PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408562

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408562

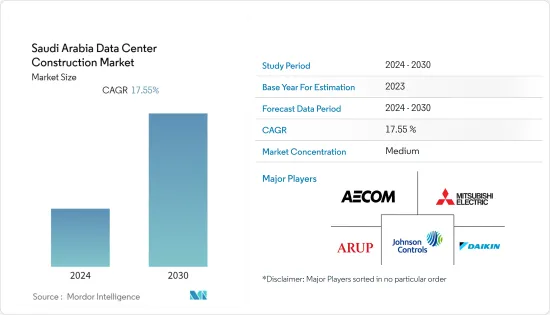

Saudi Arabia Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030

The Saudi Arabia Data Center Construction Market is projected to register a CAGR of 17.55% during the forecast period.

Under Construction IT Load Capacity: The upcoming IT load capacity of the Saudi Arabia data center construction market is expected to reach 855 MW in six years.

Under Construction Raised Floor Space: The country's construction of raised floor area is expected to reach 3.4 million sq. ft in six years.

Planned Racks: The country's total number of racks to be installed is expected to reach 170,963 units in six years. Riyadh is expected to house the maximum number of racks in six years.

Planned Submarine Cables: There are close to four submarine cables named Middle East North Africa (MENA) Cable System/Gulf Bridge International, Gulf Bridge International Cable System (GBICS)/Middle East North Africa (MENA) Cable System, Tata TGN-Gulf, Saudi Arabia-Sudan-2 (SAS-2) with landing points Jeddah, Saudi ArabiaRonne, Denmark, Tejn, Denmark, Al Khobar, Saudi Arabia, Al Khobar, Saudi Arabia, Jeddah, Saudi Arabia.

Saudi Arabia Data Center Construction Market Trends

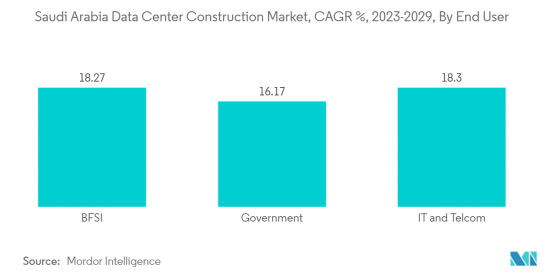

IT and Telecom to have significant market share

- The cloud, telecom, and BFSI end users are anticipated to hold the largest shares among end-user industries. More initiatives are focusing on Industry 4.0 in the BFSI sector, one of the main pillars of the nation's economy.

- The nation is undergoing several digital improvements, helping advance the cloud sector. These programs support Saudi Arabia's Vision 2030.

- Due to users' increasing adoption of 5G networks, the telecom industry is expected to continue to dominate. In six years, 5G mobile data speed is expected to increase significantly to 921 Mbps.

- This supports the idea that data center servers are increasing in demand. The country's adoption of 4G is also fueling growth in the country's data center market. Rapid expansion and installation of IT infrastructure are projected to raise demand during the forecast period. As part of Vision 2030, Saudi Arabia is planning to modernize and automate its economy, and the rise of 5G mobile services in the nation is essential to this effort.

- 5G's disruptive capabilities make new creative and disruptive applications possible. Saudi Arabia will be the first among the nations in Europe, Africa, and the Middle East to make the entire 6 GHz frequency range open for WiFi use, according to the CITC.

- This indicates that the free airwaves available to routers for the next generation of WiFi networks have increased by 150%. Saudi Arabia has now made 2,035 MHz of spectrum available for the next generation of WiFi and other license-exempt technologies, more than any other nation in the world, by assigning 1,200 MHz of the radio spectrum for WiFi6.

Riyadh to be a major hotspot for data center construction in the country

- Riyadh is the major hotspot in Saudi Arabia. Its IT load capacity is expected to reach 441.2 MW in 2023, record a CAGR of 13.40%, and reach 938.4 MW by 2029. Riyadh has the greatest concentration of data centers in the Kingdom. It is an excellent connecting point between Asia, Africa, the GCC, and Europe.

- It has well-connected intersections and is regarded as a strategic location for investment in data centers. The area is recognized as the Kingdom's ICT hub. Over the next five years, Riyadh plans to achieve digital sustainability, cultivate and train local talent, speed up the expansion of the regional economy, increase the rate at which technical jobs are Saudized, and create a robust national economy.

- Cloud services are being adopted more widely in Riyadh. Riyadh hosted the World Cloud and Data Center Show in 2022. The event highlighted fundamental data strategies and digital transformation projects that may propel the next stage of cloud adoption in the Kingdom. The Rest of Saudi Arabia comprises Jeddah, Dammam, and Madinah.

- These cities are in the process of adopting data center facilities. In the coming years, some data centers are expected to be constructed in these locations as part of Saudi Arabia.

Saudi Arabia Data Center Construction Industry Overview

Saudi Arabia Data Center Construction Market is fairly consolidated, some significant players include Johnson Controls International Plc, AECOM, Arup, Daikin Industries Ltd, and Mitsubishi Electric.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 MARKET INSIGHTS

5 Market Overview

6 Industry Attractiveness - Porter's Five Forces Analysis

- 6.1 Bargaining Power of Suppliers

- 6.2 Bargaining Power of Buyers

- 6.3 Threat of New Entrants

- 6.4 Threat of Substitutes

- 6.5 Degree of Competition

7 Key Industry Statistics

- 7.1 Planned/Under Construction IT Load Capacity

- 7.2 Planned/Under Construction Raised Floor Space

- 7.3 Planned/Under Construction Racks

- 7.4 Planned Submarine Cable

8 MARKET DYNAMICS

9 Market Drivers

- 9.1 Rising Adoption of Renewable Energy Sources

- 9.2 Increase in 5G Deployments Fueling Edge Data Center Investments

- 9.3 Smart City Initiatives Driving Data Center Investments

10 Market Restraints

- 10.1 Security Challenges in Data Centers

- 10.2 Location Constraints on the Development of Data Centers

11 MARKET SEGMENTATION

- 11.1 By Infrastructure

- 11.1.1 Electrical Infrastructure

- 11.1.1.1 UPS Systems

- 11.1.1.2 Other Electrical Infrastructures

- 11.1.2 Mechanical Infrastructure

- 11.1.2.1 Cooling Systems

- 11.1.2.2 Racks

- 11.1.2.3 Other Mechanical Infrastructures

- 11.1.3 Other Infrastructures

- 11.1.1 Electrical Infrastructure

- 11.2 By End User

- 11.2.1 IT & Telecommunication

- 11.2.2 BFSI

- 11.2.3 Government

- 11.2.4 Healthcare

- 11.2.5 Other End Users

12 COMPETITIVE LANDSCAPE

13 Company Profiles

- 13.1 Turner Construction Co.

- 13.2 DPR Construction Inc.

- 13.3 Fortis Construction

- 13.4 ABB Ltd.

- 13.5 Delta Electronics

- 13.6 AECOM Limited

- 13.7 Daikin Industries Ltd

- 13.8 Canovate

- 13.9 CyrusOne Inc.

- 13.10 Johnson Controls International Plc

- 13.11 Rittal GmbH & Co. KG

- 13.12 Legrand

- 13.13 Delta Group

- 13.14 EAE Group

- 13.15 Mitsubishi Electric

- 13.16 AECOM

- 13.17 Schneider Electric SE

- 13.18 STULZ GMBH

- 13.19 M+W Group (Exyte)

- 13.20 Mercury Engineering

- 13.21 Arup

14 INVESTMENT ANALYSIS

15 MARKET OPPORTUNITIES AND FUTURE TRENDS