PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408863

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408863

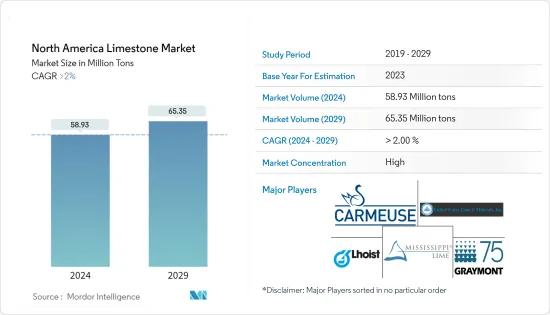

North America Limestone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The North America Limestone Market size is estimated at 58.93 Million tons in 2024, and is expected to reach 65.35 Million tons by 2029, growing at a CAGR of greater than 2% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 since most of the end-use industries witnessed a downturn since the lockdown announced by several countries across the North American region to control the spread of COVID-19. Currently, the market has recovered from the pandemic and is growing at a significant rate.

Key Highlights

- The growth in construction activities and the growing use of limestone in cement production are major factors driving the growth of the market studied.

- However, environmental concerns related to mining and processing are expected to restrain the growth of the market studied.

- Nevertheless, technological advancements for efficient extraction and processing is anticpated to create lucrative growth opportunities for the North American market.

- United States is expected to represent the largest market over the forecast period due to the consumption from various industries.

North America Limestone Market Trends

Building and Construction Sector to Dominate the Market

- Limestone is commonly utilized in construction as crushed stone, aggregate, and dimension stone due to its ability to provide strength, durability, and aesthetic appeal to buildings, roads, and other infrastructure projects.

- In North America, the United States has a major share in the construction industry. Apart from the United States, Canada, and Mexico are also contributing significantly to the construction sector investments.

- The United States has been planning to bring an overhaul to the country's existing infrastructure. In May 2022, the government announced the allocation of over USD 110 billion for carrying out 4,300 specific projects for modernizing airports and ports, rebuilding roads and bridges, and replacing lead pipes to deliver clean water. These projects are expected to benefit around 3,200 communities across the 50 states and create lucrative demand for limestone in the forecast period.

- Furthermore, in Canada, various government projects, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, are set to support the expansion of the sector hugely. In August 2022, the Canadian government announced a significant investment of more than USD 2 billion to fund three important initiatives that will collectively help to develop approximately 17,000 houses for families across the nation, including thousands of affordable housing units.

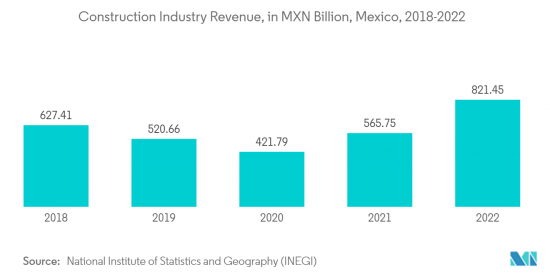

- According to the National Institute of Statistics and Geography (INEGI), the revenue generated by companies in the construction industry in Mexico in 2022 was over MXN 256 billion (~USD 12.75 billion), which is higher than in the previous year.

- Therefore, growing building and construction sector in the region is expected to drive the demand for limestone in the forecast period.

United States to Dominate the Market

- The United States is expected to dominate the limestone market during the forecast period due to the increasing demand from various industries such as construction, paper and pulp, agriculture, and others.

- According to the United States Census Bureau, the annual value for new construction put in place in the United States accounted for USD 1,792.90 billion in 2022, compared to USD 1,626.40 billion in the previous year. Moreover, the annual value of residential construction put in place in the United States was valued at USD 908 billion in 2022, which is an increase of 13 %, compared to USD 803 billion in 2021.

- Lime is a crucial component in producing high-quality paper of varying thicknesses. In technical terms, lime products are utilized in the pulp and paper industry during the recausticizing process to recycle sodium hydroxide for use in the pulp digester.

- The leading paper companies in the United States generated net sales of roughly USD 21 billion for the year ending December 31, 2022. WestRock and International Paper were the leading paper companies in the United States based on revenue. Texas-based Kimberly-Clark followed closely, with a revenue of USD 20.18 billion.

- Agricultural lime has been used by farmers for years as a soil improver. It is also a natural, low-cost way to enhance the effects of regular chemical-based fertilizers.

- According to the United States Department of Agriculture, there were over two million farms in the United States in 2022. Texas was by far the leading state in the United States in terms of total number of farms, with about 246 thousand farms by the end of 2022. Missouri was ranked second, among the leading ten states, with 95 thousand farms as of 2022.

- Therefore, all the aforementioned factors are expected to boost the demand for limestone during the forecast period.

North America Limestone Industry Overview

The North American limestone market is consolidated in nature. The major players (not in any particular order) include Carmeuse, Graymont Limited, Lhois, Mississippi Lime Company, and United States Lime & Minerals Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in the Construction Activities

- 4.1.2 Growing Use in Cement Production

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Environmental Concerns Related to Mining and Processing

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Industry Lime

- 5.1.2 Chemical Lime

- 5.1.3 Construction Lime

- 5.1.4 Refractory Lime

- 5.2 End-user Industry

- 5.2.1 Paper and Pulp

- 5.2.2 Water Treatment

- 5.2.3 Agriculture

- 5.2.4 Plastics

- 5.2.5 Building and Construction

- 5.2.6 Steel Manufacturing

- 5.2.7 Chemical

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Carmeuse

- 6.4.2 Graymont Limited

- 6.4.3 Imerys

- 6.4.4 Iowa Limestone Company

- 6.4.5 Lhois

- 6.4.6 Minerals Technologies Inc.

- 6.4.7 Mississippi Lime Company

- 6.4.8 Omya AG

- 6.4.9 The National Lime & Stone Company

- 6.4.10 United States Lime & Minerals Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements for Efficient Extraction and Processing

- 7.2 Other Opportunities