PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408491

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408491

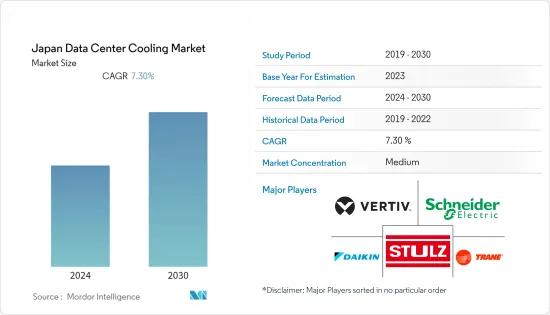

Japan Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030

The Japan data center rack market reached a value of USD 670.2 million in the previous year, and it is further projected to register a CAGR of 7.3% during the forecast period.

Key Highlights

- The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country/region.

- The upcoming IT load capacity of the Japan data center market is expected to reach 2100 MW by 2029. The country's construction of raised floor area is expected to increase to 10K sq. ft by 2029.

- The country's total number of racks to be installed is expected to reach 512K units by 2029. Osaka and Tokyo are expected to house the maximum number of racks by 2029. Throughout the year, temperatures typically fluctuate between 2°C and 30°C, rarely dropping below -1°C or above 0.5°C.

- There are close to 32 submarine cable systems connecting Japan, and many are under construction.

Japan Data Center Cooling Market Trends

Liquid-based Cooling is The Fastest Growing Segment

- Technological advances have made liquid cooling easier to maintain, more scalable, and more affordable, reducing data center liquid consumption by more than 15% in tropical climates and by 80% in greener areas. The energy used for liquid cooling can be recycled to heat buildings and water, and advanced artificial refrigerants can effectively reduce the carbon footprint of air conditioners.

- Some Japanese companies already use snow as a coolant for at least several months of the year. Based in Niigata prefecture on Japan's north coast, DataDock Inc. cools its servers in Nagaoka City with snowmelt and cold outside air.

- Japanese data center providers KDDI and NTT DATA are researching immersion technology to significantly reduce energy waste in cooling server hardware. In KDDI's field test, we achieved an astounding result of reducing power consumption during temperature control by 94% compared to conventional air cooling systems. KDDI said IT equipment is often thought of as the biggest consumer of power, but about half of the total power consumption in data centers is used for cooling.

- Direct liquid cooling (DLC) solutions can achieve partial power usage effectiveness (PUE) values ranging from 1.02 to 1.03, surpassing the efficiency of even the most advanced air cooling systems by a low single-digit margin. It is important to note, however, that PUE does not account for a significant portion of the energy efficiency improvements attributed to DLC. In traditional server setups, fans are responsible for power consumption within the server rack, and this power usage is factored into the IT power section of the PUE calculation. These fans are considered an integral part of the data center's overall energy consumption.

- Japan is one of the three largest markets for e-commerce. It is placed ahead of the United Kingdom but behind the United States. The e-commerce market in Japan is primarily driven by high internet penetration, secured by the Hi-tech network infrastructure. M-commerce is experiencing significant expansions. Mobile sales were projected to outpace the overall B2C e-commerce market until 2022. The mobile commerce market size in Japan stood at around JPY 4.9 trillion as of 2021. It has more than doubled over the last decade. Such instances cater to the major demand for colocation with the increasing demand for improved cooling services.

IT & Telecommunication is the Largest Segment

- Japan is home to major ICT organizations such as Sony, Panasonic, Fujitsu, NEC, and Toshiba, which continue to play a key role in the country's expansion as a major center for ICT. In addition, the orderly development of numerous modernization and expansion projects in the country, along with increasing government spending on maintaining high-quality and advanced infrastructure, are also driving the growth of the market.

- The rapid growth of the E-Japan strategy, which focuses on the development of local e-government projects involving citizen participation, self-evaluation, and feedback on online government services, will drive future growth of the Japanese ICT market.

- The Japanese government is making efforts to accelerate the digital transformation of the private sector and support emerging SMEs. In 2021, the Japanese government, led by the Ministry of Economy, Trade and Industry and the Ministry of Internal Affairs and Communications, published guidelines for promoting digital transformation within organizations, especially targeting small and medium-sized enterprises. Similarly, guidelines on implementing AI, cybersecurity, and secure cloud services were also published in the same year.

- In November 2022, digital infrastructure provider Equinix announced it would expand its digital infrastructure footprint in Japan with a USD 115 million investment in new data centers. The new data center will enhance corporate connectivity with global networks and cloud service providers, enabling them to scale and strengthen Japan's growing digital economy.

- In June 2022, the Japanese government announced that it would deploy wireless networks to 99% of the population by the end of 2030. Its basic policy to promote digitalization and submarine cables is scheduled to be completed throughout Japan by the end of 2025.

Japan Data Center Cooling Industry Overview

The Japan data center cooling market is moderately competitive and has recently gained a competitive edge. Currently, a few major players, including Stulz GmbH, Schneider Electric SE, Vertiv Group Corp., Daikin Industries Ltd, and Trane Inc., hold a dominant position in the market.

In March 2023, STULZ, a Hamburg-based mission-critical air conditioning company, made a significant announcement regarding its industry-leading CyberAir 3PRO DX series. They revealed that some units within this series are now compatible with the low global warming potential (GWP) refrigerant R513A. This groundbreaking development underscores the company's ongoing commitment to delivering the most sustainable air conditioning systems for data centers. Additionally, STULZ has expanded its product portfolio to incorporate the use of R513A refrigerant.

In February 2022, Gigabyte introduced pioneering high-performance computing servers based on AMD EPYC and Nvidia A100 technology. These servers are equipped with CoolIT's direct liquid cooling system. The new machines feature 1 or 2 AMD EPYC 7003 series 'Milan' processors, boasting up to 128 cores, as well as 4 or 8 Nvidia A100 80GB SXM4 modules. CoolIT, known for its unique direct liquid cooling system, ensures separate cooling for the CPU and GPU, optimizing performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development of IT Infrastructure in the Region

- 4.2.2 Emergence of Green Data Centers

- 4.3 Market Restraints

- 4.3.1 Costs, Adaptability Requirements, and Power Outages

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Cooling Technology

- 5.1.1 Air-based Cooling

- 5.1.2 Liquid-based Cooling

- 5.1.3 Evaporative Cooling

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Vertiv Co.

- 6.1.2 Schneider Electric SE

- 6.1.3 STULZ GMBH

- 6.1.4 Daikin Industries Ltd

- 6.1.5 Trane Inc.

- 6.1.6 Johnson Controls International PLC

- 6.1.7 Mitsubishi Electric Corporation

- 6.1.8 RITTAL Electro-Mechanical Technology Co. Ltd (RITTAL GMBH & CO. KG)

- 6.1.9 Nortek Air Solutions

- 6.1.10 Munters Air Treatment Equipment (Beijing) Co. Ltd

- 6.1.11 CoolIT Systems Inc.

- 6.1.12 Asetek AS

- 6.1.13 Wakefield-Vette Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS