PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851094

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851094

Fixed Wireless Access - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

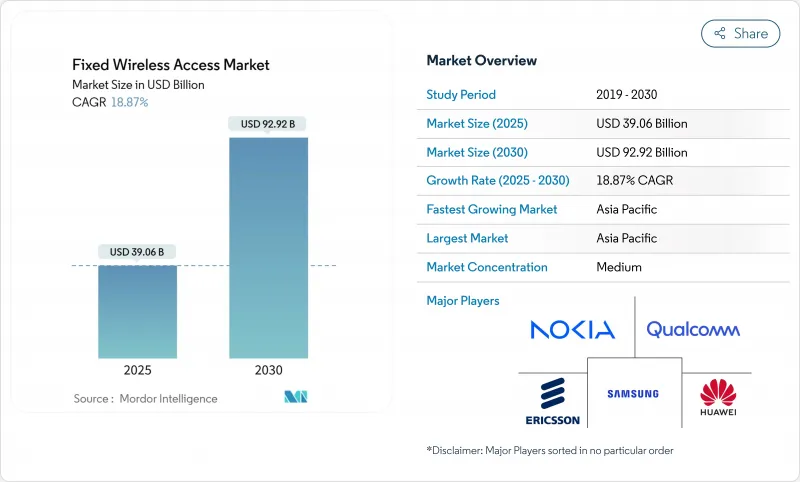

The fixed wireless access market is valued at USD 39.06 billion in 2025 and is forecast to reach USD 92.72 billion by 2030, reflecting an 18.87% CAGR and confirming the fixed wireless access market size as one of the most rapidly expanding broadband segments.

Expansion rests on three pillars: accelerated 5G roll-outs that repurpose existing mobile towers for home broadband, growing demand for affordable last-mile connectivity in rural districts, and continuous innovation in customer-premises equipment that delivers near-fiber speeds. Operators in North America and Asia Pacific have redirected capital from traditional fiber-to-the-home toward fixed wireless, trimming deployment timelines and reducing per-household costs by wide margins. Spectrum allocations in Sub-6 GHz, coupled with millimeter-wave launches in dense urban zones, give providers the flexibility to balance coverage and capacity. Meanwhile, industrial IoT pilots are turning fixed wireless access links into secure, low-latency backbones for factories and logistics hubs, thereby opening fresh revenue streams.

Global Fixed Wireless Access Market Trends and Insights

5G Roll-out Accelerating Gigabit-class FWA

Widespread 5G deployment allows operators to layer fixed wireless access on the same radio network, turning mobile macro sites into neighborhood broadband nodes. U.S. carriers report the majority of net broadband additions coming from fixed wireless packages, underscoring how the fixed wireless access market is eating into cable's traditional base. Investments in massive MIMO and beamforming raise outdoor CPE throughput while sustaining service in non-line-of-sight environments. Ericsson software upgrades extend usable range without new hardware, simplifying rural coverage. Vendors such as Nokia have showcased mmWave receivers that hold a 1 Gbps link at distances up to 7 km, proving viability in both dense cities and sparsely populated fringes. Taken together, these advances lift customer experience to fiber-like benchmarks and boost adoption across homes and enterprises.

Rural Broadband Stimulus Programmes

Public funding is narrowing digital divides by underwriting radio access equipment and CPE for towns bypassed by fiber trenching. In the United States, federal and state grants funnel billions into unserved census blocks, and fixed wireless access often receives priority because towers are deployed in weeks rather than months. Washington State regulators confirm that FWA solutions can be installed rapidly at lower cost, albeit with modest speed trade-offs compared with fiber. Europe's Digital Decade agenda mirrors this approach through flexible spectrum rules that invite wireless internet service providers into rural bands. Cost-benefit studies from The Brattle Group link broadband expansion, including fixed wireless, to trillions in property-value and income gains, fueling more policy support.

Spectrum Scarcity & Regulatory Uncertainty

Mid-band spectrum sits at the sweet spot between coverage and capacity, yet much of it is tied up in legacy use or contested by incumbent broadcasters. Lobbying battles over the lower 3 GHz block in the U.S. illustrate how protracted policymaking can stall operator investment. Dynamic sharing systems such as Google's Spectrum Access System allow opportunistic use, but device ecosystems still rely on clear, licensed holdings. Varied regional rules complicate global equipment design, raising costs and slowing volume manufacturing. Although national road maps, including the NTIA National Spectrum Strategy, promise additional allocations, uncertainty lingers through auction delays and shifting priorities.

Other drivers and restraints analyzed in the detailed report include:

- FWA as Cost-effective Last-mile Alternative to Fibre

- Enterprise SD-WAN Back-up Connectivity Demand

- High mmWave Densification CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained a 65% share of the fixed wireless access market in 2024 thanks to intensive early-stage spending on radios and CPE that anchor network roll-outs. Indoor devices make up 60% of units shipped, while outdoor models dominate revenue because of higher unit pricing and professional installation. Operators and vendors continue to innovate on thermals, antenna gains, and router software, giving customers a self-install experience that parallels Wi-Fi mesh kits. The fixed wireless access market size attributable to hardware is projected to expand, yet at a slower clip than subscriptions.

The services segment is set for a 19.60% CAGR through 2030, outstripping the rest of the fixed wireless access industry as providers diversify into managed Wi-Fi, over-the-top video, and cloud security bundles. More than 40% of operators have migrated to speed-based tariff menus that mimic fiber grade tiers, accelerating average revenue per user. Network APIs will soon enable on-demand throughput boosts during live events or e-sports tournaments, further lifting service margins. As adoption reaches scale, recurring fees rather than equipment sales will define earnings power.

Residential broadband accounted for 52% of overall revenue in 2024, reflecting aggressive consumer campaigns by Tier-1 mobile carriers. Promotions often bundle streaming subscriptions and zero-cost hardware, which compresses churn. Industrial deployments, in contrast, record a 22.32% CAGR to 2030. Factories insert fixed wireless gateways between production lines and edge servers, supporting real-time machine vision, robotics, and safety systems. Trials have demonstrated a median downlink of 648 Mbps and peaks above 1 Gbps using carrier-aggregated spectrum. These metrics satisfy stringent availability targets common in automotive and semiconductor plants.

Commercial sites such as quick-service restaurants rely on fast turn-ups and flexible contracts to connect point-of-sale systems and digital signage. Education and healthcare settings also favor rapid deployment over trenching permits. Consequently, fixed wireless access market players tailor vertical packages that integrate private 5 G cores with zero-touch provisioning.

The Fixed Wireless Access Market Report is Segmented by Type (Hardware [Consumer Premise Equipment (CPE), Access Units [Femto and Picocells]] and Services), Application (Residential, Commercial, and Industrial), Frequency Band (Sub-6 GHz and MmWave (above 24 GHz), Deployment Mode (Outdoor CPE and Indoor CPE), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific keeps a 37% revenue share and posts the fastest 21.07% CAGR as 5 G population coverage exceeds 85% in China, South Korea, and Japan. India's top two operators have bundled AirFiber services with pay-per-day vouchers, capturing millions of first-time broadband users in less than a year. Government incentives under Digital India reimburse up to 80% of tower equipment in unserved villages, further accelerating roll-out. Fixed wireless access market players also benefit from device-manufacturing hubs across the region that shorten supply chains.

North America follows, fueled by large-scale 5 G standalone cores and supportive spectrum policy. The fixed wireless access market size in the United States is climbing as telecoms redeploy mid-band holdings cleared from satellite services. Operators routinely report 600,000 to 700,000 net additions per quarter, a trend that has forced cable incumbents to introduce symmetrical tiers. Canada's rural broadband drive funds rooftop radios for farms and tourist lodges where fiber trenching through permafrost is impractical.

Europe shows a fragmented pattern. Northern nations with high fiber coverage use fixed wireless mainly for redundancy, while Southern and Eastern countries leverage it to leapfrog copper upgrades. Regulatory flexibility in the 26 GHz band encourages cross-border equipment harmonization, which lowers CPE cost. Emerging markets in the Middle East and Africa rely on wireless first solutions for last-mile access. National broadband plans treat fixed wireless as the primary method to connect schools and clinics within two years, positioning the fixed wireless access market as a catalyst for digital inclusion across the continent.

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Ericsson AB

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Verizon Communications Inc.

- ATandT Inc.

- T-Mobile US Inc.

- US Cellular Corp.

- Airspan Networks Inc.

- Siklu Communication Ltd.

- Starry Group Holdings Inc.

- Arqiva Ltd.

- Inseego Corp.

- ZTE Corporation

- Deutsche Telekom AG

- Vodafone Group Plc

- Telstra Corp. Ltd.

- Orange S.A.

- Globe Telecom Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G roll-out accelerating gigabit-class FWA

- 4.2.2 Rural broadband stimulus programmes

- 4.2.3 FWA as cost-effective last-mile alternative to fibre

- 4.2.4 Enterprise SD-WAN back-up connectivity demand

- 4.3 Market Restraints

- 4.3.1 Spectrum scarcity and regulatory uncertainty

- 4.3.2 High mmWave densification CAPEX

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Key enablers for FWA adoption

- 4.6.2 Vendor initiatives and partnerships

- 4.6.3 Business considerations and prerequisites

- 4.6.4 FWA vs FTTH / FTTdp comparison

- 4.6.5 Rural, semi-urban and urban use-case models

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.1.1 Consumer Premise Equipment (CPE)

- 5.1.1.2 Access Units (Femto and Picocells)

- 5.1.2 Services

- 5.1.1 Hardware

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.3 By Frequency Band

- 5.3.1 Sub-6 GHz

- 5.3.2 mmWave ( above 24 GHz)

- 5.4 By Deployment Mode

- 5.4.1 Indoor CPE

- 5.4.2 Outdoor CPE

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia-Pacific

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Technologies Co. Ltd.

- 6.4.2 Nokia Corporation

- 6.4.3 Ericsson AB

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Verizon Communications Inc.

- 6.4.7 ATandT Inc.

- 6.4.8 T-Mobile US Inc.

- 6.4.9 US Cellular Corp.

- 6.4.10 Airspan Networks Inc.

- 6.4.11 Siklu Communication Ltd.

- 6.4.12 Starry Group Holdings Inc.

- 6.4.13 Arqiva Ltd.

- 6.4.14 Inseego Corp.

- 6.4.15 ZTE Corporation

- 6.4.16 Deutsche Telekom AG

- 6.4.17 Vodafone Group Plc

- 6.4.18 Telstra Corp. Ltd.

- 6.4.19 Orange S.A.

- 6.4.20 Globe Telecom Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment