PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408496

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408496

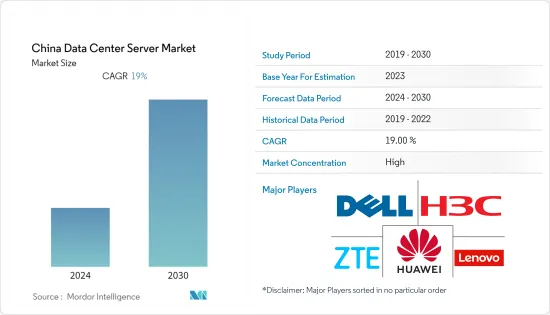

China Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030

The China data center server market reached a value of USD 7.6 billion in the previous year, and it is further projected to register a CAGR of 19% during the forecast period. The increasing demand for cloud computing among (small and medium-sized enterprises) SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country/region.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the China data center market is expected to reach 3300 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 12 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 599.4K units by 2029. Beijing is expected to house the maximum number of racks by 2029.

- Planned Submarine Cables: There are close to 19 submarine cable systems connecting China, and many are under construction. One such submarine cable that is estimated to start service in 2023 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 Kilometers with landing points from Chung Hom Kok, China.

China Data Center Server Market Trends

IT and Telecom to Hold Significant Growth

- The demand for data center servers in the IT and telecom industry is rising with increasing network traffic. Telecom data centers are responsible for managing network resources, such as vRAN and 5G packet core. In contrast, IT data centers are responsible for the IT applications used by the telecom service.

- The telecommunications industry in China experienced several waves of reforms in the last three decades towards liberalization and privatization. Nowadays, China has become one of the largest telecommunications markets in the world. As of 2022, China had more than one billion Internet users, accounting for more than one-fifth of Internet users over the world.

- China's major telecom operators are increasing the proportion of servers they buy that are powered by domestic chips. Huawei states that China Telecom ordered 53,401 servers powered by domestic chips for the 2022-2023 period. This is a significant increase from the 24,823 domestic servers they purchased in the 2020-21 period. With many years of R&D and production expertise, ZTE servers and storage products have been used in over 40 countries and regions, including five major R&D bases in Shenzhen, Nanjing, Changsha, Chengdu, and Shanghai.

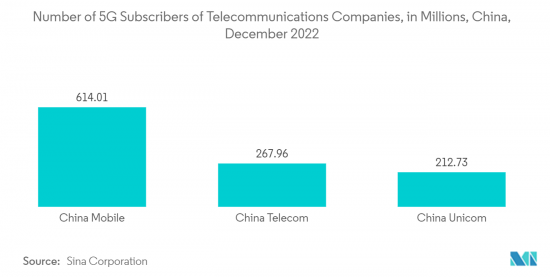

- China has become the country with the largest mobile-cellular user base worldwide. When 5G (fifth generation) technology started to hit the market in 2019, China became one of the frontrunners in the global 5G deployment and 5G devices production race. By 2025, China was forecasted to host the most 5G connections in the world, approximately equaling the sum of North America, Asia-Pacific developed countries, and Western Europe. Such factors are expected to create major data center construction, leading to more demand for servers.

Rack Server to Hold Significant Share

- Rack servers are compact and efficient devices that can handle a variety of computing tasks and are commonly used in data center environments where space is at a premium. The advantages of a server rack include increased scalability, maximized airflow when coupled with a cooling system, and ease of regular computer maintenance and diagnostics.

- The province with the highest concentration of server companies is Jiangsu Province, where 30.3% of China's server companies are located, followed by Guangdong Province and Zhejiang Province. In China, there is a demand for rack servers due to the above advantage, and with increasing digitalization, the market is expected to increase.

- The Chinese government is also doubling down on its efforts to boost computing power to help accelerate domestic artificial intelligence (AI) development amid a growing technological rivalry with the US. According to the National Association of Software and Service Companies (NASSCOM), China's IT spending accounts for 1.4% of the country's gross domestic product (GDP), and 2.7% of its total IT expenditure is spent on cloud services, which is expected to increase by more than 10% in coming five years.

- E-government services were brought in to simplify various government processes online and provide better services to the citizens. The Chinese e-government portal currently accounts for a user base of 29.21 million and offers services such as registering businesses, bill payments, and emergency response information.

- The online financial transactions carried through various financial applications are increasing potentially. WeChat and Alipay are the two preferred applications by users for conducting cashless payments in China. Almost 64% of the users in China have both applications to complete their financial transactions. As of December 2021, the user base of online payment in China reached 904 million, compared to 49.29 million in December 2020, implying that 87.6% of the population preferred online payments. Such factors are expected to drive the companies to keep their rack server allocation for the anticipated growth in the data from these transactions.

China Data Center Server Industry Overview

The China data center server market is fairly consolidated among top players and has gained a competitive edge in recent years. Some of the major players include such as Huawei Technologies Co., Ltd., Dell Inc., Lenovo Group Limited, and others. These major players with a prominent market share focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

In September 2022, Lenovo Group Ltd. announced dozens of new servers, storage systems, and hyper-converged infrastructure appliances, as well as a cloud-based hardware management service. Its new servers can run financial analytics applications up to 70% faster than its previous-generation hardware. Developing artificial intelligence applications is another task that the company promises to speed up significantly for customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Deployment of 5G and Network Traffic

- 4.2.2 Demand for Cloud Computing Among Enterprises

- 4.3 Market Restraints

- 4.3.1 High CaPex for Building Data Center Along With Security Challenges

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Form Factor

- 5.1.1 Blade Server

- 5.1.2 Rack Server

- 5.1.3 Tower Server

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-User

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Huawei Technologies Co., Ltd.

- 6.1.3 Lenovo Group Limited

- 6.1.4 New H3C Technologies Co., Ltd.

- 6.1.5 Nanjing ZTE software Co. Ltd.

- 6.1.6 Shenzhen Innovision Technology Co.,Ltd

- 6.1.7 Inspur Group

- 6.1.8 Kingston Technology Corporation

- 6.1.9 Dawning Information Industry Company Limited (Sugon)

- 6.1.10 Hyllsi Technology Co., Ltd.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS