Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690992

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690992

Asia-Pacific Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 334 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

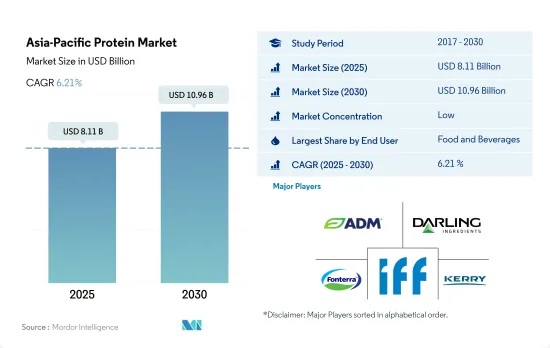

The Asia-Pacific Protein Market size is estimated at 8.11 billion USD in 2025, and is expected to reach 10.96 billion USD by 2030, growing at a CAGR of 6.21% during the forecast period (2025-2030).

Growing demand for animal-free products amid rising veganism is driving the food and beverage segment, resulting in the largest market share

- Food and beverage remained the largest protein-consuming segment in the region. Among others, bakery, dairy, and meat alternatives remained the major application areas, capturing a 39% volume share of the protein consumed in the region in 2023. Growing demand for animal-free products amid rising veganism attracted greater integration of plants, especially soy proteins, in dairy and meat imitation applications.

- The segment was followed by the animal feed segment, which relies on plant proteins for their cost-effective and nutritional attributes. Asia-Pacific is one of the major cattle-producing regions, especially countries like India and China, where the demand for quality-centric animal feed is growing, further benefitting the protein market in the region. For instance, currently, the number of cattle herds is 307.42 million heads, marginally up from 307.4 million heads in 2023. Soy protein is emerging as a high-quality feed ingredient for poultry, livestock, and aquaculture among retailers as it is highly digestible, making a good diet for cattle. Due to the significant share, the application of soy protein is set to record a major CAGR of 6.23% by volume during 2024-2029.

- Supplements hold a significant share in the protein market. The sports nutrition sub-segment mainly dominated the market, and it is projected to register a CAGR of 4.58% by value during 2024-2029. One of the key elements supporting the growth of the protein market is the expanding popularity of fitness and sports culture, along with the rising number of sports clubs and training facilities. In India, 54% of people frequently exercised in 2021, and 30% upgraded their fitness routines by utilizing cutting-edge applications and gadgets.

China leads the Asia-Pacific protein market due to the increasing demand for protein functionalities and rising awareness about protein-rich diets

- By country, China led the market in 2023, majorly driven by the food and beverage segment. The increasing demand for protein functionalities and awareness about protein-rich diets primarily drive protein demand in the food and beverage segment. In China, companies are making significant investments in rolling out innovative protein-based products in the retail space. For instance, Cargill, Hoafood, and Eat Just expanded their plant-based operations in China during 2019-2023. China is also anticipated to register the fastest growth in the region, with a CAGR of 7.09% by volume during 2024-2029.

- China was closely followed by India, driven by the emerging young population and their demand for high-protein meals. Initiatives such as India Protein Score (IPS) are further boosting protein-related awareness among consumers. The rise of various forms of plant-based protein powders and supplements, like soy, pea, and brown rice, contributes to this demand. The immense availability, functionality, vegan protein source, and low price of soy, wheat, and peas have contributed to the country's leading position in the plant protein segment. Hence, the Indian protein market observed a growth rate of 10.19% by value from 2019 to 2023.

- In Indonesia, plant-based fast food is gaining popularity, prompted by greater consumer awareness of health, sustainability, and animal welfare, with many food chains across the country adopting the vegan trend. Companies such as Starbucks, Ikea, and Burger King are launching vegan foods, thus boosting the demand for plant-based proteins in Indonesia. Hence, the plant protein segment in Indonesia is projected to register a CAGR of 3.29% by volume during 2024-2029.

Asia-Pacific Protein Market Trends

The share of whey and milk protein is expected to increase in animal protein consumption

- Consumers are opting for whey products due to sporting events that took place in the region, like the Olympic Tokyo Games in 2020 and the Rugby World Cup. The sports events and the growing older population in Japan are driving serum consumption as the main protein supplement in sports nutrition and elderly nutrition, respectively. The increasing awareness about the benefits of proteins among the Japanese military is also boosting the consumption of whey proteins. India is one of the fastest-growing countries in the world.

- Currently, the animal protein market in China is witnessing a steady development. With improved living standards in China, consumer safety requirements for food and drugs have improved. China has seen a decline in its pig herd of almost 40% due to the deficit created by African Swine Fever in the last two years and an increase in the importation of animal proteins during the past two years.

- Whey protein concentrates offer versatile benefits, including efficient and easy-to-digest processing and inexpensive applications, which are contributing to India's market growth. They have a wide range of applications in the sports nutrition category. Owing to the increased consumption of sports nutrition among young Indians, the demand for whey protein concentrate also increased. The per capita consumption of whey protein in the country increased to 17.2g in 2022 from 14g in 2017.

Milk and meat production majorly contributes as raw material for animal protein ingredient manufacturers

- India is the major milk-producing country in the region, followed by China. In 2021, India produced nearly 96 million tons of cow milk, while China produced around 35 million tons. Concentrated animal feeding operations (CAFOs) or factory farms for dairy production plants are being set up across Asia, many housing thousands of cows, by global and new national dairy corporations often working in partnership with governments. The strongest gains in milk production over the past decade have been registered in Southeast Asia.

- China's milk production in the region increased by 7.06% in 2021 due to improved productivity, as the COVID-19 disruption caused China's production and consumption of milk to grow rapidly. Imports are also showing positive growth due to consumer demand and requirements for the manufacturing industries in China. Skim milk powder, which is majorly used for milk protein production, has increased due to the Chinese food industry's dependence on imported skim milk powder.

- Animal protein from cattle, pigs, and chickens is used for collagen and gelatin production. Production is improving significantly in countries like India and China, and it is supported by government initiatives and the construction of new, modern slaughterhouses across the countries. Overall pig production declined in 2020 as African Swine Fever continued to impact China's hog industry.

Asia-Pacific Protein Industry Overview

The Asia-Pacific Protein Market is fragmented, with the top five companies occupying 13.91%. The major players in this market are Archer Daniels Midland Company, Darling Ingredients Inc., Fonterra Co-operative Group Limited, International Flavors & Fragrances, Inc. and Kerry Group plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90173

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 China

- 3.4.3 India

- 3.4.4 Japan

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 New Zealand

- 4.3.8 South Korea

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.3.11 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Corbion Biotech, Inc.

- 5.4.3 Darling Ingredients Inc.

- 5.4.4 Fonterra Co-operative Group Limited

- 5.4.5 Fuji Oil Group

- 5.4.6 Glanbia PLC

- 5.4.7 Hilmar Cheese Company, Inc.

- 5.4.8 International Flavors & Fragrances, Inc.

- 5.4.9 Kerry Group plc

- 5.4.10 Lacto Japan Co. Ltd.

- 5.4.11 Nagata Group Holdings Ltd

- 5.4.12 Nitta Gelatin Inc.

- 5.4.13 Nutrition Technologies Group

- 5.4.14 Tereos SCA

- 5.4.15 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.