnam is also rising as Vietnamese entrepreneurs are looking for investment opportunities.

Vietnam Commercial Real Estate Market Trends

Growth in Vietnamese E-commerce to Drive the Industrial Real Estate Market

The Vietnamese e-commerce market is projected to continue growing in the post-pandemic period. The e-commerce revenue in Vietnam reached USD 11.8 billion in 2020, posting a growth rate of 18%. The Vietnamese e-commerce market recorded the fastest growth rate in Southeast Asia. E-commerce is expected to continue thriving post the COVID-19 pandemic, creating new consumption trends.

Since the outbreak, the demand for online purchases through e-commerce platforms has increased sharply. By 2021, more than 70% of Vietnam's population accessed the Internet, of which nearly 50% of consumers tried online shopping, and 53% of them used e-wallets and online payment.

E-commerce, particularly in logistic services and express delivery focusing on e-commerce, is now a prospering sector for investors. Recently, 4PL (4th party) logistics providers entered the market by offering more custom solutions to customers who need more flexibility in their shipping needs. The demand for industrial park real estate from investors entering the Vietnam market is also high. In the past, they often needed to find a land fund to develop with a scale of 5,000-10,000 m2. Up to now, it has increased to 10,000-50,000 m2. The market is also expected to see a significant increase in cold storage demand in support of essential medical services, such as the rotation and storage of the new COVID-19 vaccine.

Workplace Real Estate Continues to Grow in Vietnam

Currently, the demand for coworking spaces in Vietnam is driven by start-ups, freelancers, and small corporations. The growing demand has attracted domestic firms, global firms, and investment funds to Vietnam. Such spaces will continue to expand in terms of supply and offerings and attract start-ups as tenants, including small corporations looking to minimize costs and increase flexibility.

By the end of 2021, the total stock of Grade A and B reached 1,596,448 sq. m (NLA) in Hanoi. In Q4 2021, asking rents remained stable in existing projects in both grades. Asking rents of existing Grade A and Grade B offices were maintained at USD 24.6 per sq. m/month and USD 14.0 per sq. m/month, respectively.

In Q4 2021, the Ho Chi Minh City (HCMC) office market recorded a good revenue trend in vacancy and rental rates. In 2022, the market is expected to have 96,000 sq. m of new NLA from two Grade B buildings and one Grade A building.

Vietnam Commercial Real Estate Industry Overview

Commercial real estate in Vietnam has a medium level of market share concentration. International investors are also attracted to the Vietnamese market and are looking to invest in almost all segments, from office to retail and high-end hotels. Developers are active in creating new hospitality products for sales, most notable of which are coastal shophouse/shop villas in Phu Quoc and Ha Long.

In hospitality real estate, there is a need for developers in Vietnam to diversify their market by paying attention to the non-traditional market and bringing in professionals to manage their property. There is rising demand for quality office and retail stock in centralized places, with the Hanoi CBD in focus. The strength of the manufacturing and tourism sector will keep demand high for retail, office, and industrial units. Some of the players are Vin Group, Dat Xanh Group, FLC Group, Toong, Nam Long Investment, and Sun Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights

- 4.1 Current Economic Scenario and Consumer Sentiment

- 4.2 Commercial Real Estate Buying Trends - Socioeconomic and Demographic Insights

- 4.3 Government Initiatives, Regulatory Aspects for Commercial Real Estate Sector

- 4.4 Insights on Existing and Upcoming Projects

- 4.5 Insights on Interest Rate Regime for General Economy and Real Estate Lending

- 4.6 Insights on Rental Yields in Commercial Real Estate Segment

- 4.7 Insights on Capital Market Penetration and REIT Presence in Commercial Real Estate

- 4.8 Insights on Public-private Partnerships in Commercial Real Estate

- 4.9 Insights on Real Estate Tech and Start-ups Active in Real Estate Segment (Broking, Social Media, Facility Management, Property Management)

- 4.10 Impact of COVID-19 on the Market

- 4.11 Market Dynamics

- 4.11.1 Drivers

- 4.11.2 Restraints

- 4.11.3 Opportunities

5 Market Segmentation

- 5.1 By Type

- 5.1.1 Offices

- 5.1.2 Retail

- 5.1.3 Industrial

- 5.1.4 Logistics

- 5.1.5 Multi-family

- 5.1.6 Hospitality

- 5.2 By Key Cities

- 5.2.1 Ho Chi Minh City

- 5.2.2 Hanoi

- 5.2.3 Quang Ninh

- 5.2.4 Da Nang

- 5.2.5 Rest of Vietnam

6 Competitve Landscape

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Vingroup

- 6.2.2 Dat Xanh Group

- 6.2.3 FLC Group

- 6.2.4 Toong

- 6.2.5 Nam Long Investment Corporation

- 6.2.6 Coteccons Construction JSC

- 6.2.7 Hoa Binh Construction Group

- 6.2.8 Ricons Construction Investment JSC

- 6.2.9 Construction Corporation No.1 JSC

- 6.2.10 NEWTECONS Investment Construction JSC

- 6.2.11 Obayashi Viet Nam Corporation

- 6.2.12 Thai Son Construction Co. Ltd*

7 Future of the Market and Analyst Recommendations

8 Disclaimer