PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044244

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044244

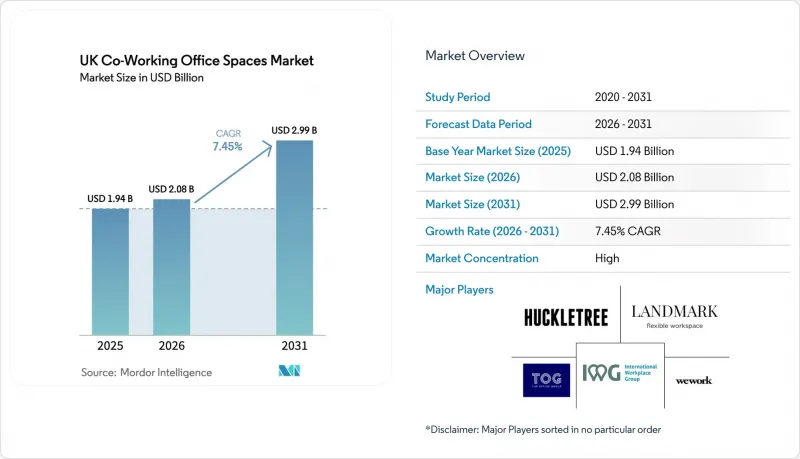

UK Co-Working Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The UK co-working spaces market size was valued at USD 1.94 billion in 2025 and estimated to grow from USD 2.08 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031).

Demand is being propelled by employers formalizing hybrid policies, which has shifted flexible workspace from a cyclical perk to a core component of real-estate strategy. Enterprises are renegotiating headquarters footprints while adding regional satellites, a move that enlarges the addressable pool for the UK co-working spaces market. ESG mandates are simultaneously pushing landlords to retrofit or develop BREEAM- and LEED-certified buildings, encouraging operators to prioritize certified assets where rent premiums reach 15-20%. Capital is abundant: family offices, infrastructure funds, and REITs are allocating dry powder to revenue-share agreements that shield operators from heavy fit-out costs and give landlords upside participation. Meanwhile, regional hubs such as Manchester and Belfast are closing the gap with London, signaling a durable geographic rebalancing that diversifies portfolio risk for providers active in the UK co-working spaces market.

UK Co-Working Office Spaces Market Trends and Insights

Hybrid-Work Penetration Sustaining Double-Digit Flexible-Space Absorption

Two-thirds of UK employers now require employees in the office at least part of the week, up sharply since 2023, and average office utilization hit 66% in 2025. Companies are therefore shifting from fixed leases toward variable-cost desks that can expand or contract with headcount. Technology giants have mainstreamed occupancy-sensor ecosystems that feed real-time data into scheduling tools, and operators able to plug into this stack are winning enterprise contracts. This uptake underpins stable, double-digit absorption across the UK co-working spaces market.

Technology, Creative & Professional-Services Tenants Extending Multi-City Footprints

Government grants for gaming, film, and digital media-totaling USD 480 million since 2024-are driving tenants to Manchester, Birmingham, and Leeds, where new innovation districts bundle studio space with co-working floors. Professional-services firms mirror this pattern, piloting nearshore delivery teams outside London to control salary costs, which enlarges the UK co-working spaces market beyond the capital.

Localized Oversupply in Central-London Sub-Markets Depressing Desk Rates

Inventory in the City and Westminster grew by more than 1 million sq ft between 2022-2024, yet utilization lingers below 70%. Average monthly desk rates reached USD 994 in early 2024, but landlords in fringe zones now offer rent-free periods and fit-out subsidies to fill space, straining margins for incumbent operators.

Other drivers and restraints analyzed in the detailed report include:

- Regional-Hub Demand Spike Narrowing London Dependence

- Shift Toward BREEAM/LEED-Certified Spaces to Meet Occupiers' ESG Mandates

- Elevated Energy, FM and Labor Costs Squeezing Operator EBITDA Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large campuses accounted for the fastest expansion path, registering a 9.11% CAGR outlook as of 2026-2031. Operators like Bruntwood SciTech and British Land are building 200,000 sq ft CL2-ready developments that compress fit-out timelines to eight weeks, making them magnets for biotech and AI drug-discovery ventures. Medium-scale hubs still hold the greatest slice at 43% of the UK co-working spaces market share, favored by enterprises distributing 5,000-20,000 sq ft footprints across multiple cities. Small neighborhood locations under 5,000 sq ft flourish in suburban London, absorbing work-from-near-home demand with minimal commute friction. Collectively, the trio of formats gives providers a diversified revenue mix that insulates them from cycle swings.

Demand heterogeneity requires operators to balance portfolio mix. Campuses can anchor multi-year agreements with anchor tenants, while medium hubs function as satellite nodes, and small sites satisfy freelancers. Groups that over-index on one scale risk occupancy shocks as tenant requirements evolve. Consequently, expansion blueprints in the UK co-working spaces market now bundle at least one asset in each scale tier to hedge against structural shifts.

The United Kingdom Co-Working Office Spaces Market Report is Segmented by Size & Scale of Facility (Small, Medium, Large), by Sector (IT & ITES, BFSI, Business Consulting & Professional Services, Other Services), by End Use (Freelancers, Enterprises, Start-Ups & Others), and by Geography (England, Scotland, Wales, Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- International Workplace Group plc (IWG)

- WeWork

- The Office Group

- Landmark

- Huckletree

- Labs

- Work Well Offices

- The Brew

- Jactin House

- Icon Offices

- Wimbletech CIC

- The Skiff

- Soho Works

- Creative Works

- The Hoxton

- Mare Street Market

- Southbank Centre

- Bruntwood Works

- Knotel UK

- Clockwise Offices

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid-work penetration sustaining double-digit flexible-space absorption

- 4.2.2 Technology, creative & professional-services tenants extending multi-city footprints

- 4.2.3 Regional-hub demand spike (Manchester, Birmingham, Leeds) narrowing London dependence

- 4.2.4 Shift toward BREEAM/LEED-certified spaces to meet occupiers' ESG mandates

- 4.2.5 Family-office & infrastructure-fund capital earmarked for income-resilient co-working portfolios

- 4.2.6 Landlord-operator revenue-share models lowering entry barriers for new sites

- 4.3 Market Restraints

- 4.3.1 Localized oversupply in Central-London sub-markets depressing desk rates

- 4.3.2 Elevated energy, FM and labour costs squeezing operator EBITDA margins

- 4.3.3 SME demand volatility amid UK inflation/recession fears

- 4.3.4 Upcoming non-traditional competition (hotel-lobby passes, retail pop-ups) eroding pricing power

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real-Estate Developers & Asset Owners - Key Quantitative and Qualitative Insights

- 4.4.3 Workspace Design & Technology Consultants - Key Quantitative and Qualitative Insights

- 4.4.4 Modular Furniture & Smart-Office Solution Providers - Key Quantitative and Qualitative Insights

- 4.5 Regulatory Landscape (Planning-use-class E, EPC-B 2030 mandate, business-rates reliefs)

- 4.6 Technological Outlook (prop-tech, IoT-enabled desk booking, AI space-optimisation)

- 4.7 Key Office-Real-Estate Metrics (Supply, Rentals, Prices, Occupancy/Vacancy %)

- 4.8 Impact of Remote Working on Space Demand

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Size & Scale of Facility

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.2 By Sector

- 5.2.1 IT & ITES

- 5.2.2 BFSI

- 5.2.3 Business Consulting & Professional Services

- 5.2.4 Other Services (Retail, Lifesciences, Energy, Legal)

- 5.3 By End Use

- 5.3.1 Freelancers

- 5.3.2 Enterprises

- 5.3.3 Start-ups & Others

- 5.4 By Country

- 5.4.1 England

- 5.4.1.1 London

- 5.4.1.2 Rest of England

- 5.4.2 Scotland

- 5.4.3 Wales

- 5.4.4 Northern Ireland

- 5.4.1 England

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles {(includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.3.1 International Workplace Group plc (IWG)

- 6.3.2 WeWork

- 6.3.3 The Office Group

- 6.3.4 Landmark

- 6.3.5 Huckletree

- 6.3.6 Labs

- 6.3.7 Work Well Offices

- 6.3.8 The Brew

- 6.3.9 Jactin House

- 6.3.10 Icon Offices

- 6.3.11 Wimbletech CIC

- 6.3.12 The Skiff

- 6.3.13 Soho Works

- 6.3.14 Creative Works

- 6.3.15 The Hoxton

- 6.3.16 Mare Street Market

- 6.3.17 Southbank Centre

- 6.3.18 Bruntwood Works

- 6.3.19 Knotel UK

- 6.3.20 Clockwise Offices

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment