PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406025

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406025

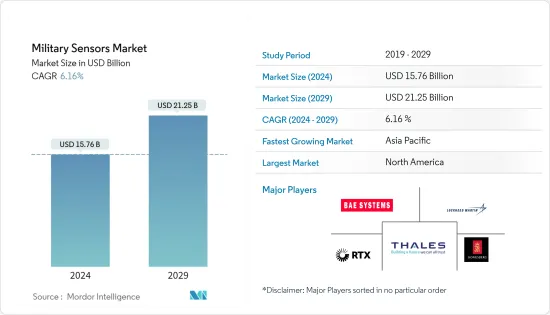

Military Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Military Sensors Market size is estimated at USD 15.76 billion in 2024, and is expected to reach USD 21.25 billion by 2029, growing at a CAGR of 6.16% during the forecast period (2024-2029).

The evolution and rapid adoption of microelectromechanical systems (MEMS)-based devices have led to the development of sophisticated micro gyros for navigation and positioning, microbolometers for infrared imaging, and micromirrors for steering laser beams. RF MEMS and nanotechnology could lead to breakthroughs in aerospace and defense applications, such as satellite communications at speeds in excess of 100 GHz and electronically steerable RF phase shifters for true-time delay.

Modern military systems are heavily reliant on complex software and interconnectivity to perform their missions. Advanced features, such as an electronic attack, sensor fusion, and communications, of the cyber-enabled military systems provide a tactical edge to the equipped armed forces against an adversary force or during critical operations in a hostile environment. Factors such as increasing demand for battlespace awareness amongst defense forces, ongoing advancements in MEMS technology, and integration of anti-jamming capabilities with navigation systems will be driving the growth of the market. However, cybersecurity risks, complexity in the designs of military sensors, and lack of accuracy would be constraining the growth of the market.

Military Sensors Market Trends

Airborne Segment Expected to Register the Highest CAGR During the Forecast Period

Modern military planes are made to do different kinds of missions. An increase in the global aerial fleet has led to a rise in the demand for military sensors in airborne segments. Countries like the United States, India, China, Iran, Israel, and Russia, among others, have invested in modernizing and upgrading their existing air fleets. China is using stealth technology in unmanned platforms and is unveiling more UAV variants. Furthermore, rising global expenditure and rising spending on enhancing defense capabilities drive market growth.

Moreover, the cost-effectiveness and ease of operations of unmanned platforms, compared to manned platforms, aided the rapid adoption of UAVs in defense applications (for both surveillance and attack operations). Military organizations are also largely deploying unmanned platforms in conflict regions across the world. Also instances such as in September 2022, the US Army awarded phase two contracts to defense firms Raytheon and L3Harris for the development of prototype sensors that were to support the service's next-gen airborne intelligence, surveillance, and reconnaissance program dubbed HADES. These factors render a positive outlook for the airborne military sensors segment of the market during the forecast period.

Asia-Pacific is Expected to Generate the Highest Demand During the Forecast Period

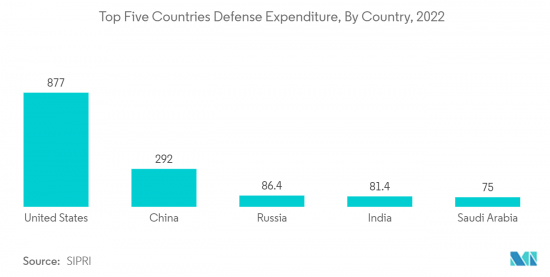

The Asia-Pacific region is expected to generate the highest demand for military sensors on account of the several ongoing programs fostering the modernization of the regional defense forces during the forecast period. In the Asia-Pacific, several modernization programs are underway to enhance the current capabilities of the commercial and military end-users in the region. For instance, Indonesia's Defence Ministry sealed a deal with Turkey to acquire 12 cutting-edge drones valued at USD 300 million, marking yet another step in the country's ongoing efforts to modernize its aging military equipment. In terms of operational fleet, the region has the largest fleet of aircraft and rotorcraft, with 14,529 aircraft. Out of these, combat aircraft constitute about 4,998, along with 520 special purpose aircraft, 46 tankers, 1,008 transport, and 3,079 training and helicopters. The increasing geopolitical tensions between neighboring nations and the rising demand for advanced threat detection systems are expected to aid the growth of the market in this region.

Military Sensors Industry Overview

The military sensors market is semi-consolidated and marked by the presence of many prominent players competing for a larger market share. The prominent players in the military sensors market are RTX Corporation, Lockheed Martin Corporation, Kongsberg Gruppen ASA, BAE Systems plc, and THALES. Vendors are modifying their offerings to enhance current capabilities and introduce revolutionary features as a means to deliver value-added sensor solutions to end users. This helps introduce low-differentiated products at competitive pricing. Furthermore, strategic collaboration between manufacturers is on the rise to develop sophisticated sensors that conform with the design and performance specifications of the end-user defense forces. This is expected to benefit industry stakeholders during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.1.2 Communication and Navigation

- 5.1.3 Target Recognition

- 5.1.4 Electronic Warfare

- 5.1.5 Command and Control

- 5.2 Platform

- 5.2.1 Airborne

- 5.2.2 Terrestrial

- 5.2.3 Naval

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Germany

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 TE Connectivity Ltd.

- 6.2.3 RTX Corporation

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 THALES

- 6.2.6 Kongsberg Gruppen ASA

- 6.2.7 Ultra

- 6.2.8 Aerosonic LLC (Transdigm Group)

- 6.2.9 General Electric Company

- 6.2.10 BAE Systems plc

- 6.2.11 Vectornav Technologies LLC

- 6.2.12 Viooa Imaging Technology Inc.

- 6.2.13 Imperx Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS