PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644828

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644828

Global Servo Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

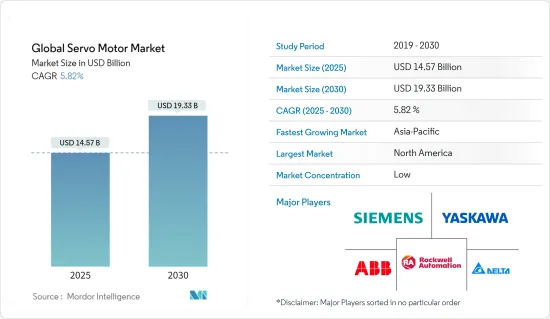

The Global Servo Motor Market size is estimated at USD 14.57 billion in 2025, and is expected to reach USD 19.33 billion by 2030, at a CAGR of 5.82% during the forecast period (2025-2030).

Recent technological advancements and government policies such as Minimum Energy Performance Standards (MEPS) in several countries have resulted in energy-efficient motor systems, which has increased the market for servo motors and drives.

Key Highlights

- The most advanced motion control devices are servo motors. It employs advanced design techniques, high-force magnet materials, and precise dimensional tolerance. Although not a specific type of motor, these electrical devices are designed and intended for motion control applications requiring high performance, quick reversing, and precise positioning. Furthermore, it is simple to install and requires no maintenance, further driving their demand over the forecast period.

- The primary factor driving the market is the use of servo motors for automation. Technological advancements in servo systems have increased end-user interest. These electrical devices are used in various industries, including automobile manufacturing, packaging machines, food processing, semiconductors, and healthcare.

- As of February 2021, Allied Motion Technologies introduced the H Series Brushless Servo Motor Drive, which includes Hiperface DSL, multi-feedback device support, and Safe Torque Off (STO) safety options. The H-Drive is part of Allied's new AMS servo packages and is designed to drive the HeiMotion brushless servo motors and Megaflux series of brushless torque motors.

- Further, at Automate 2022, Kollmorgen debuted the new TMB2G Robot-Ready Frameless Servo Motors. At the June 2022 breakout session, Kollmorgen also talked about improving Robot Efficiency Through Permanent Magnet Motor Design and Selection.

- Some significant drivers influencing the market growth are rapid growth and advancements in automation, and increasing adoption of international energy-efficient standards. Stringent electricity utilization standards, rising electricity prices, and the need to replace outdated low-efficiency electric motors with highly efficient servo motors are expected to drive demand for servo motors over the forecast period.

- Global industrial production was disrupted as a result of the COVID-19 pandemic. Steel is a common raw material used in servo motors. Several disruptions occurred in the steel industry and hampered servo motor production. Furthermore, China is a major steel producer. Every year, the country produces half of the world's steel. Steel production was hampered by factory closures and trade restrictions imposed by the Chinese government during the pandemic.

Servo Motor Market Trends

Increasing Automation Advancement

- The growing use of automation in manufacturing processes and the incorporation of digitization and AI are the primary factors driving demand for industrial robots in the automotive sector.

- Automakers, such as KUKA AG, have automated their plants in recent years to reduce the number of issues on the shop floor, improve efficiency, and lower operational costs. Many companies have followed suit, automating their plants to gain better returns and efficiency, thereby driving the servo motors and drives market.

- For instance, in June 2022, Aerobotix and Automated Solutions Australia officially announced an international robotic automation partnership for developing, testing, and manufacturing hypersonic missiles. The Aerobotix-ASA collaboration will make it easier for the Australian defense sector and defense contractors to access both companies' automation expertise.

- Servo motors are used in material handling, packaging, factory automation, machine tools, assembly lines, and other demanding applications such as robotics, CNC machinery, and automated manufacturing in the industrial sector. As a result, increased automation and robotics adoption is expected to drive the market for servo motors in the automotive sector over the forecast period.

North America to Hold Significant Share

- In North America, the United States is the largest industrial robot user in the Americas, accounting for 79% of total installations in the region. Mexico comes second with 9%, and Canada comes third with 7% (source: International Federation of Robotics).

- For Instance, in December 2021, According to the Association for Advancing Automation, factories and industrial concerns in North America ordered a record 29,000 robots in the first nine months of 2021, a 37 % increase over the previous year (A3).

- Servo motors demand accuracy and repeatability in a country where multiple manufacturing processes are becoming increasingly automated. Unlike hydraulic pumps or induction motors, Servo motors are switched on and off during operation to consume less power saving up to 65%.

- The servo solution is based on the most recent single-source, system-based design ideas. It uses Kollmorgen's AKD2G servo drive and AKM2G servo motor's performance capabilities. It avoids micro-incompatibilities when engineers select components from different manufacturers because the motor and drive are precisely matched in every element (e.g., drive switching frequency, commutation algorithms, and motor magnetics).

- Applied motion products increased MDX Integrated servo motor acceptance on the supplier front. The certification ensures that the motors meet high-quality electrical safety standards in the United States. The motors from Integrated were tested by the ANSI/UL standards 1004-1 Rotating Electrical Machines, 1004-6 Servo and Stepper Motors, and 61800-5-1 Adjustable Speed Drives. The certifications are listed as UL file number E472271.

Servo Motor Industry Overview

The market for servo motors is expected to be highly competitive over the forecast period, as market participants are increasingly focusing on new product development with a sharp focus on overcoming the processor's shortcomings. The players are also focusing on partnerships, mergers, and acquisitions to broaden their consumer base. Organizations such as ABB Ltd., Allied Motion Technologies, Inc., Ametek, Inc., General Electric Company, Nidec Corporation, Rockwell Automation Inc., Schneider Electric, Emerson Electric Company, Siemens AG, WEG Industries, Hitachi Ltd., Oriental Motor, Mitsubishi Electric Corp., Yaskawa Electric Corp. are the key performers in manufacturing servo motor globally.

- November 2021- Rockwell Automation, Inc. announced the expansion of its PowerFlex AC variable frequency drive portfolio to support a wider range of motor control applications. Customers will benefit from increased flexibility, performance, and intelligence in their next-generation drive thanks to TotalFORCE Technology.

- April 2021- By adding new servo motors, Siemens is expanding the range of applications for its Sinamics S210 single-cable servo drive system. The company is launching the Simotics S-1FS2, a motor version with a stainless-steel housing, the highest level of protection IP67/IP69, and high-resolution 22-bit absolute multiturn encoders for use in the pharmaceutical and food industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing the adoption of international energy-efficiency standards

- 5.1.2 Growing Automation Advancements

- 5.2 Market Challenges

- 5.2.1 Growing the availability of low-cost alternatives

6 SEGMENTATION

- 6.1 By Motor Type

- 6.1.1 AC Servo Motor

- 6.1.2 DC Servo Motor

- 6.2 By End-user Industry

- 6.2.1 Oil & Gas

- 6.2.2 Chemical & Petrochemical

- 6.2.3 Power Generation

- 6.2.4 Water & Wastewater

- 6.2.5 Metal & Mining

- 6.2.6 Food & Beverage

- 6.2.7 Discrete Industries

- 6.2.8 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Italy

- 6.3.2.4 France

- 6.3.2.5 Russia

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Australia & New Zealand

- 6.3.3.6 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Chile

- 6.3.4.4 Rest of Latin America

- 6.3.5 Middle-East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Turkey

- 6.3.5.4 Rest of Middle-East and Africa

- 6.3.1 North America

7 VENDOR MARKET SHARE

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Yaskawa Electric Corporation

- 8.1.2 ABB Ltd.

- 8.1.3 Siemens AG

- 8.1.4 Rockwell Automation, Inc.

- 8.1.5 Delta Electronics, Inc.

- 8.1.6 Maxon Precision Motors, Inc.

- 8.1.7 Mitsubishi Electric Corp.

- 8.1.8 FANUC Corp.

- 8.1.9 SANMOTION R.

- 8.1.10 Schneider Electric

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET