PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403875

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403875

Canada Automotive Thermoplastic Polymer Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Canada Automotive Thermoplastic Polymer Composites Market is valued at USD 0.86 billion in 2024, and it is expected to reach USD 1.35 billion by 2029, registering a CAGR of 7.72% during the forecast period.

There was a rising interest in thermoplastic polymer composites over the past few years, owing to several advantages of these materials, including high volume processability, recyclability, superior damage tolerance, fracture toughness, and ability to produce complex shapes.

These composites found applications in different modes of transportation, from cars to underground trains. Among thermoplastic composites, long-fiber thermoplastics (LFTs) are being extensively used in the transportation sector.

The automotive industry was impacted due to high fuel prices. Furthermore, in the transportation industry, vehicle OEMs and suppliers use thermoplastic composites to reduce vehicle mass. Due to stringent emission regulations, automotive manufacturers are focusing on reducing the weight of the vehicle, as it helps in saving a noticeable amount of carbon dioxide emissions. A 10 kg weight reduction is estimated to reduce 1 gm of carbon dioxide per km.

Canada Automotive Thermoplastic Polymer Composites Market Trends

Glass Mat Thermoplastic (GMT) is Expected to Grow with a Fast Pace

Glass mat thermoplastic sheets were first introduced in 1970. Considering the cost-related mechanical performance criteria, GMT composites are located between injection moldable, discontinued (long or short) glass-fiber-reinforced composites, and advanced thermoplastic with various fiber architectures.

Although GMTs are available in various polymer matrices and are dominated by propylene-based composites due to their low price. These are well capable of competing with other structure materials, primarily in conditions where temperatures lesser than 110°C are maintained.

Glass mat thermoplastic composites are witnessing demand from the composite market. They are easy to use, with superior mechanical performance.

- Mercedes-Benz selected two grades of glass mat-reinforced thermoplastic material, which are supplied by the Swiss material producer Quadrant Plastic Composites. These materials are used for manufacturing the innovative front-end module, which was designed for its S-class series luxury coupe. The new front-end module weighs only 3.4 kg, while the previous model used to weigh 5 kg.

Innovations and greater market penetration are expected to drive the demand for glass mat thermoplastic composites during the forecast period.

Transportation Sector to Drive the Market

The Corporate Average Fuel Economy (CAFE) standard forced manufacturers in the automobile industry to develop vehicle designs that incorporated high-performance, lightweight materials. The weight of an automobile include a direct impact on driving dynamics, fuel consumption, and agility. A 10% reduction in vehicle weights results in approximately 5-7% rise in fuel savings.

The rising focus on minimizing carbon emissions and enhancement of fuel economy, primarily by reducing the weight of a vehicle, is driving the demand for thermoplastics composites.

Continuous fiber-reinforced thermoplastic composites (CFRTP) are one of the primary materials that can address the rising concerns regarding a vehicle's weight. In combination with metals, CFRTP composites will be a part of a multi-material approach when designing the car of the future. These materials are developed and assembled with recyclability and sustainability in mind. In addition, the automotive industry standards will serve to align methods for characterizing the performance of CFRTP composites.

The automotive industry is undergoing a major transformation. As companies explore various options to address future needs, collaboration proves to be an effective way to discover new growth avenues while leveraging risk. The preferred approach is collaboration with strategic players throughout the value chain.

- For instance, DuPont Transportation and Advanced Polymers choose to advance through collaborative networks while actively participating in consortia, including IACMI (Institute for Advanced Composites Manufacturing Innovation) and AZL (Aachen Centre for Integrative Lightweight Production. It is where standardization is addressed, along with collaborative teams that are focusing on demonstrating the production methods of cost-effective CFRTP composites, especially for high-volume applications.

Canada Automotive Thermoplastic Polymer Composites Industry Overview

The Automotive Thermoplastic Polymer Composites Market is consolidated, with only a few companies dominating the market. Some of the major players in the market are 3B-Fiberglass, Base Group, BASF, BMW, and Cytec Industries, Inc., amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasingly Focused On Lightweighting Vehicles

- 4.2 Market Restraints

- 4.2.1 High Production Cost

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD)

- 5.1 By Production Type

- 5.1.1 Hand Layup

- 5.1.2 Resin Transfer Molding

- 5.1.3 Vacuum Infusion Processing

- 5.1.4 Injection Molding

- 5.1.5 Compression Molding

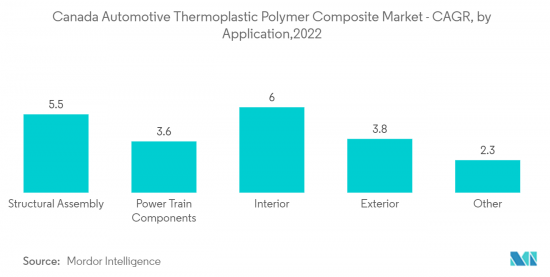

- 5.2 By Application Type

- 5.2.1 Structural Assembly

- 5.2.2 Power-train Components

- 5.2.3 Interior

- 5.2.4 Exterior

- 5.2.5 Other Application Types

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles

- 6.2.1 Solvay Group

- 6.2.2 3B-Fiberglass (Braj Binani Group)

- 6.2.3 Cytec Industries Inc.

- 6.2.4 Arkema Group

- 6.2.5 Celanese Corporation

- 6.2.6 Daicel Polymer Ltd

- 6.2.7 DuPont de Nemours

- 6.2.8 Hexcel Corporation

- 6.2.9 Technocompound GmbH

- 6.2.10 Polyone Corporation

- 6.2.11 Base Group

- 6.2.12 Gurit Holding

- 6.2.13 BASF SE

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Manufacturing Technologies

- 7.2 Development of Innovative Glass Fiber Composites