PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850999

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850999

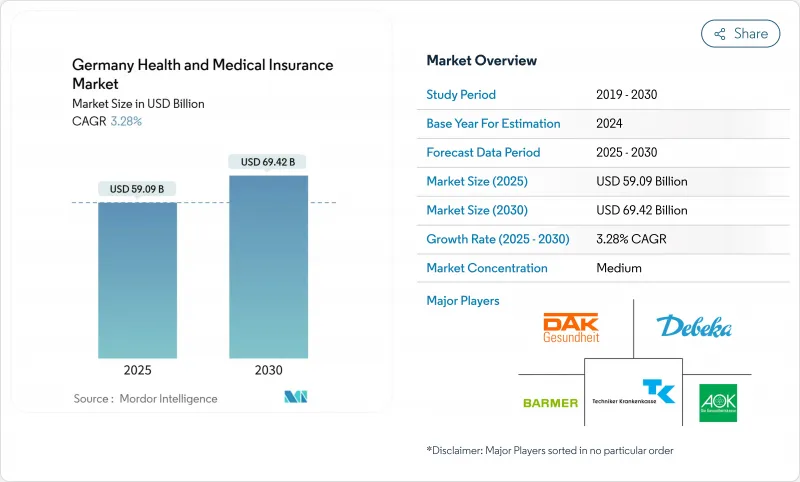

Germany Health And Medical Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Germany health and medical insurance market reached USD 59.09 billion in 2025 and is projected to rise to USD 69.42 billion by 2030, with a steady 3.28% CAGR.

Rising life expectancy, a chronic disease burden that is among Europe's heaviest, and a regulatory commitment to universal coverage give the market a resilient baseline even as statutory insurers wrestle with deficits. Contribution-rate hikes inside the statutory system are nudging many high-income workers toward supplemental private cover, while the nationwide electronic patient record (ePA) rollout is accelerating end-to-end digitalization that trims reimbursement lags and administrative waste. Corporate group plans remain the backbone of the Germany health and medical insurance market, underwriting 72% of total contracts, and direct digital channels, though still smaller than tied-agent sales, are compounding at an 8.97% CAGR as younger adults opt for app-based onboarding. Regional dynamics add another layer: Westdeutschland commands the largest premium pool, yet Ostdeutschland posts the highest growth rate, aided by telemedicine that bridges physician shortages. Private insurers leverage this digital momentum to bundle virtual consults and disease-management modules, while statutory funds emphasize preventive programs that can flatten future cost curves.

Germany Health And Medical Insurance Market Trends and Insights

Aging Population & Chronic-Disease Prevalence

Germany's over-65 cohort is projected to approach one-third of residents by 2050, a demographic shift that enlarges insurance risk pools and amplifies the demand for geriatric and chronic-care benefits. Healthcare outlays already exceed USD 6,414 per person, the European Union's peak level, and chronic illnesses such as diabetes and coronary disease dominate hospital days. Actuaries respond by refining age-band pricing, while carriers roll out prevention platforms that link wearable data to premium discounts. Digital nursing services, reimbursed under new telecare tariffs, help soften workforce shortages in eldercare facilities. Taken together, population aging remains the primary structural engine of the Germany health and medical insurance market.

Escalating Statutory Contribution Rates Driving Supplemental Cover

Statutory spending rose 6.8% in 2025 against only 3.7% revenue growth, lifting the average additional GKV contribution to 2.5%. High earners now face monthly deductions of USD 651.91 at a contribution ceiling of USD 71,442, prompting many to seek private dental, alternative treatment, or private ward upgrades. Carriers market modular riders that plug GKV gaps without forcing full departure from the statutory pool, an approach resonating with professionals who value continuity of coverage yet want premium amenities. This arbitrage mechanism accelerates premium inflows to the private side of the Germany health and medical insurance market.

Structural GKV Deficit & Political Price Pressure

Germany's reserve buffers have dipped beneath the mandated threshold of USD 5.18 billion. It has ignited discussions around imposing an expenditure moratorium and seeking increased federal transfers to stabilize the system. While policymakers are hesitant to raise contributions further, fearing added strain on payroll costs and potential economic repercussions, insurers find their pricing flexibility significantly curtailed. Such constraints hinder the swift adoption of costly digital upgrades, which are essential for modernizing operations, improving efficiency, and dampening short-term profitability for insurers in Germany's health and medical sector. The ongoing structural GKV deficit and political price pressures are expected to continue influencing market dynamics in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Digital-Health & ePA Roll-Out Accelerating Insurer Innovation

- Rising Per-Capita Health-Expenditure Outlay

- Premium Inflation in PKV Dampening New Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Statutory health insurance maintained 85.1% control of the Germany health and medical insurance market in 2024, anchored by universal access and employer cost-sharing. The Germany health and medical insurance market size grows as GKV funds leverage scale to embed ePA services, but their deficits intensify. 82 of 93 funds raised contribution rates for 2025, signaling a pivot to non-price differentiation, such as wellness apps and rapid reimbursement.

Private carriers, post the quickest 4.67% CAGR to 2030 by targeting high-income consumers with concierge benefits and guaranteed specialist access. The consolidation strengthens that play: BaFin cleared the Gothaer-Barmenia merger valued at over USD 7.56 billion, creating the sixth-largest private insurer. The integrated entity can negotiate hospital tariffs more forcefully and spread IT costs over a larger base, reshaping competitive architectures within the Germany health and medical insurance market.

In 2024, long-duration policies dominated the Germany health and medical insurance market, making up 90.2% of its size. This trend mirrors the country's tradition of lifetime statutory entitlements and a strong culture of stable employment. Insurers are now linking loyalty bonuses to wellness targets, providing premium rebates for gym visits, which are conveniently tracked through app QR codes. Its heightened engagement incentivizes healthier habits and also enriches underwriting data, leading to better forecasts for chronic diseases. Additionally, the integration of wellness programs into insurance offerings reflects a broader shift toward preventive healthcare, aiming to reduce long-term costs for both insurers and policyholders.

While short-term expat plans currently hold a smaller share, they are projected to grow at an annual rate of 6.38%. This surge is largely fueled by the influx of foreign students, gig workers, and employees on temporary postings. Digital brokers are streamlining services by integrating visa letters, tele-doctor consultations, and multilingual claims assistance into a single smartphone platform. These innovations enhance customer convenience and accessibility, making such plans more attractive to a diverse and mobile population. Such strategic maneuvers diversify revenue streams and provide a buffer for carriers, shielding them from demographic saturation in Germany's core health and medical insurance segments. Furthermore, the growing demand for short-term plans highlights the evolving needs of an increasingly globalized workforce, prompting insurers to adapt their offerings to remain competitive in this dynamic market.

The Germany Health and Medical Insurance Market is Segmented by Product Type (Statutory Health and Private Health Insurance), Term of Coverage (Short-Term and Long-Term), Distribution Channel (Single-Tied, Direct Selling, Credit Institutions, and More), End-User (Corporate/Employer, Individual/Families, and More), and Region. The Market Forecasts are Provided in Value (USD).

List of Companies Covered in this Report:

- Techniker Krankenkasse (TK)

- AOK - Die Gesundheitskasse

- Barmer

- DAK-Gesundheit

- Debeka

- Allianz

- AXA

- Gothaer Group

- DKV

- Signal Iduna

- HanseMerkur

- Continentale

- Ergo Direkt

- Cigna

- Aetna

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing population & chronic-disease prevalence

- 4.2.2 Escalating statutory contribution rates driving supplemental cover

- 4.2.3 Digital-health & ePA roll-out accelerating insurer innovation

- 4.2.4 Rising per-capita health-expenditure outlay

- 4.2.5 Expansion of employer-sponsored group PHI plans

- 4.2.6 InsurTech MGA cost-disruption lowering admin expense

- 4.3 Market Restraints

- 4.3.1 Structural GKV deficit & political price pressure

- 4.3.2 Premium inflation in PKV dampening new uptake

- 4.3.3 Prospect of "Burgerversicherung" single-payer reform

- 4.3.4 Intermediary talent shortage inflating acquisition cost

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Statutory vs Private Preference Analysis

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value)

- 5.1.1 Statutory Health Insurance (GKV)

- 5.1.2 Private Health Insurance (PKV)

- 5.2 By Term of Coverage (Value)

- 5.2.1 Short-term

- 5.2.2 Long-term

- 5.3 By Distribution Channel (Value)

- 5.3.1 Single-tied / Insurance-group Intermediaries

- 5.3.2 Broker & Multiple Agents

- 5.3.3 Credit Institutions

- 5.3.4 Direct Selling

- 5.3.5 Other Channels

- 5.4 By End-User/Customer Type

- 5.4.1 Corporate/Employer (Group Plans)

- 5.4.2 Individual/Families

- 5.4.3 SME's (Small & Medium-sized Enterprises)

- 5.4.4 Others

- 5.5 By Region

- 5.5.1 Norddeutschland

- 5.5.2 Ostdeutschland

- 5.5.3 Westdeutschland

- 5.5.4 Suddeutschland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Techniker Krankenkasse (TK)

- 6.4.2 AOK - Die Gesundheitskasse

- 6.4.3 Barmer

- 6.4.4 DAK-Gesundheit

- 6.4.5 Debeka

- 6.4.6 Allianz

- 6.4.7 AXA

- 6.4.8 Gothaer Group

- 6.4.9 DKV

- 6.4.10 Signal Iduna

- 6.4.11 HanseMerkur

- 6.4.12 Continentale

- 6.4.13 Ergo Direkt

- 6.4.14 Cigna

- 6.4.15 Aetna

7 Market Opportunities & Future Outlook

- 7.1 Die BMW BKK

- 7.1.1 TK Auxiliary InsurTech Envivas

- 7.1.2 HUK-COBURG Krankenversicherung

- 7.1.3 Munchener Verein