PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408857

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408857

Americas Semiconductor Device In Aerospace & Defense Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

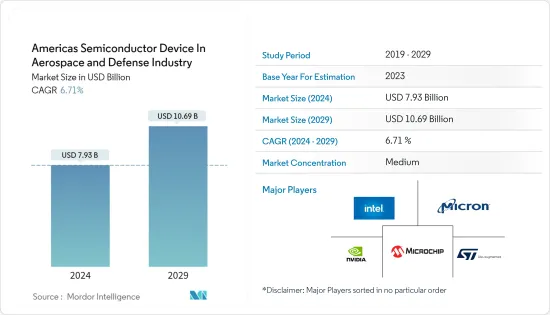

The Americas Semiconductor Device In Aerospace & Defense Industry is expected to grow from USD 7.93 billion in 2024 to USD 10.69 billion by 2029, at a CAGR of 6.71% during the forecast period (2024-2029).

Key Highlights

- The growing military expenditure in countries such as the United States and investments being made across major American countries to modernize the military and aerospace industry's infrastructure are among the major factors driving the growth of the studied market in the region.

- Semiconductor devices have a broad range of applications in the aerospace and defense industries. Semiconductors, for example, are used to power executives, aeronautics, RF frameworks, coordinated aircraft frameworks, and advanced sensing systems. The industry is expected to see a further flood sought after as a result of the growing consumption of advanced electronic devices.

- The Americas, especially the North American region, has been among the pioneers of the aerospace industry as the region is home to some of the largest aerospace companies. Companies such as Boeing and Lockheed Martin are considered among the leading aerospace companies. Apart from fulfilling the local demand for aircraft, these companies also export aircraft globally, which creates a favorable outlook for the growth of the studied market in the region.

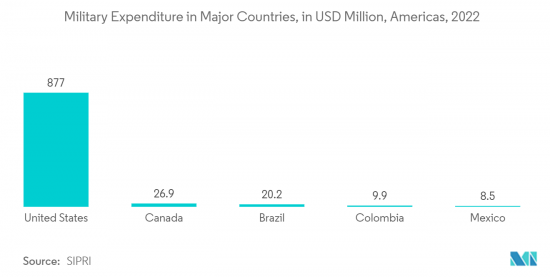

- Furthermore, countries such as the United States are globally recognized for their defense and military prowess. The country spends billions each year to modernize and advance its capabilities. According to the Stockholm International Peace Research Institute (SIPRI), in 2022, about USD 877 billion was spent by the United States on national defense. As the country is among the leading adopters of advanced technologies, such trends support the studied market's growth in the country.

- Apart from the United States, countries such as Canada, Brazil, and Mexico have also started taking initiatives to further strengthen their defense amid the rise in terror activities. For instance, in 2022, the Canadian defense ministry announced an expenditure worth USD 4.9 billion over the course of the next six years to modernize continental defense. The ministry also announced that the government's overall investment in continental and northern defense would exceed USD 40 billion over the next two decades.

- However, the global semiconductor chip shortage is expected to have a significant impact on the growth of the studied market. Additionally, military and defense expenditures largely vary depending upon the macroeconomic condition of any country/region. Hence, the recent recession scare looming over the Americas is expected to challenge the studied market's growth in the region.

Americas Semiconductor Device in Aerospace & Defense Market Trends

Rising Military Expenditure to Drive the Market's Growth

- Traditionally, the United States has been among the leading countries in terms of military expenditure in the American region. However, in recent years, other countries' expenditures, including Canada, Brazil, and Mexico, have also increased significantly. For instance, according to a report by SIPRI, the United States contributed to 39% of world military spending in 2022, remaining the largest military spender in the American region and globally.

- In addition to their own specific developments, military organizations in the Americas are also using more and more electronic components to enhance their battlefield preparedness. This is significantly expanding the use cases for semiconductor devices. For instance, the adoption of optoelectronic devices in recent years has increased significantly in aerospace and defense applications, including laser radar, infrared sensors, optical sonar systems, other night-vision equipment, weapons-grade laser systems, etc.

- Military modernization is becoming a common trend across major American countries, including Canada, Brazil, Mexico, etc. To advance the capabilities of soldiers, advanced electronic devices such as night vision cameras, advanced sensors, and navigation systems are increasingly being adopted by the military across these countries, which drives the demand for semiconductor devices in the region.

- Considering such trends, the demand for lighter semiconductor components has been increasing, which is leading to the development of new manufacturing techniques and the exploration of new material types. For instance, SiC promises lighter-weight components that facilitate higher power density and switching for a given current and voltage rating in a smaller, lighter device. Hence, such trends are expected to influence the studied market's growth in the region.

The United States to Hold a Significant Market Share

- The United States is among the largest aerospace & defense markets in the Americas; hence is expected to hold the largest share of the studied market during the forecast period. Major factors driving the studied market's growth in the country include a large aerospace & defense expenditure, the presence of some of the biggest aerospace and defense equipment manufacturing companies, along a strong research and development sector continuously engaged in the development of advanced semiconductor and electronic devices for the aerospace and defense applications.

- The United States is one of the largest aviation markets and boasts a fleet of thousands of commercial and well as military aircraft. For instance, according to the Federal Aviation Administration (FAA), in 2022, the country had a general aviation fleet of about 204,590 aircraft and a fleet of 6,870 for-hire carriers. As aircraft contain a wide range of electronic systems, such trends support the demand for semiconductor devices in the country.

- The United States is also among the leading aircraft manufacturers (both commercial & defense). For instance, Boeing is among the leading aircraft manufacturer in the country. In 2022, the company delivered about 480 airplanes and won 774 net new orders. Such trends also work in favor of the studied market.

- Furthermore, in recent years, the aerospace sector, which was long limited to national agencies, is now shifting part of its business to private companies. For instance, in the United States, the aerospace industry has witnessed the rise of private companies like Virgin Galactic, SpaceX, Blue Origin, and Rocket Lab, which have numerous activities and ambitions. As these companies are highly focused on developing innovative solutions, such trends create a favorable outlook for the growth of the studied market in the country.

Americas Semiconductor Device in Aerospace & Defense Industry Overview

The Americas semiconductor device market for the aerospace and defense industry has experienced increased competition, primarily driven by the growing adoption of advanced electronic systems. Market players are consistently striving to develop innovative solutions to enhance their market presence. They are also employing strategies such as partnerships, mergers, and acquisitions to expand their customer base and support the creation of new products and solutions. Key market players in this sector include Intel Corporation, NVIDIA Corporation, Microchip Technology Inc., and STMicroelectronics N.V., among others.

In January 2023, NXP Semiconductor unveiled the MMRF5018HS wideband 125 W C.W. GaN on SiC R.F. Power Transistor designed for aerospace and defense communication applications. This transistor is housed in a low Rth NI-400HS air cavity ceramic package, offering high gain and ruggedness. It is well-suited for various R.F. applications, including continuous wave (C.W.), pulse, and wideband applications. Typical uses for this transistor include narrowband and multi-octave wideband amplifiers, jammers, L-Band radar, EMC testing, and emergency service and public mobile radios, among others.

In October 2022, Intel Corporation launched an initiative as part of its foundry platform expansion plan, focusing on creating chips for the U.S. aerospace, military, and government sectors. The initiative, known as the United States Military, Aerospace, and Government (USMAG) Alliance within Intel Foundry Services (IFS), aims to establish a design ecosystem in collaboration with U.S.-based manufacturing. The primary goal is to ensure chip production on advanced process technologies to meet the needs of national security applications in these sectors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact Analysis of Macro Trend on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Military Expenditure

- 5.1.2 Growing Adoption of Advanced Electronic & Semiconductor Devices

- 5.2 Market Restraints

- 5.2.1 Semiconductor Chip Shortage Issue

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro (MCU, MPU, Digital Signal Processor)

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Canada

- 6.2.3 Brazil

- 6.2.4 Mexico

- 6.2.5 Rest of Americas

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 NVIDIA Corporation

- 7.1.3 Microchip Technology Inc.

- 7.1.4 Analog Devices Inc.

- 7.1.5 STMicroelectronics NV

- 7.1.6 Micron Technology Inc.

- 7.1.7 Infineon Technologies AG

- 7.1.8 Texas Instruments Inc.

- 7.1.9 NXP Semiconductors

- 7.1.10 On Semiconductor Corporation

- 7.1.11 OSI Optoelectronics

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET