PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689924

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689924

Compound Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

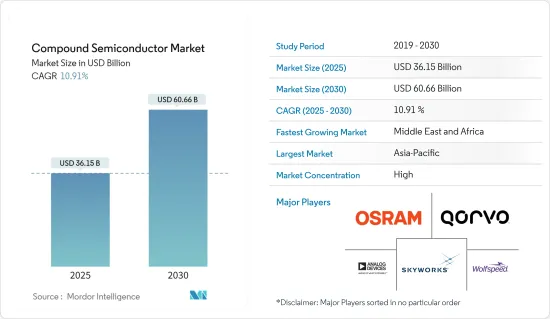

The Compound Semiconductor Market size is estimated at USD 36.15 billion in 2025, and is expected to reach USD 60.66 billion by 2030, at a CAGR of 10.91% during the forecast period (2025-2030).

The COVID-19 pandemic halted the manufacturing of several products in the compound semiconductor production industry owing to continued lockdown in critical global regions. In addition, country-wise lockdowns inflicted by governments across the globe further resulted in sectors taking a hit and disrupting supply chains and manufacturing operations worldwide. Most manufacturing operations, including the factory floor work, were significantly affected, resulting in decreased productivity.

Key Highlights

- Compound semiconductors are made from two or more elements of the different or same group of the periodic table. These are manufactured by using various types of deposition techniques, such as chemical vapor deposition, atomic layer deposition, and others. They possess unique properties like high temperature and heat resistance, enhanced frequency, high sensitivity to magnetism, and faster operation and optoelectronic features are some of the key advantages boosting their demand. Moreover, the decrease in the manufacturing cost of compound semiconductors has increased their application in electronic and mobile devices.

- The ability of compound semiconductors to emit and sense light in the form of general lighting (LEDs) and lasers and receivers for fiber optics is further driving the demand. The decrease in manufacturing and installation cost of LEDs has increased its application in lamps and fixtures across all sectors. Mega-cities concentrate on investing in infrastructure development to meet the needs of the growing population, and governments are helping customers to install energy-efficient lighting sources to reduce their electricity consumption costs.

- For instance, during the pandemic, EESL (Energy Efficiency Services Limited) celebrated the completion of its one-year governmental project called the Unnat Jyoti Program (UJALA). Under this program, it substituted more than 10.6 million street light bulbs with LED lights to reduce the carbon dioxide footprint by 20 million tons and the electricity cost. Such initiatives further boost the market studied.

- In 2020, the Taiwan Semiconductor Manufacturing Company (TSMC) sourced about 31% of spare parts locally in China, which increased to 31% in 2021.

- According to the US Department of Energy (DOE), LED lights use about 75-80% less energy than traditional incandescent light bulbs and about 65% less energy than halogen bulbs. Commercial enterprises need lighting for an extended period, whether for long working hours, safety and security in a warehouse or manufacturing facility, or other uses. Thus, switching to LED lights can save millions of dollars annually. For example, US Energy Recovery clients can save about 20-55% on their electric utility bills by swapping out old lighting systems for state-of-the-art LED lighting. Therefore, the shift toward LED adoption is driving the growth of the market studied.

- The smartphone is the major consumer of compound semiconductors. The smartphone market has been very competitive in recent years. The increasing usage of mobile phones is further anticipated to drive the global market. For instance, according to the Ericsson Mobility Report, 2022, by the end of 2027, there will be 4.4 billion 5G subscriptions globally, accounting for 48% of all mobile subscriptions.

- The Internet of Things applications are increasing, which is expected to boost the sales of compound semiconductors. Moreover, the wireless communications sector is expected to grow with the growth in 5G networks. Fifth-generation networks also indicate the likelihood of consumers upgrading their mobile handsets or devices to drive global compound semiconductor adoption.

- The compound semiconductor industry is considered one of the most complex industries, not only due to the more than 500 processing steps involved in the manufacturing and various products but also due to the harsh environment it faces, e.g., the volatile electronic market and the unpredictable demand.

Compound Semiconductor Market Trends

Optoelectronics to Have a Significant Growth During the Forecast Period

- Optoelectronic products covered under the study scope include photodiodes, phototransistors, optical spectrum analyzers, solar panels, and other optoelectronic devices, excluding LED products.

- GaN-based transistors are discovering new ways, particularly in optoelectronics, compared to SiC-based, as they are faster and more efficient. GaN has 1,000 times the electron mobility of silicon, along with relatively stable operability at higher temperatures.

- Recent advancements in the field of optoelectronics, such as plasmonic nanostructures, perovskite transistors, optically active quantum dots, microscopic light bulbs, low-cost 3D imaging, laser-powered 3D display technology, and Laser Li-Fi, are expected to cause a quantum shift in the dynamic applicability areas of optoelectronic apparatus.

- Further, in June 2022, a multiwavelength optoelectronic synapse that enables optical data detection, storage, and processing in the same device was created by researchers in the United States (University of Central Florida) and South Korea. The resultant in-sensor artificial visual system, which significantly improves processing effectiveness and picture identification precision, might use robotics, self-driving cars, and machine vision. Like the human eye, where the retina, through the synapse of the optic nerve, carries optical data, optoelectronic synapse allows optical data sensing, memory, and processing to be integrated into the same device.

- Additionally, in August 2022, Yokogawa launched two new optical spectrum analyzers (OSAs) to fulfill the market demand for an instrument capable of measuring a wide range of wavelengths to meet unique optical product expansion and manufacturing needs. The Yokogawa AQ6375E and AQ6376E are the only grating-based OSAs covering SWIR (Short-Wavelength InfraRed) over 2 μm and MWIR (Mid-Wavelength InfraRed) over 3 μm, with advanced optical performance.

- To meet the various needs of the customers, the firms are expanding their product portfolio. For instance, in April 2022, the Everlight line specializes in manufacturing different optoelectronic devices, introduced a wide range of new products in its portfolio, including photodiodes and phototransistors. These products are offered by third-distributor Transfer Multisort Elektronik (TME).

- Growing demands for renewable energy are further driving the studied Market. According to IRENA, the solar photovoltaic energy capability in the South Asian country of India peaked at over 62.8 gigawatts in 2022, up 21.5% from the previous year.

Middle East and Africa to Witness Significant Growth

- Prominent countries across the Middle East and Africa, such as Saudi Arabia, Egypt, and the United Arab Emirates, have some of the region's most extensive renewable energy programs. Compound semiconductor devices play a significant role in controlling the generation and link to the network of renewable energy sources.

- Moreover, the semiconductor industry is slowly gaining momentum in the Middle East and Africa, creating considerable market growth opportunities. For instance, in March 2022, the King AbdulazizCity for Science and Technology (KACST) announced the launch of the Saudi Semiconductor Program, the first of its kind in the province, which is desired to support the research, development, and qualification of professionals in the field of designing and localizing electronic chips.

- Furthermore, in the Middle East & North Africa, 5G is expanding significantly. The Gulf nations have taken the lead in developing 5G, and their governments and authorities have given mobile carriers access to the 5G launch spectrum so they may build some of the world's first and fastest 5G networks. According to GSMA, the diversified economies of the Middle East and North Africa (MENA) will significantly benefit from 5G, with the mid-band estimated to provide USD16 billion more in new GDP in 2030, or 0.35% of the region's GDP.

- In addition, in March 2022, MTN, a multinational mobile telecommunications firm based in South Africa, said it would invest more than USD 42.25 million in network development and a 5G push in the nation's largest province, the Northern Cape, and its judicial center, the Free State. Such initiatives to boost the overall semiconductor industry in these regions create a positive outlook for the growth of the studied market.

- Further, Dubai is expected to spend millions of Dirhams on incentives to have 42,000 EVs on its streets by 2030. General Motors expects to boost sales in the Middle East & Africa with the launch of its Chevrolet EV. The number of EV Green Charger stations in Dubai may be doubled as part of the 'Smart Dubai' initiative, which seeks to make Dubai the world's most innovative and happiest city. The Dubai Electricity and Water Authority announced the fulfillment of the second phase of its 'Green Charger' ambition, which contained the installation of additional 100 EV Green Charger stations across Dubai.

- According to the Climate Reality Project, the world's most extensive concentrated solar plant is due to be completed recently near Dubai, and it is expected to have a capacity of 1,000 MW. Dubai aims to produce 75% of its energy from clean sources by 2050, and its target energy mix for 2030 is 25% solar. These initiatives are driving the studied market in the region.

Compound Semiconductor Industry Overview

The Compound Semiconductor Market is highly competitive and is dominated by several major players like Broadcom, Skyworks Solutions, Cree, Qorvo, Analog Devices, OSRAM, GaN Systems, Skyworks Solution, and Infineon Technologies. These prominent players with a significant market share focus on extending their customer base across foreign nations. These companies leverage strategic cooperative initiatives to increase their market share and profitability. However, with technological advancements and product innovations, mid-size to smaller companies are growing their market by securing unique contracts and tapping new markets.

- June 2022 - ams OSRAM announced that Taiwan-based Ledtech had chosen OSLON UV 3636 UV-C LEDs for a sanitization function in its newBioLED intelligent air purifier. The BioLED's OSLON UV 3636 LEDs can inactivate up to 99.99% of viruses, including SARS-CoV-2, at a dosing rate of 3.6mJ/cm2.

- May 2022 - Qorvo introduced a new generation of 1200V SiCFETs. The new UF4C/SC series of 1200V Gen 4 SiCFETs (from recently acquired UnitedSiC) are designed for 800V bus architectures in onboard chargers for electric vehicles, industrial battery chargers, industrial power supplies, DC/DC solar inverters, welding machines, uninterruptible power supplies, and induction heating applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Electronic and Mobile Devices

- 5.1.2 Increase in Industrial Automation

- 5.2 Market Challenges

- 5.2.1 High Raw Material and Fabrication Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Gallium Arsenide (GaAs)

- 6.1.2 Gallium Nitride (GaN)

- 6.1.3 Gallium Phosphide (GaP)

- 6.1.4 Silicon Carbide (SiC)

- 6.1.5 Others

- 6.2 By Product

- 6.2.1 LED

- 6.2.2 RF

- 6.2.3 Optoelectronics

- 6.2.4 Power Electronics

- 6.2.5 Other Products

- 6.3 By Application

- 6.3.1 Telecommunications

- 6.3.2 Information & Communication Technology

- 6.3.3 Defense & Aerospace

- 6.3.4 Consumer Electronics

- 6.3.5 Healthcare

- 6.3.6 Automotive

- 6.3.7 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 France

- 6.4.2.3 Italy

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of the Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Skyworks Solutions INC.

- 7.1.2 Wolfspeed Inc.

- 7.1.3 Qorvo Inc.

- 7.1.4 Analog Devices Inc.

- 7.1.5 OSRAM GmbH (ams-OSRAM AG)

- 7.1.6 GaN Systems Inc.

- 7.1.7 Infineon Technologies AG

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Advanced Wireless Semiconductor Company

- 7.1.10 STMicroelectronics N.V.

- 7.1.11 Texas Instruments Inc.

- 7.1.12 Microsemi Corporation (Microchip Technology Inc.)

- 7.1.13 WIN Semiconductors Corp.

- 7.1.14 ON Semiconductor Corp. (Semiconductor Components Industries Llc)

- 7.1.15 Mitsubishi Electric Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET