PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1429210

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1429210

Global Chemical Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

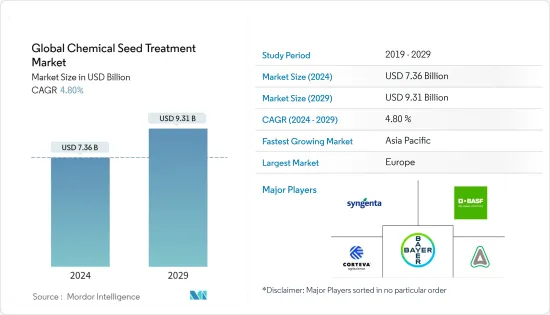

The Global Chemical Seed Treatment Market size is estimated at USD 7.36 billion in 2024, and is expected to reach USD 9.31 billion by 2029, growing at a CAGR of 4.80% during the forecast period (2024-2029).

The impact of the COVID-19 pandemic on the seed treatment market has been minimal, mainly due to transportation barriers. The impact of lockdowns or disruptions has been exempted by the government for all types of agricultural activities, hence there has been no such effect of corona outbreak. Indeed, the agrochemical companies have made double-digit profits as compared to last year, due to panic buying behavior from farmers. Growing awareness among farmers over the use of seed treatment has resulted in support from the government. Multiple seed banks are being managed by the governments of developing countries, at the national, as well as village levels, in order to store seeds that are properly treated by seed treatment chemicals, hence preventing the rotting of seeds. Encouraging government regulations and campaigns over the use of seed treatment is driving the market. The global market for seed treatment comprises chemical agents, including insecticides, fungicides, and other chemicals, of which chemical agents form the most dominant application segment.

Chemical Seed Treatment Market Trends

Increase in Cost of High-Quality Seeds driving the Market

High costs associated with hybrids and genetically modified seeds is a major factor driving the growth of the seed treatment market, globally. Seed treatment is gradually being considered by farmers as a mode to protect investments made on good quality seeds, due to an increase in regulatory issues relating to fumigation, as well as the foliar application of pesticides. Cost of seeds is expected to increase, owing to a increase in the demand for high-quality seeds, with desirable agronomic traits. Both companies and farmers are ready to spend on seed treatment solutions, in order to save high-quality seeds. According to USDA estimates of 2019, corn seeds cost about 300% since 1995, while the yield grew by only 35%. Framers are trying to cut down operating costs by selecting seeds that do not require multiple doses of chemicals. The initial protection of these engineered seeds is ensured by using seed treatments products.

Increasing Usage in the Asia Pacific region

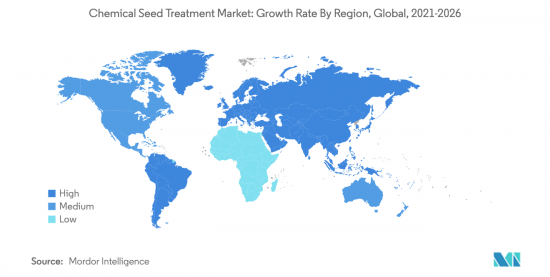

Geographically, Asia Pacific is the top consumer of seed treatment with a market share of around 60.0%. Major crops produced in Asia include rice, sugar beet, fruits & vegetables, cereals, and grains. Asian countries, such as Korea, China, Japan, and recently Vietnam, are applying more of seed protection/enhancement products for both short-term and perennial crops. Various leading seed treatment companies like Syngenta, BASF, and Bayer are operating in these regions and they regularly organize field trials and training sessions to increase the awareness regarding their products, as well as to present the benefits of using seed treatment products. The increasing agricultural practices and requirement of high-quality agricultural produce are factors that are projected to drive the seed treatment market growth in this region.

Chemical Seed Treatment Industry Overview

The market for chemical seed treatment is consolidated. Top players in the market occupy a major portion of the market, having a diverse and increasing product portfolio. In terms of market share dominance, Syngenta International AG with 24.0% share is followed by Bayer CropScience AG, Corteva Agriscience, BASF SE, and Syngenta. These major players in this market are focusing on increasing their presence through expansions & investments, mergers & acquisitions, partnerships, joint ventures, and agreements. These companies have a strong presence in North America, Asia Pacific, and Europe. They also have manufacturing facilities, along with strong distribution networks across these regions. The major players in this market are focusing on increasing their presence through expansions & product innovations, mergers & acquisitions, partnerships, joint ventures, and agreements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of Substitute Products

- 4.4.4 Threat of New Entrants

- 4.4.5 Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Insecticide

- 5.1.2 Fungicide

- 5.1.3 Other Chemicals

- 5.2 Crop

- 5.2.1 Corn/Maize

- 5.2.2 Soybean

- 5.2.3 Wheat

- 5.2.4 Rice

- 5.2.5 Canola

- 5.2.6 Cotton

- 5.3 Geography

- 5.3.1 North America

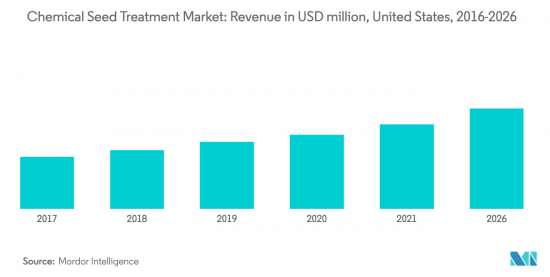

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Vietnam

- 5.3.3.6 Australia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta International AG

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 DowDuPont Inc.

- 6.3.5 ADAMA Agricultural Solutions Ltd

- 6.3.6 Advanced Biological Systems

- 6.3.7 BioWorks Inc.

- 6.3.8 Germains Seed Technology

- 6.3.9 Incotec Group BV

- 6.3.10 Nufarm Limited

- 6.3.11 Plant Health Care

- 6.3.12 Precision Laboratories

- 6.3.13 Valent Biosciences Corporation

- 6.3.14 Verdesian Life Sciences

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 AN ASSESSMENT OF IMPACT OF COVID-19 ON THE MARKET