PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1407018

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1407018

NOR Flash Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

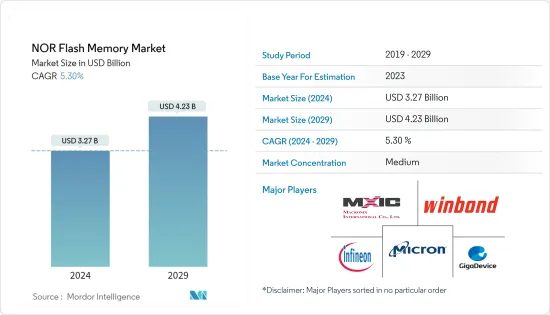

The NOR Flash Memory Market size is estimated at USD 3.27 billion in 2024, and is expected to reach USD 4.23 billion by 2029, growing at a CAGR of 5.30% during the forecast period (2024-2029).

Key Highlights

- NOR flash memory remains useful for code storage and low-end embedded applications but is not a serious contender for high-capacity storage applications. In the automotive space, NOR products are used in infotainment systems, advanced driver assistance systems (ADAS), and dashboard instrument clusters. Some leading automotive ADAS manufacturers have already been using NOR flash. For Example, Bosch uses the automotive-grade Serial NOR Flash memories from Cypress Semiconductor Corporation, which Infenion now acquires to manufacture its video-based Advanced Driver Assistance Systems (ADAS). The usage is expected to boost the storage of system boot code and algorithms at temperatures up to +125 degree C.

- Additionally, the growing digitalization is driving demand for data logging requirements, artificial intelligence, and over-the-air updates, which are mainly incorporated by wearables. This demand for technology in wearables is also creating opportunities in the global NOR flash memory market. For instance, according to the Consumer Technology Association (CTA), the sales revenue of wearables in the United States is anticipated to reach USD 13.8 billion in 2023.

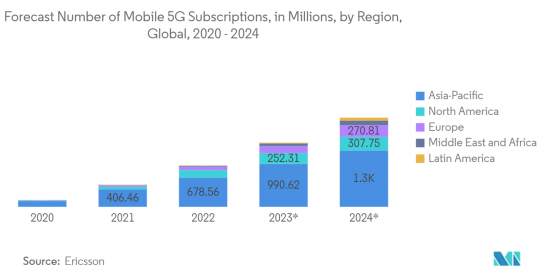

- The expanding telecommunication sector is also anticipated to support the studied market's growth. For instance, following 4G, 5G is the next generation of wireless communication technology for digital cellular networks. 5G technology, with its fast speed, huge bandwidth (up to 10Gb/s), and ultra-low latency, could enable new applications that were previously unimaginable. NOR Flash is widely employed in wireless base stations because it meets the modern world's high reliability and availability demand. NOR Flash, unlike NAND Flash, allows SoCs (system-on-chip devices) and FPGAs (field-programmable gate arrays) to boot from it directly and consistently; hence, it is frequently used to store firmware images. It is also clear how the rapidly expanding 5G infrastructure would increase demand for NOR Flash.

- Furthermore, the current semiconductor shortages and undersupply of other memory products, such as NAND and DRAM, have increased demand and the average selling price of NOR Flash products since the pandemic. However, over the coming years, the ASP of NOR Flash is expected to decline due to growing stockpiles, which will impact the growth of the studied market.

- Research and development costs are also a costly affair in the NOR flash memory market, which is expected to increase with the growing end-user requirements. Vendors like Micron have recently announced investments worth billions to construct new fabrication & R&D facilities for memory manufacturing to cater to the growing demand across industries like automotive, data centers, and memory applications in artificial intelligence and 5G. This indicates the costly setup for research and development and the fabrication process, which continues to remain among the challenging factors for the growth of the studied market.

NOR Flash Memory Market Trends

Communication to be the Largest End-user Application

- Communications and Telecom represent the largest segment of the market. The amount of data generated worldwide is increasing at a rapid pace. The explosion of data is fueled by a plethora of embedded devices that produce a small amount of data for each discrete transaction and add up to big data when clubbed together. Organizations collect data from a range of sources, including smart (IoT) devices, business transactions, industrial equipment, social media, etc.

- The need to respond to evolving market standards in a compressed time-to-market window has resulted in the widespread use of field-programmable gate arrays (FPGAs) and complementary system-on-chip devices (SoCs) in a wide range of wireless infrastructure applications. FPGAs and SoCs require configuration each time the system is powered up. These devices can be configured by diverse types of memories, including Flash.

- Unlike NAND flash, NOR flash memories provide high reliability with low latency in initial response and boot. In addition, advances in NOR Flash process technology, such as MirrorBit technology, which stores two bits per memory cell, support greater density scaling than floating-gate technology. The increased density enables monolithic 1-GB and higher density NOR flash products required for 5G wireless infrastructure. Due to such characteristics, NOR flash memories are widely used in wireless infrastructure applications.

- With the growing demand for 5G, the number of 5G base stations is increasing globally. 5G base stations are expected to need a significant amount of memory chips, as they are usually equipped with high-density NOR flash with 1 or 2 gigabytes of memory, fueling the demand for the market studied.

- Also, a growth in machine-to-machine (M2M) wireless solutions is creating a significant demand for NOR Flash memory. Embedded memory, like NOR Flash, can enable short-range radio solutions (Wi-Fi, ZigBee, Z-wave, Bluetooth, and IP500).

China to Hold Major Market Share

- The rise in the trend of portable electronic devices combined with the growing penetration of advanced technologies, like IoT, among the population across china acts as one of the major factors driving the growth of the NOR flash memory market. The increase in the sales of consumer electronics in China is escalating the growth of the NOR flash market.

- For instance, according to the State Council of the People's Republic of China, significant electronics manufacturers' added value increased 12.7% year over year in the two months between January and February 2022, as opposed to the 7.5% growth experienced by the nation's entire industrial sector. The demand for NOR flash memory devices is driven by China, the world's top producer of consumer electronics such as TVs, cellphones, laptops, and PCs.

- The concentration of electronics manufacturing in China has provided a foundation for the significant development of IoT products in the country, further stimulated by massive domestic consumer demand. IoT development in China also benefits from massive state-led spending on enabling infrastructure. For instance, China recently announced a three?year plan for new IoT infrastructure development (2021?2023), targeting the initial completion of new IoT infrastructure in major cities by the end of 2023. Such initiatives will fuel the growth of IoT-enabled smart devices, facilitating market growth.

- With the growing demand for 5G, the number of 5G base stations is increasing globally. According to the Ministry of Industry and Information Technology (MIIT), China aims to have 2 million installed 5G base stations in 2022 to expand the country's next-generation mobile network. According to MIIT, the Chinese mainland currently has 1.425 million installed 5G base stations that support more than 500 million 5G users nationwide, making it the biggest network in the world. According to the ministry, the country has a 24.3% 5G penetration rate. IoT and other intelligent automation applications that use NOR memory devices are expanding as a result of 5G networks being more widely used.

NOR Flash Memory Industry Overview

The NOR Flash Memory market is moderately competitive, with major vendors such as Infineon, Micron Technology, GigaDevice Semiconductor (Beijing) Inc., and Winbond Electronics Corporation dominating the market. High entry barriers make it difficult for new players to enter the market. Existing vendors are investing heavily in researching and developing new and innovative products.

In May 2023, GigaDevice, a leading flash memory manufacturer, launched GD25LE128EXH, the industry's smallest 128Mb SPI NOR Flash in the ultra-compact 3x3x0.4mm FO-USON8 package. According to the company, with only 0.4m thickness, the GD25LE128EXH offers unparalleled flexibility in designing compact applications, making it the ideal code storage unit for wearables, IoT, healthcare, and networking products that demand low power consumption and high functionality.

In March 2023, GigaDevice introduced the GD25UF series of SPI NOR Flash in its strategic roadmap of 1.2V Flash products, which support systems-on-chip (SoCs) and applications processors built on advanced function nodes. The GD25UF SPI NOR Flash products are optimized for applications that require ultra-low power consumption or a small board footprint.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Digitalization and Emergence of Data-Centric Applications

- 5.1.2 Growing Applications of IoT

- 5.2 Market Restraints

- 5.2.1 High Cost of R&D and Fabrication

- 5.2.2 Availability of Substitutes

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Serial NOR Flash

- 6.1.2 Parallel NOR Flash

- 6.2 By End-user Application

- 6.2.1 Communication

- 6.2.2 Consumer Electronics

- 6.2.3 Automotive

- 6.2.4 Industrial

- 6.2.5 Other End-user Applications

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Japan

- 6.3.4 China

- 6.3.5 Rest of the World

- 6.4 By Density

- 6.4.1 2 MEGABIT and LESS NOR

- 6.4.2 4 MEGABIT and LESS (>2MB) NOR

- 6.4.3 8 MEGABIT and LESS (>4MB) NOR

- 6.4.4 16 MEGABIT and LESS (>8MB) NOR

- 6.4.5 32 MEGABIT and LESS (>16MB) NOR

- 6.4.6 64 MEGABIT and LESS (>32MB) NOR

- 6.4.7 Other Densities

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Micron Technology Inc.

- 7.1.3 GigaDevice Semiconductor Inc.

- 7.1.4 Macronix International Co. Ltd

- 7.1.5 Winbond Electronics Corporation

- 7.1.6 Integrated Silicon Solution Inc.

- 7.1.7 Microchip Technology Inc.

- 7.1.8 Renesas Electronics Corporation

- 7.1.9 Elite Semiconductor Microelectronics Technology Inc.

- 7.1.10 Wuhan Xinxin Semiconductor Manufacturing Co. Ltd (XMC)

8 VENDOR MARKET SHARE

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITES AND FUTURE TRENDS

11 PRICING ANALYSIS