PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408521

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408521

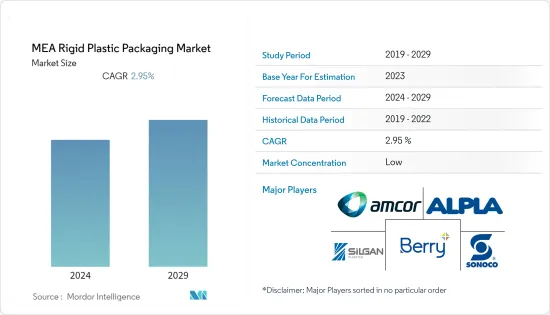

MEA Rigid Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Middle East And Africa Rigid Plastic Packaging Market was valued at USD 17.66 billion in the previous year and is expected to register a CAGR of 2.95% during the forecast period to become USD 21.19 billion by the next five years.

Key Highlights

- The recyclable rigid plastic packaging products are made of plastic jars with open tops and independent lids, closures, or covers. Large rigid containers are widely used in supermarkets and shops to transport various products, including foods, products, and pharmaceuticals. Therefore, rigid plastics' durability and ability to be recycled are the main factors driving the industry in the region.

- Many countries' governments in the region are supporting the adoption of recyclable plastic in the mainstream of packaging solutions and creating an environment to develop recyclable packaging manufacturing facilities in the region, which could drive the market in the studied period. For instance, in January 2023, The UAE's Ministry of Industry and Advanced Technology (MoIAT) published a decree regulating the sale of recycled plastic water bottles by the highest standards of food safety and public health, which will aid in luring new investments by growing the plastic recycling sector.

- The Middle East and Africa region is experiencing a surge in demand for Recyclable Rigid Plastic Bottles (rPET). Several international beverage companies have initiated pilot programs to incorporate rPET into their products, potentially stimulating the market. For example, the Supreme Committee for Delivery & Legacy (SC) of Qatar and the Coca-Cola MIDA declared in November 2022 the implementation of 100% Recycled PET Bottles for the Coca-Cola portfolio of beverages in FIFA World Cup 2022 venues, including Stadiums and Fan Zones.

- Plastics represent a severe environmental risk if they are not managed appropriately at the start of the value chain and throughout their prolonged existence, especially in the ocean. Due to increased plastic production and use in the Arabian Gulf and shipping and waste disposal practices, the amount of plastic waste on the ocean's surface and beaches has increased. Plastic packaging companies must adhere to suitable recycling regulations to introduce their products in the region, restricting the market growth.

MEA Rigid Plastic Packaging Market Trends

Polyethylene (PE) Occupies the Largest Market Share

- Polyethylene is a type of plastic that is highly durable, chemically resistant, and cost-effective. It is composed of petroleum polymers and can withstand any environmental challenge. PE is divided into three main categories: High-Density Polyethylene or HDPE, Low-density Polyethylene or LDPE, and Linear Low-Density polyethylene or LLDPE.

- PE is the most consumed plastic product in the Middle East and Africa. High versatility, easy processability, and recyclability are the primary reasons for the high demand for PE in several packaging applications. Companies such as SABIC and Takween offer many products made from HDPE copolymers and homopolymers for rigid plastic packaging markets. For instance, Takween offers HDPE bottles and containers.

- Moreover, the need for LDPE is also increasing in food packaging, and market vendors in the region are capitalizing on the opportunity and offering LDPE for food packaging. For instance, Qatar Petrochemical Company (QAPCO) offers LDPE plastic for food packaging applications. That is also expected to boost the demand for LDPE bottles in the region in the future.

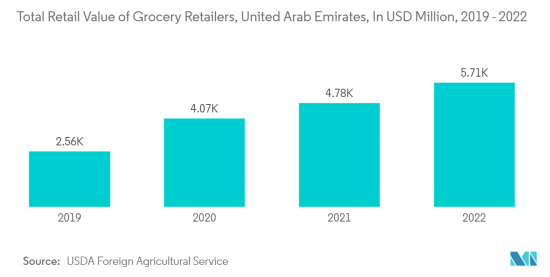

- The United States Department of Agriculture (USDA) Foreign Agricultural Service has reported that in 2022, grocery retail sales in the United Arab Emirates, excluding sales tax, amounted to approximately USD 23.44 billion, a significant increase from the previous year's total of USD 22.15 billion. As the grocery retail sector continues to grow, there is a heightened focus on preserving the quality and freshness of products along the entire supply chain. This could result in a greater need for rigid PE packaging solutions that provide superior protection against external elements.

United Arab Emirates (UAE) to Show Significant Growth

- The country's pharmaceutical sector has witnessed significant growth in the past few years owing to the growing government initiatives and the rise in the production capacity of medicines. This growth is creating considerable growth opportunities for rigid plastic packaging market vendors as High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Polyethylene terephthalate (PET), etc., are widely used in pharmaceutical packaging. For instance, HDPE is the most common rigid plastic for solid pharmaceutical products, creating moisture-resistant and structurally rigid containers.

- Further, United Arab Emirates-based companies have increased their production capacity by enhancing manufacturing capacities, driving the demand for medicine packaging, and creating opportunities for rigid plastic packaging market vendors. For instance, in June 2022, Bioventure Healthcare, a United Arab Emirates-based pharmaceutical manufacturing company, planned to double the production capacity of its factory by launching new lines of tablets, capsules, and sachets, which would create a demand for plastic packaging, including the blister packaging in the country.

- In addition, Dubai is continuing its efforts to become a world-class industrial and manufacturing center and attracting substantial investments across critical sectors as part of Dubai Industrial Strategy 2030. Dubai Industrial Strategy 2030 projects an additional growth of USD 5 billion in the industrial sector by 2030. With the development of the region's personal care and cosmetics sector, there is a massive need for rigid plastic packaging for cosmetics and personal care products. For example, the multinational manufacturer of medicinal products, herbal products, and personal care products, Himalaya Wellness, will construct a factory at Dubai Industrial City, one of the region's largest manufacturing centers. The project is expected to start commercial production in the first quarter of 2024. This could increase demand for personal care packaging products within the country.

- According to the Department of Economic Development (Dubai), In 2022, e-commerce sales in the United Arab Emirates (UAE) were around USD 27 billion. E-commerce businesses often require customized packaging to enhance their brand identity and improve customer experience. Rigid plastic packaging can be efficiently designed, molded, and printed upon, allowing companies to create unique, eye-catching packaging designs.

MEA Rigid Plastic Packaging Industry Overview

The rigid plastic packaging market is highly competitive. Manufacturers seek lightweight, high-performing plastic grades to reduce costs and improve packaging performance. Some of the most well-known rigid plastic packaging manufacturers include Amcor Plc, ALPLA, Silgan Holdings, Seal Air Corporation, Plastipak Holding, and Sonoco Products Company, among others.

In July 2023, Packaging specialist ALPLA launched a new brand, ALPLARECYCLING. The plastic packaging company had 13 plants, including four joint ventures with regional partners. The company aims to process at least 25% post-consumer (PCR) material by 2025. After investing millions into new sites in South Africa, Romania, and Thailand and a site extension in Poland, packaging specialist ALPLA is consolidating all its activities under the brand ALPLArecycling.

In November 2022, Sonoco planned to open a new protective packaging manufacturing plant in Bursa (Turkey). The production of Sonopost packaging is scheduled to commence in the 4th Quarter of 2022 and was to be further extended to meet the increasing demand for EPS-free packaging. The new Sonoco Protective facility was to include a Design and Testing Laboratory to support customers in the packaging design.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot (Trend Analysis of the Plastic Manufacturing Processes)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Recyclable Rigid Plastic Packaging is Expected to Grow Due to the New Regulation

- 5.1.2 Increasing Demand for Rigid Plastic Packaging to Extend Shelf Life of Products

- 5.2 Market Restraints

- 5.2.1 Environmental Concerns Over Safe Disposal and Price Volatility of the Raw Materials

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Bottles and Jars

- 6.1.2 Trays and Containers

- 6.1.3 Caps and Closures

- 6.1.4 Other Products (Blister and Clamshell Packs and Rigid Plastic Tubes)

- 6.2 By Material

- 6.2.1 Polyethylene (PE)

- 6.2.2 Polyethylene Terephthalate (PET)

- 6.2.3 Polypropylene (PP)

- 6.2.4 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.2.5 Polyvinyl Chloride (PVC)

- 6.2.6 Other Rigid Plastic Packaging Materials

- 6.3 By End-user Industry

- 6.3.1 Food and Beverage

- 6.3.2 Healthcare

- 6.3.3 Cosmetics and Personal Care

- 6.3.4 Industrial

- 6.3.5 Building and Construction

- 6.3.6 Automotive

- 6.3.7 Other End-user industries (Electrical and Electronics)

- 6.4 By Country

- 6.4.1 United Arab Emirates

- 6.4.2 Saudi Arabia

- 6.4.3 Egypt

- 6.4.4 South Africa

- 6.4.5 Rest of Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Berry Global Inc.

- 7.1.3 Alpla Werke Alwin Lehner GmbH & Co KG

- 7.1.4 Silgan Holdings Inc.

- 7.1.5 Sealed Air Corporation

- 7.1.6 Plastipak Holding, Inc.

- 7.1.7 Sonoco Products Company

- 7.1.8 Zamil Plastic Corporation

- 7.1.9 Packaging Products Company (PPC)

- 7.1.10 Saudi Arabian Packaging Industry WLL (SAPIN)

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS