PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406181

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406181

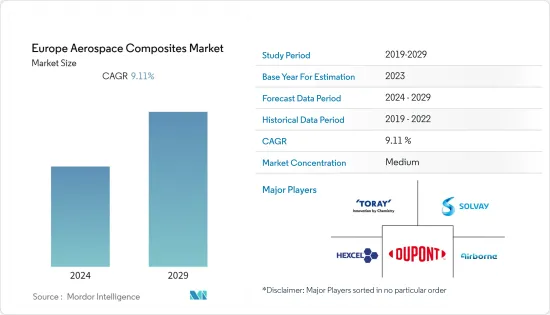

Europe Aerospace Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Europe Aerospace Composites Market size is expected to grow from USD 5.53 billion in 2024 to USD 8.57 billion by 2029, registering a CAGR of 9.11% during the forecast period.

The characteristics of composites, like temperature and chemical resistance, lightweight, high stiffness, dimensional stability, and flex performance, among others, made their use popular in various aerospace components and structural applications. Reduced maintenance and longer design life, fewer parts, and reduced tooling and assembly costs are some of the reasons that drive the composites market in the aerospace industry. The increasing investments in the research and development (R&D) of advanced composite materials by several aerospace incumbents, like the General Electric Company, the Boeing Company, and Airbus SE, among others, are also supporting the growth of the Europe aerospace composites market.

Europe Aerospace Composites Market Trends

Commercial Aviation Segment to Continue its Dominance During the Forecast Period

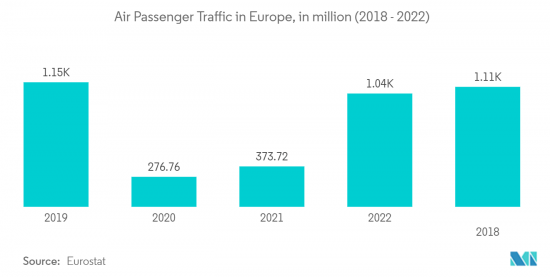

Air passenger traffic in Europe witnessed steady growth during the last decade. According to ACI, passenger traffic across the European airport network nearly doubled (+98%) in 2022 compared to the previous year, reaching 1.94 billion passengers. However, that was still -21% below pre-pandemic (2019) volumes, with just 27% of Europe's airports fully recovering their 2019 passenger traffic level. The rise in passenger traffic signifies a parallel demand for new aircraft from airline operators to effectively serve more passengers and gain market share. The new generation aircraft features extensive use of composites due to their inherent cost and weight savings benefits over traditional airframe materials such as metal alloys. For instance, while the A380 features around 30% carbon fiber reinforced polymer (CFRP) in its airframe and component layout, CFRPs constitute around 53% of the same in the A350XWB. The increase in the CFRP composition enabled designers to ensure weight savings of over 10 tons in the A350XWB as compared to the A330. Since a weight saving of 100 kg is attributed to a potential cost saving of 10,000 l of gasoline per year for an aircraft operator, the use of composites in the OEM design of commercial aircraft is envisioned to grow during the forecast period. The order books of commercial aircraft OEMs such as Airbus and Boeing depict a paradigm shift towards the adoption of more fuel-efficient aircraft by airlines around the world, including Europe. It is, thereby, creating a positive outlook for the market in focus.

Germany to Witness Robust Growth During the Forecast Period Due to Flourishing Space Industry

Europe is continuously at the forefront of space exploration. Currently, it holds the second-largest public space budget in the world, with numerous active satellite R&D programs and manufacturing facilities spanning different European countries. Two factors foster the growth of the focus market in Germany: One is an increased budget dedicated to the R&D of innovative satellite-based products and services, and the other is the introduction of space economy-friendly government initiatives that incentivize both public and private users of satellite-based services such as the mandatory inclusion of GNSS-enabled in-vehicle technology. The huge demand also fostered satellite manufacturers to ramp up their production facilities to meet project deadlines. Besides composites are also used extensively in booster rockets. Eminent space launchers such as the Falcon9 (SpaceX) and Ariane 6 (ESA/ASL) are built with the help of carbon composites. On this note, the CFP boosters of the Ariane 6 are developed and later manufactured by MT Aerospace and AVIO by means of a coiling process.

Also, to improve air transport in the country, the largest airline in the country, Lufthansa, is expanding its fleet of aircraft. With constant plans for expansion, the airline is consistently engaged in the modernization of its long-haul fleet. The newly ordered 20 Boeing 787-9 and 20 additional Airbus A350-900 planes will be delivered to Germany between 2022 and 2027. In addition to this, Germany is a world leader in lightweight engineering technology. The growing demand for materials, such as composites, carbon fiber, etc., from the aviation and satellite manufacturing industry is expected to drive market growth.

Europe Aerospace Composites Industry Overview

The European Aerospace Composites Market is highly competitive, and it is marked by the presence of many prominent players, such as Toray Industries Inc., Hexcel Corporation, Solvay SA, DuPont, and Airborne, competing for the market share. Strategic acquisitions are considered a measure to enhance production capabilities and technical expertise to serve new emerging sub-segments. Companies are investing significantly in developing advanced carbon fiber materials that can overcome the challenges associated with the materials available today. Companies are also collaborating with research institutions to work on advanced materials that can shape the future of materials used by the aviation industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fiber Type

- 5.1.1 Glass Fiber

- 5.1.2 Carbon Fiber

- 5.1.3 Ceramic Fiber

- 5.1.4 Other Fiber Types

- 5.2 Application

- 5.2.1 Commercial Aviation

- 5.2.2 Military Aviation

- 5.2.3 General Aviation

- 5.2.4 Space

- 5.3 Country

- 5.3.1 United Kingdom

- 5.3.2 Germany

- 5.3.3 France

- 5.3.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Airborne

- 6.1.2 Bally Ribbon Mills

- 6.1.3 Belotti SpA

- 6.1.4 DOPAG India Pvt. Ltd

- 6.1.5 DuPont

- 6.1.6 Hexcel Corporation

- 6.1.7 Materion Corporation

- 6.1.8 Mitsubishi Chemical Carbon Fiber and Composites Inc.

- 6.1.9 SGL Carbon SE

- 6.1.10 Solvay SA

- 6.1.11 Teijin Carbon Europe GmbH

- 6.1.12 Toray Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS