Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690975

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690975

North America Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 211 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

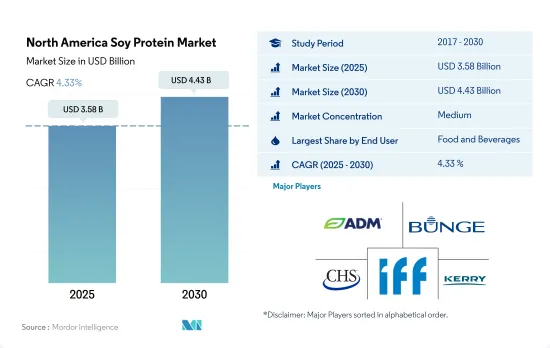

The North America Soy Protein Market size is estimated at 3.58 billion USD in 2025, and is expected to reach 4.43 billion USD by 2030, growing at a CAGR of 4.33% during the forecast period (2025-2030).

The F&B segment has major applications of soy protein due to the form's high nutritional properties

- In 2022, the food and beverages segment emerged as the top end user segment by value share. Within this segment, meat and its alternatives, particularly those utilizing soy proteins, commanded the highest share of 46%. Soy proteins, known for their versatility, are instrumental in creating meat-like textures such as chunks, shreds, and strips, enhancing the appeal of meat-free options. Notably, in 2021, a quarter of Americans turned to plant-based meat alternatives, citing health and environmental concerns, further fueling this sub-segment's growth.

- In the animal feed segment, soy proteins, predominantly in concentrate form, play a pivotal role. Their popularity stems from attributes like easy digestibility, extended shelf-life, and potent protein fortification. As a result, soy proteins have become the go-to protein source in the diets of various farm animals, from ruminants and pigs to poultry and aquaculture. This trend aligns with the region's increasing recognition of soy proteins' significance in animal feed. Projections indicate this end user segment will see a steady CAGR of 3.20% over the forecast period in the North American market.

- Supplements are poised for rapid growth, with a projected CAGR of 5.92% over the forecast period. This surge is fueled by a heightened interest in fitness among consumers, particularly in sports and performance nutrition. With a growing number of fitness enthusiasts and vegan gym-goers relying on proteins for muscle-building, the demand for supplements is on the rise. Female athletes, in particular, are turning to soy protein powder as an ergogenic aid, not only to boost performance but also to hasten muscle recovery, offering potential benefits in conditions like osteoporosis.

The United States holds a significant market share owing to favorable government initiatives

- In 2022, the United States led the North American soy protein market, buoyed by robust government initiatives and promotions aimed at bolstering soy protein consumption. The food and beverages segment, along with the animal feed segment, collectively commanded the largest share, with the former at 51.1% and the latter at 47.8%. Notably, the thriving poultry industry, a significant consumer of soy protein, played a pivotal role. For instance, per capita poultry consumption, encompassing broilers, other chickens, and turkeys, climbed from 107.6 pounds in 2016 to 113.4 pounds in 2021.

- Within the food and beverage landscape, meat, poultry, seafood, and their alternatives held a commanding 42.5% market share in 2022. Consumers, increasingly health-conscious, are pivoting toward products that promote well-being. This shift is largely attributed to a heightened awareness of the adverse effects of traditional meat consumption. Consequently, the demand for meat alternatives and analogs has surged in recent years.

- While the United States led the pack in 2022, Canada and Mexico followed suit. Mexico, although in its infancy in the soy protein market, shows promising growth prospects, especially given its burgeoning food and beverages segment. With a strong inclination toward traditional, often meat-centric, foods, Mexican manufacturers are innovating to replicate meat's properties, texture, flavor, and aroma. Consequently, the food and beverages segment of the Mexican soy protein market is poised to witness the swiftest CAGR of 5.40% during the forecast period.

North America Soy Protein Market Trends

Plant protein consumption growth fuels opportunities for key players in the ingredients industry

- From 2017 to 2022, the region saw a 2.42% increase in per capita plant protein consumption, driven by investments and innovations. This surge was primarily fueled by a growing number of consumers shifting toward vegan or vegetarian diets, largely motivated by concerns for animal welfare. Notably, in 2020, approximately 9.6 million more Americans adopted plant-based diets, constituting nearly 3% of the US population. After the COVID-19 pandemic, plant protein consumption surged, partly due to concerns over viral contamination in animal-sourced proteins and a general increase in protein blends, including both animal and plant sources.

- While most Americans are reducing their meat intake, they are not eliminating it, leaning more toward a flexitarian diet than strict veganism or vegetarianism. Plant proteins find significant usage in sports nutrition and as meat alternatives. Soy and whey proteins, in particular, are prevalent in food and beverage, supplements, and sports nutrition. By 2021, 36% of US consumers were familiar with and had consumed soy protein, with a slightly lower share of 31% having tried whey protein.

- Canada boasts the second-largest flexitarian population, showcasing a significant shift toward flexitarianism and veganism among consumers. This trend presents a ripe opportunity for manufacturers to further innovate in the plant protein market. In 2021, the Canadian government pledged over USD 4.3 million to bolster the country's pulse and special crop farmers, aligning with the rising consumer appetite for sustainable, high-quality plant-based proteins.

The United States produces more than 90% of all soybeans in North America

- The United States and Canada are the largest soybean producers in North America. The United States produces about one-third of the total soybeans globally, followed closely by Brazil and Argentina. In 2021, the country produced 119.88 million metric tons of soybeans, accounting for a 31% share of global soybean production. Soy, a globally traded commodity, thrives in temperate and tropical climates, serving as a vital source of protein and vegetable oils. Shifting food consumption patterns, a growing preference for vegetarian protein sources, and evolving food requirements are key drivers driving the US soy protein ingredients market.

- However, catering to domestic needs, the United States exported soybeans worth USD 27.94 billion in 2023. China, Europe, Mexico, Japan, and Indonesia emerged as primary destinations for US soybean exports. Farmers in the United States are embracing innovation and leveraging regenerative agriculture and biotechnology to meet domestic and international demands. The United Soybean Board collaborates with farmers, promoting best practices to enhance efficiency and bean quality.

- Canada, while being the third-largest producer of soybeans in North America, has seen soybeans gain prominence as a cash crop, particularly in regions like Quebec, Manitoba, the Maritimes, southeast Saskatchewan, and southern Alberta. Canada boasts 200 registered soybean varieties, with a significant 80% being herbicide-tolerant.

North America Soy Protein Industry Overview

The North America Soy Protein Market is moderately consolidated, with the top five companies occupying 54.20%. The major players in this market are Archer Daniels Midland Company, Bunge Limited, CHS Inc., International Flavors & Fragrances, Inc. and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90078

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 Canada

- 3.4.2 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Supplements

- 4.2.3.1 By Sub End User

- 4.2.3.1.1 Baby Food and Infant Formula

- 4.2.3.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.3.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.3.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 Bunge Limited

- 5.4.4 CHS Inc.

- 5.4.5 Farbest-Tallman Foods Corporation

- 5.4.6 Foodchem International Corporation

- 5.4.7 International Flavors & Fragrances, Inc.

- 5.4.8 Kerry Group PLC

- 5.4.9 The Scoular Company

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.