PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690928

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690928

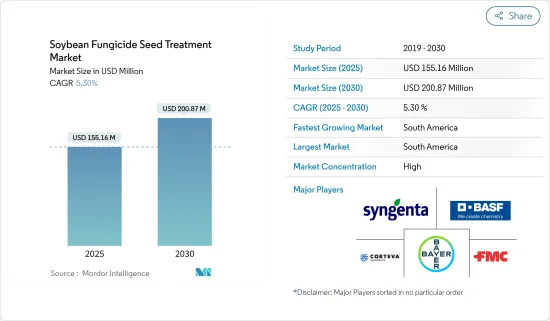

Soybean Fungicide Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Soybean Fungicide Seed Treatment Market size is estimated at USD 155.16 million in 2025, and is expected to reach USD 200.87 million by 2030, at a CAGR of 5.30% during the forecast period (2025-2030).

The soybean fungicide seed treatment market is growing as farmers focus on protecting crops against fungal diseases to maintain healthy yields. Soybeans face significant risks from soil- and seed-borne pathogens including Phytophthora, Rhizoctonia, and Fusarium, which affect germination and early plant development.

Global soybean consumption continues to rise across food, animal feed, and industrial sectors. Soybeans provide essential protein and oil for plant-based foods, including tofu, soy milk, and meat alternatives, which are increasing in popularity due to health and sustainability concerns. The livestock industry depends on soybean meal for feeding poultry, swine, and cattle. The global cattle population reached 1,575.7 million in 2023, up from 1,557.7 million previously. The biofuel industry also increases demand through soybean oil used in biodiesel production. Population growth and changing dietary preferences sustain this consumption growth further driving the soybean fungicide treatment market.

Advanced fungicide formulations provide enhanced protection against multiple pathogens. These treatments improve seedling vigor, ensure uniform growth, and strengthen environmental stress resistance. The industry is moving from traditional chemical applications to targeted seed treatments, focusing on maximizing crop productivity while reducing input costs and application complexity.

South America dominates the soybean fungicide seed treatment market, with Brazil and Argentina as major contributors due to extensive soybean production. North America, particularly the United States, represents a significant market share due to humid conditions that increase fungal infection risks. The Asia-Pacific market is expanding through increased soybean cultivation and seed treatment adoption, particularly in China and India. India's soybean imports increased to 724.9 thousand metric tons from 489.5 thousand metric tons, according to the ITC trade map. The market for soybean fungicide seed treatments is anticipated to expand during the forecast period, driven by increasing soybean demand.

Soybean Fungicide Seed Treatment Market Trends

Rapidating Demand for Biological Seed Treatment

Environmental concerns in developed regions are increasing the demand for biological seed treatments, driving market growth during the forecast period. Chemical companies are responding by expanding their biological seed treatment offerings. In the United States, major companies are providing soybean seeds treated with biological and chemical combinations. According to FAOSTAT, Canada's soybean harvested area increased from 2.11 million hectares in 2022 to 2.26 million hectares in 2023.

Biological seed treatments incorporate active ingredients such as living microbes, fermentation products, plant extracts, phytohormones, and chemical compounds to benefit plant development. These treatments are gaining popularity due to their ability to enhance plant growth, reduce stress, and increase yield by maximizing plant genetic potential.

The United States seed treatment market is expanding due to increased crop consumption and early soybean planting practices. FAOSTAT reports soybean production reached 113.3 million metric tons in 2023. Early planting in moist soils often exposes seeds and seedlings to insects, diseases, and pests, necessitating seed treatment for protection and yield improvement. The US Environmental Protection Agency (EPA) oversees chemical pesticide application on crops and food products, with numerous companies securing EPA registration in recent years.

Companies are increasingly entering the biological seed treatment market. In 2022, BASF SE registered Veltyma Fungicide for Canadian soybean farming. This product combines mefentrifluconazole (Revysol) with pyraclostrobin's plant health benefits and metconazole's Fusarium control capabilities to provide comprehensive soybean disease management.

South America Dominates the Market

South America dominates global soybean production and export, with Brazil and Argentina as major contributors. Brazil, the world's largest soybean producer, accounts for over 40% of global soybean output, while Argentina maintains its position among top exporters according to FAO. The region's extensive arable land, suitable climate, and modern farming practices enable large-scale production to meet global demand for soybeans in food, animal feed, and biofuels. According to FAOSTAT, soybean production increased from 121.2 million metric tons in 2022 to 152.1 million metric tons in 2023. Brazil's main soybean-producing states - Mato Grosso, Parana, and Rio Grande do Sul - constitute a significant portion of national output. Argentina's Pampas region serves as a primary soybean cultivation area, supported by established agricultural infrastructure.

South America controls the global soybean export market, with China as the primary importer. Brazil's soybean exports increased from 78.9 million metric tons in 2022 to 101.9 million metric tons in 2023, according to the ITC Trade map, supplying key markets in Asia, Europe, and North America. Argentina, despite lower production volumes than Brazil, specializes in exporting processed soybean products, including meal and oil. The region's port infrastructure, including Brazil's Santos Port and Argentina's Rosario Port, facilitates efficient global distribution. These exports support worldwide food security and livestock industries, particularly in regions with limited soybean production.

South America experiences increasing demand for bio seed treatment fungicides, driven by sustainable agriculture needs and environmental awareness. Soybean farmers combat fungal diseases including Phytophthora root rot, Fusarium wilt, and Rhizoctonia damping-off, which affect crop yields. The transition from conventional chemical fungicides to bio-based seed treatments continues due to their environmental benefits and positive effects on seed germination and early crop development. These biofungicides utilize natural microbes and plant extracts to control fungal pathogens while improving soil conditions, supporting global sustainability initiatives. South America maintains its market position through strong production and export capabilities, combined with increasing adoption of sustainable farming practices like bio seed treatment fungicides.

Soybean Fungicide Seed Treatment Industry Overview

The global market for soybean fungicide seed treatment is consolidated, with major players such as Syngenta Group, BASF SE, Bayer Crop Science AG, Corteva Agriscience, and FMC Corporation among others. Syngenta International AG occupies the largest market share, followed by BASF SE and Bayer Crop Science AG. Major players in the market have extended their product portfolio and taken the approach of expansion and partnerships to broaden their business and strengthen their position in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Soybean Fungal Diseases

- 4.2.2 Growing Demand for High-Quality Crop Yield

- 4.2.3 Government Support and Initiatives

- 4.3 Market Restraints

- 4.3.1 Adverse Effect of Chemical Seed Treatment Fungicides

- 4.3.2 Stringent Regulations on Agrochemicals

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Chemical

- 5.1.2 Non-Chemical/Biological

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 Italy

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Thailand

- 5.2.3.5 Vietnam

- 5.2.3.6 Australia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Rest of Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta Group

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 UPL

- 6.3.5 Corteva Agriscience

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 FMC Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS