PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849965

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849965

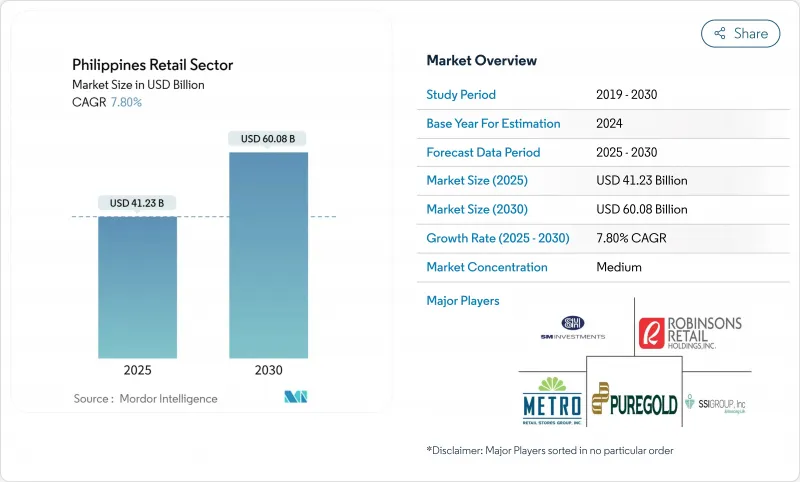

Philippines Retail Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Philippines retail market reached USD 41.23 billion in 2025 and is forecast to advance to USD 60.08 billion by 2030, reflecting a sturdy 7.8% CAGR.

Digital transformation, a rising middle-income segment, and steady remittance inflows underpin this trajectory. Household spending is rising from 5.0% in 2024 to 5.3% in 2025 as disposable incomes climb, encouraging retailers to broaden assortments and upgrade store formats. Simultaneously, the share of retail in national output is moving from 18.6% in 2022 toward 20% by late 2024, underscoring the sector's growing macroeconomic weight. Rapid e-commerce uptake, now 52.8% of transactions, has pushed retailers to integrate mobile wallets and social shopping, while massive public-private infrastructure projects lower logistics barriers and open provincial growth corridors.

Philippines Retail Sector Market Trends and Insights

Rising Disposable Incomes and Expanding Middle Class

Average per-capita income is expected to almost double from USD 3,541 in 2025 to USD 6,500 in 2030. This enlarges the consuming class and lifts demand for premium labels as well as modern shopping ambiances. Luxury categories are therefore growing at 12.21%-well above the Philippines retail market average. Retailers answer with wider private-label assortments, renovated store layouts, and loyalty programs that emphasize quality and experience. Department stores and specialty chains that curate global brands are seeing traffic from aspirational shoppers, while sari-sari owners leverage digital supply hubs to stock higher-margin goods.

Accelerating E-commerce Adoption and Digital Payments

Digital payments already account for 52.8% of retail transactions, overshooting the government's 50% target two years early. Monthly electronic transfers now approach 2.62 billion, worth USD 110 billion, and mobile wallet penetration exceeds 30 million active users. Retailers consequently embed click-and-collect counters, live-stream selling and single-cart checkout across channels. Social commerce thrives as 85% of shoppers expect live selling to grow, motivating MSMEs to extend reach nationally. Broad payment choice and friction-free returns reduce cart abandonment and build trust among first-time online buyers.

Chronic Traffic Congestion and Last-Mile Inefficiencies

Gridlock in Metro Manila inflates freight costs by up to 20% versus efficient cities. Retailers must over-invest in urban depots and widen delivery windows for perishables, eroding margins. Government freight-route mapping and "no truck ban" policies aim to cut delays, yet implementation lags and businesses still adopt AI routing tools alongside motorbike fleets to skirt bottlenecks.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Convenience-Oriented FandB Retailing

- Government Logistics Infrastructure Improvements

- Rising Utility and Operating Costs for Modern Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food and Beverage claimed 46.52% of the Philippines' retail market share in 2024, anchoring day-to-day traffic and buffering the sector against cyclical shocks. The Philippines' retail market size for this category benefits from robust tourism, hotel openings, and strong agricultural links with the United States. Layered onto staples, Cosmetics and Personal Care expands at a 10.2% CAGR, fueled by heightened wellness awareness and growing disposable incomes. Apparel, Electronics and Furniture register steady single-digit gains tied to urbanization and housing upgrades, while Confectionery and Ice Cream post 8% annual growth on rising leisure spending.

Expanding middle-income wallets allow premium gourmet grocers to carve niches, yet the mass-market grocery core remains vital. Imported delicacies and plant-based offerings sit alongside local rice and canned fish, illustrating basket polarisation. Multinational brands partner with sari-sari owners for rural penetration, whereas mall-based supermarkets emphasise experiential bakery corners and dine-in counters to extend dwell time.

Supermarkets and hypermarkets combined delivered 38.56% of Philippines retail market share in 2024, supported by Robinsons, SM Hypermarket and Savemore's dense outlet matrix. Their bundled promotions and loyalty schemes nurture repeat traffic, yet footfall is fragmenting as consumers explore faster fulfilment choices. The online grocery segment exceeded USD 1 billion in 2023 and will likely outpace headline Philippines retail market growth with a 15% CAGR anchored in mobile wallet habituation.

Convenience chains continue to seed secondary cities, reaching commuters and students after working hours. Department and specialty stores refocus on curation, leveraging beauty consultation and pet-care services to defend margins. Dark-store platforms test 15-minute delivery in Metro Manila, showing where the next incremental dollar of Philippines retail market size could emerge.

Philippines Retail Market is Segmented by Product Category (Food and Beverage, Personal and Household Care, and More), by Distribution Channel (Supermarkets / Hypermarkets, Convenience Stores, and More), by Retail Format (Modern Trade, Traditional Trade, and More), by Price Segment (Mass/Value, Premium, and Luxury), by Store Size (Large, Mid and More), by Region (Luzon, and More).

List of Companies Covered in this Report:

- SM Investments Corp. (SM Retail Inc.)

- Puregold Price Club Inc.

- Robinsons Retail Holdings Inc.

- Metro Retail Stores Group Inc.

- SSI Group Philippines

- Rustan Supercenters Inc.

- Alfamart Philippines

- Philippine Seven Corp. (7-Eleven)

- Golden ABC Inc.

- Mercury Drug Corp.

- Rose Pharmacy Inc.

- Ever Bilena Cosmetics Inc.

- AllDay Marts Inc.

- Landers Superstore / S&R

- Gaisano Capital Group

- Prince Retail Group

- WalterMart (WM Retail)

- LCC Supermarket

- Davao Central Warehouse Club Inc.

- MiniStop Philippines*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising disposable incomes and expanding middle class

- 4.2.2 Accelerating e-commerce adoption and digital payments

- 4.2.3 Growth of convenience-oriented FandB retailing

- 4.2.4 Government logistics infrastructure improvements

- 4.2.5 Overseas remittances fuelling discretionary consumption

- 4.2.6 Emergence of micro-fulfilment "dark stores"

- 4.3 Market Restraints

- 4.3.1 Chronic traffic congestion and last-mile inefficiencies

- 4.3.2 Rising utility and operating costs for modern formats

- 4.3.3 Dominance of informal sari-sari stores

- 4.3.4 VAT equalisation on foreign e-commerce platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Consumer Behaviour Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Category

- 5.1.1 Food and Beverage

- 5.1.2 Personal and Household Care

- 5.1.3 Apparel

- 5.1.4 Footwear and Accessories

- 5.1.5 Furniture

- 5.1.6 Toys and Hobbies

- 5.1.7 Electronics and Household Appliances

- 5.1.8 Other Products

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets / Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Department Stores

- 5.2.4 Specialty Stores

- 5.2.5 Online

- 5.2.6 Other Channels

- 5.3 By Retail Format

- 5.3.1 Modern Trade

- 5.3.2 Traditional Trade

- 5.3.3 Discount Stores and Warehouse Clubs

- 5.3.4 Omnichannel and Dark Stores

- 5.4 By Price Segment

- 5.4.1 Mass / Value

- 5.4.2 Premium

- 5.4.3 Luxury

- 5.5 By Store Size

- 5.5.1 Large-Format (Greater than 2,500 m2)

- 5.5.2 Mid-Format (400-2,500 m2)

- 5.5.3 Small / Micro (Less than 400 m2)

- 5.6 By Region

- 5.6.1 Luzon

- 5.6.2 Visayas

- 5.6.3 Mindanao

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 SM Investments Corp. (SM Retail Inc.)

- 6.4.2 Puregold Price Club Inc.

- 6.4.3 Robinsons Retail Holdings Inc.

- 6.4.4 Metro Retail Stores Group Inc.

- 6.4.5 SSI Group Philippines

- 6.4.6 Rustan Supercenters Inc.

- 6.4.7 Alfamart Philippines

- 6.4.8 Philippine Seven Corp. (7-Eleven)

- 6.4.9 Golden ABC Inc.

- 6.4.10 Mercury Drug Corp.

- 6.4.11 Rose Pharmacy Inc.

- 6.4.12 Ever Bilena Cosmetics Inc.

- 6.4.13 AllDay Marts Inc.

- 6.4.14 Landers Superstore / S&R

- 6.4.15 Gaisano Capital Group

- 6.4.16 Prince Retail Group

- 6.4.17 WalterMart (WM Retail)

- 6.4.18 LCC Supermarket

- 6.4.19 Davao Central Warehouse Club Inc.

- 6.4.20 MiniStop Philippines*

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment