PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408768

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408768

Semiconductor Device In Consumer Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

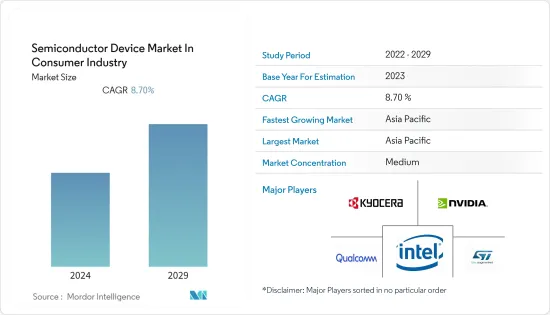

The semiconductor device market in the consumer industry was valued at USD 83.4 billion in the current year and is expected to register a CAGR of 8.7%, reaching USD 126.9 billion over the forecast period.

Key Highlights

- Most consumer electronics, like mobile phones, laptops, game consoles, microwaves, and refrigerators, operate with semiconductors, such as integrated chips, diodes, and transistors. The high demand for these devices is a key factor contributing to the market growth.

- The use of integrated circuits is widespread in consumer electronics with microprocessor control, from cell phones and portable music players to gaming systems, PCs, and other digital devices. An integrated circuit (IC) or chip is an extremely sophisticated device that packs up many electronic components like capacitors, transistors, and resistors into an area of a few square centimeters on a silicon wafer.

- Further, the emergence of trends, such as consumer Internet of Things (IoT), has fueled the demand for the semiconductor devices market in the consumer industry. An ideal example of consumer IoT is the smart home, where electronic equipment, lighting, HVAC systems, and appliances are all controlled and monitored from a central hub. IoT applications cannot work without integrated circuits and sensors, so all IoT devices require semiconductors, which creates a huge growth potential for the market studied.

- Moreover, the explosive growth of smartphones and smart home devices in the markets in recent years has fueled the demand for the semiconductor device market in the consumer industry. The increasing adoption of the fifth-generation (5G) wireless technology for digital devices is also one of the major contributing factors to the rising demand for connected devices and smart products, thereby supporting the market's growth.

- The Russia and Ukraine war negatively impacted the supply chain in the semiconductor Industry. According to SEMI, Ukraine and China supply about 80% of Xenon and krypton gasses. These gasses are highly used in semiconductor manufacturing, and they can be obtained mainly through steel manufacturing and with the help of Air Separation units.

- With the war in place and no dedicated Air Separation Units elsewhere, the lead time for semiconductor manufacturing is increasing, leading to chip shortages across the industries studied.

Semiconductor Device Market Trends

Increase Penetration of Smartphones and Smart Wearable Devices

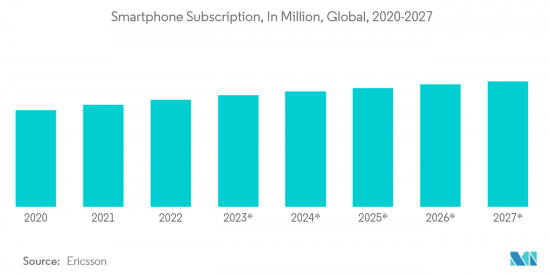

- Due to the increasing population and urbanization, smartphone adoption rates are increasing, particularly in developing countries, which has fueled the demand for the semiconductor device market in the consumer industry. For instance, as per GSMA, by 2025, smartphones are expected to account for four of every five connections, up from 65% in 2019.

- Moreover, as per BankMyCell, as of September 2022, smartphone users worldwide are 6.648 billion, translating to 83.04% of the world's population owning a smartphone. The number of people owning a smart and feature phone is 7.26 billion, making up 91.08% of the world's population.

- Further, the semiconductor device market in the consumer industry will witness high growth due to the growing penetration of 5G technology, which drives the demand for 5G-enabled smartphones. For instance, as per GSMA, by 2025, 5G networks will likely cover one-third of the world's population. In the 5G wireless cellular networks, smartphone battery efficiency and optimal power utilization have emerged as important factors contributing to the growth of semiconductor devices.

- Additionally, several smartphone manufacturers are focusing on launching technologically advanced phones to gain a competitive edge, further supporting the market growth. For instance, in May 2023, Poco announced the launch of Poco F5 in India and global markets. The company is also launching the Poco F5 Pro simultaneously globally.

- Smart wearable devices, such as smartwatches, smart wristbands, fitness trackers, activity trackers, sports watches, and virtual realty (VR) headsets, are integrated with advanced technologies such as artificial intelligence (AI) and the Internet of Things (IoT), which employ a huge number of sensors and integrated circuits (ICs). For instance, fit bits, smartwatches, and pulse oximeters are among the wearable systems incorporated with optical sensors to provide real-time patient health tracking solutions. Therefore, with the increased use of these devices, the overall semiconductor device market in the consumer industry is impacted positively, exhibiting steady growth.

- Many vendors are also focusing on developing new products to meet the growing demands and increase customer base. For instance, in January 2023, 221e srl and STMicroelectronics joined forces to enhance artificial intelligence solutions for wearable, IoT, and other consumer applications based on 221e's sensing AI software and STMicroelectronics's microcontrollers and intelligent sensors.

Asia-Pacific to Dominate the Market

- The semiconductor device market in the consumer industry is projected to be dominated by Asia-Pacific owing to the presence of leading consumer electronics manufacturers. The market is expected to be driven by increasing smartphone penetration, 5G penetration, and smart home appliances.

- Several global companies see the Asia-Pacific region as one of the key markets likely to generate future growth. The growth of the Asia-Pacific consumer market is mainly driven by favorable demographics and increasing disposable income.

- With the presence of significant manufacturers, the region is among the biggest consumer electronics markets. The demand for the semiconductor devices market in the consumer industry is anticipated to increase as the consumer electronics industry expands in several countries. India, for instance, is one of the major global markets for consumer goods and the newest technology. India Brand Equity Foundation (IBEF) predicted that the market for Indian appliances and consumer electronics (ACE) will grow at a 9% CAGR to reach USD 21.18 billion by 2025. Such numbers are estimated to drive the growth of product launches in the region.

- Moreover, the demand growth for smart homes is expected to be driven by rising energy costs, which has led to the adoption of energy-efficient and cost-saving solutions for thermostats, lighting, and smart outlets. Such an increase in the demand for smart home devices and smart power management devices in the market is expected to fuel the demand growth of the semiconductor device market in the consumer industry in the region.

- Furthermore, major industry players focus on expanding their regional operations to stay ahead of the competition. For instance, in March 2023, Samsung announced to build a new semiconductor facility in South Korea by investing USD 228 billion.

Semiconductor Device Industry Overview

The semiconductor device market in the consumer industry is currently experiencing significant fluctuations due to ongoing consolidation, technological advancements, and geopolitical factors. In a market where gaining a sustainable competitive advantage through innovation is of paramount importance, competition is poised to escalate. Given this dynamic environment, brand identity becomes a crucial factor, especially considering the high expectations of quality from end-users in the semiconductor manufacturing sector.

The market is dominated by established giants, including Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Technologies Inc., and STMicroelectronics NV, which have achieved substantial market penetration. In this competitive landscape, innovation, time-to-market, and performance stand out as the key differentiators for industry players. Overall, the competitive rivalry is steadily increasing over the forecast period.

April 2023 witnessed Renesas Electronics Corporation's milestone announcement, as they introduced their first microcontroller (MCU) based on advanced 22-nm process technology. This innovative product launch aims to provide customers with superior performance while reducing power consumption through lower core voltages.

In March 2023, STMicroelectronics and Winbond Electronic Corporation entered into a strategic partnership to amalgamate high-performance memory with STM32 devices for consumer and smart industrial applications. The partnership's goal is to combine Winbond's DDR3 dynamic RAM with ST's STM32M P1 MPUs. These MPUs incorporate up to two Cortex-A7 cores and offer advanced peripherals, IoT security hardware, and highly efficient on-chip power conversion integrated circuits.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macro Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Proliferation of Smart Technologies in the Consumer Electronics Sector

- 5.1.2 Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 5.2 Market Challenges

- 5.2.1 Supply Chain Disruptions

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessors (MPU)

- 6.1.4.4.2 Microcontrollers (MCU)

- 6.1.4.4.3 Digital Signal Processor

- 6.2 By Geography

- 6.2.1 United States

- 6.2.2 Europe

- 6.2.3 Japan

- 6.2.4 China

- 6.2.5 Korea

- 6.2.6 Taiwan

- 6.2.7 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Nvidia Corporation

- 7.1.3 Kyocera Corporation

- 7.1.4 Qualcomm Incorporated

- 7.1.5 STMicroelectronics

- 7.1.6 Micron Technology Inc.

- 7.1.7 Xilinx Inc.

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Toshiba Corporation

- 7.1.10 Texas Instruments Inc.

- 7.1.11 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 7.1.12 SK Hynix Inc.

- 7.1.13 Samsung Electronics co. ltd

- 7.1.14 Fujitsu Semiconductor Ltd

- 7.1.15 Rohm Co. Ltd

- 7.1.16 Infineon Technologies AG

- 7.1.17 Renesas Electronics Corporation

- 7.1.18 Advanced Semiconductor Engineering Inc.

- 7.1.19 Broadcom Inc.

- 7.1.20 ON Semiconductor Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET