PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641944

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641944

Polyurethane Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

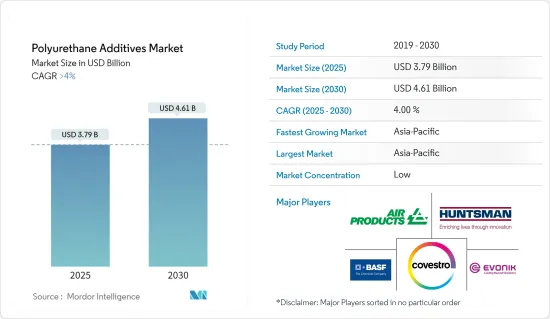

The Polyurethane Additives Market size is estimated at USD 3.79 billion in 2025, and is expected to reach USD 4.61 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

Key Highlights

- The rising demand for polyurethane in the construction industry will likely propel additives' consumption. One of the largest applications is the use of rigid PU foam as wall and roof insulation, insulated panels, and gap fillers for the space around doors and windows. Thereby augmenting the market's growth.

- On the flip side, the alternative additives can be used in some of the same applications as PU additives. For example, silicon additives and acrylic additives are both effective additives against PU foams.

- The increasing demand for more innovative and cost-effective additives is projected to act as an opportunity for the market in the future.

- The Asia-Pacific region is expected to account for the largest share and register the highest growth rate over the forecast period.

Polyurethane Additives Market Trends

Increasing Demand from the Automotive Industry

- The automotive industry provides one of the best examples of the diverse applications of PU materials. Nearly every type of PU product is used in the automotive end-user industry.

- Flexible PU foams are used in seating, headrests, armrests, HVAC, and other interior systems for automotive, like in airliners, trains, and buses. PU coatings provide a vehicle's exterior with high gloss, durability, scratch resistance, and corrosion resistance. PU coatings are also used for glazing windshields and windows, increasing strength and providing fog resistance.

- PU elastomers protect against tire punctures and are used in other molded components, such as shock absorbers. Thermoplastic PU materials are used to manufacture many automotive parts, including exterior body parts, trunk liners, anti-lock brake systems, timing belts, and fuel lines. The unique properties of PU elastomers contribute to their exclusive usage in gaskets, O-rings, and other seals.

- Seating is the largest application of PU in the automotive industry. Many automotive seating manufacturers demand products made with bio-based polyols. However, the market penetration of "green" PU is still emerging in most global PU markets.

- Globally, more than 90% of automobiles are produced with bonded windshields and rear windows using one-component PU sealants. The automotive industry is the largest end-user industry for reaction injection molding (RIM) PU parts. RIM is used to maximize the shock absorption of vehicle fenders, bumpers, and spoilers without adding weight or bulk.

- In 2022, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), around 85.02 million motor vehicles were produced worldwide. This figure translates into an increase of around 6% compared with the previous year. China, Japan, and Germany were the largest producers of cars and commercial vehicles in 2022, which is driving the PU additive market.

- However, with growing concerns about environmental pollution from petrol- and diesel-based vehicles, the production of electric vehicles is expected to pick up over the next five years. This is likely to drive the demand in the market studied over the forecast period.

- In August 2023, Global technology company Altair and the Center for Automotive Research (CAR), both based in Michigan, named Marelli as the 2023 Enlighten award winner in the Future of Lightweighting category for its polyurethane foam for interior products.

- Further, the global electric vehicle market is expanding significantly, which is benefitting the market studied. For instance, in 2022, around 10.5 million units of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold across the globe, witnessing a growth rate of 55% compared to 6.77 million units sold in the previous year.

- All the factors above are expected to drive the market during the forecast period.

China is Expected to Dominate the Asia-Pacific Region

- In Asia-Pacific, China is the largest economy in terms of GDP. The GDP value of China represents 7.73% of the world economy in 2022 and has a 3% GDP growth compared to the previous year.

- China is one of the largest countries in the world, where the construction sector dominates almost all other sectors in growth. In 2022, the construction industry accounted for around 6.9% of China's gross domestic product, and the value added to the Chinese construction industry increased by about 5.5% compared to the previous year.

- The rapid growth of the furniture manufacturing industry in the country is majorly fueled by the increasing domestic demand, coupled with significant demand from the foreign market.

- China accounted for almost 53% of the global furniture production in 2022. The production was further increased rapidly due to the increase in domestic demand and exports to European countries.

- According to the OICA, China remains the world's largest automotive manufacturing country and automotive market since 2009. Annual vehicle production in China accounted for more than 32% of worldwide vehicle production, which exceeds that of the European Union or that of the United States and Japan combined.

- However, the popularity of electric vehicles in the country is expected to propel the demand for PU additives in the coming years. The Chinese government plans to have a minimum of 5,000 fuel-cell electric vehicles by 2025 and 1 million by 2030. The government promoting the use of electric, hybrid, and fuel-cell electric vehicles is expected to drive the market studied during the forecast period.

- Such factors are expected to increase the demand for polyurethane additives in the country.

Polyurethane Additives Industry Overview

The polyurethane additives market is partially fragmented in nature. The major players (not in any particular order) include Evonik Industries AG, Air Products Inc., Covestro AG, Huntsman International LLC, and BASF SE. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Polyurethane in the Construction Industry

- 4.1.2 Increasing Demand from the Automotive Industry

- 4.1.3 Growing demand for sustainable Polyurethane products

- 4.2 Restraints

- 4.2.1 Availability of Alternative Additives

- 4.2.2 Stringent Government Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Blowing Agents

- 5.1.2 Catalysts

- 5.1.3 Flame Retardants

- 5.1.4 Surfactants

- 5.1.5 Other Additives( Filler, Emulsifiers, and Crosslinking Additives)

- 5.2 Application

- 5.2.1 Adhesives and Sealants

- 5.2.2 Coatings

- 5.2.3 Flexible Molded Foams

- 5.2.4 Rigid Foams

- 5.2.5 Other Applications (Elastomers, Fibers, Composites, and Medical Devices)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Products Inc.

- 6.4.2 Covestro AG

- 6.4.3 BASF SE

- 6.4.4 Dow

- 6.4.5 GEO Specialty Chemicals Inc.

- 6.4.6 Huntsman International LLC

- 6.4.7 Eastman Chemical Company

- 6.4.8 Evonik Industries AG

- 6.4.9 Momentive Performance Materials Inc.

- 6.4.10 KAO Corporation

- 6.4.11 Specialty Products Inc.

- 6.4.12 Tosoh Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for More Innovative and Cost-effective Additives

- 7.2 Other Opportunities