Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408553

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408553

Africa Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030

PUBLISHED:

PAGES: 100 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

The Africa data center server market reached a value of USD 2.3 billion in the previous year, and it is further projected to register a CAGR of 15.4% during the forecast period. The increasing demand for cloud computing among small and medium-sized enterprises (SMEs), government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the region.

Key Highlights

- The upcoming IT load capacity of the Africa data center construction market is expected to reach 1226 MW by 2029.

- The region's construction of raised floor area is expected to increase 5.2 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 260K units by 2029. South Africa is expected to house the maximum number of racks by 2029.

- There are close to 70 submarine cable systems connecting Africa, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Africa-1, which stretches over 10,000 Kilometers with a landing point in Port Said, Ras Ghareb, Egypt.

Africa Data Center Server Market Trends

IT & Telecommunication Segment Holds the Major Share.

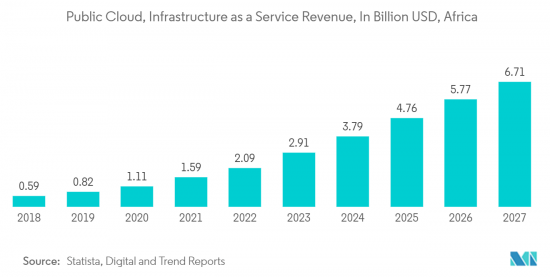

- The need for data localization has recently encouraged global cloud aggregators to introduce cloud data centers in the country. This highlights regional investment's growing demand and favorability, helping sectors like the cloud grow.

- Cloud infrastructure offers users increased scalability and remote access, helping companies choose it as a critical part of their operations in technology-driven businesses. The market share for cloud users is expected to increase from 7.25% in 2022 to around 8.6% by 2029. Since data centers and payrolls of highly skilled cloud maintenance staff are cheaper than big international cloud aggregators, even public services rely on service providers like Google, Microsoft, and AWS.

- As data colonialism is rampant, African governments and private companies would seek more data centers and cloud service providers on domestic premises to keep data within the continent and secure within their territory for added security. As the authorities see the need to improve the contribution of their regions to the international markets, the improved cloud scenario would generate significant demand for data centers in the region.

South Africa is Expected to Witness Significant Growth in the Region

Africa Data Center Server Industry Overview

Additional Benefits:

Product Code: 50001186

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of cloud computing services

- 4.2.2 Advent of 5G networks

5 MARKET SEGMENTATION

6 COMPETITIVE LANDSCAPE

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.