PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431296

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431296

Europe HVAC Field Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

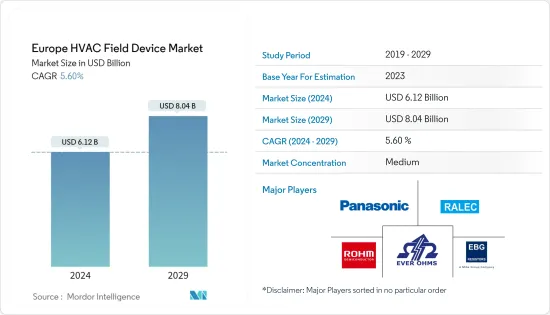

The Europe HVAC Field Device Market size is estimated at USD 6.12 billion in 2024, and is expected to reach USD 8.04 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

Key Highlights

- .Over the past few years, the market for HVAC field devices has undergone a period of transition due to new technology, regulations, changes in climatic conditions, and consumer trends. The region's emphasis on user-friendly and modern HVAC appliances has witnessed newfound demand.

- Government regulations regarding energy efficiency and eco-friendly refrigerants are expected to increase the need for HVAC field devices in the European regions, particularly in the United Kingdom, Germany, and France.

- In Germany, the government actively promotes the fast development and integration of renewable and efficient heating and cooling technologies through new laws and attractive incentives. This promotion has led to a significant market shift in Germany, with the heating and cooling industry growing partly due to this. The number of renewable and efficient technologies (such as CHP, solar thermal, heat pumps, condensing heating boilers, and pellet heating systems) has grown enormously.

- Moreover, the government's measures to create a climate-neutral building stock by 2050 are insufficient; the country's German Housing Association (GdW) and the CDU Economic Council are looking to shift to central heating. Such developments will severely impact the heating equipment market over the coming years.

- Retrofitting older buildings with air conditioning is significantly more difficult, especially if there is insufficient space to install ductwork. For buildings with space, the expense of these updates can be a bit high for end-users. The workaround on both ends is to use ductless cooling and heating units.

- Increasing construction activities and supportive government regulations for energy-saving solutions are expected to boost market growth.

Europe HVAC Field Device Market Trends

Residential Sector to have the Major Market Share

- Residential HVAC systems have become a necessity with extreme weather changes globally. Residential HVAC units are pieces of equipment that are installed in homes to maintain an indoor temperature.

- Residential HVAC systems consist of two separate units, including the indoor evaporator and the outer compressor. The three main functions of a residential HVAC system are ventilation, heating, and air conditioning. The ventilation functions can either be natural or forced; the heating component is carried out via a boiler or furnace; and the air conditioning function works to cool or maintain a lower room temperature by removing existing heat from the inside of the home.

- Various types of residential heating and cooling products include furnaces, air conditioners, heat pumps, air handlers, ductless systems, and thermostats, among others.

- Europe's summer heat waves are pushing demand for air conditioners in the region. Heatwaves are common in the European region, with summer temperatures reaching up to 45 Celsius, and demand for residential air conditioners has increased in the region.

- Further, urbanization, new building construction, and an increase in disposable income are the other key factors contributing to the rapid growth of the HVAC market in the European region.

United Kingdom is Expected to Hold the Major Market Share

- The increase in replacing existing equipment with better-performing ones and supportive government regulations, including incentives for saving energy through tax credit programs, are driving the United Kingdom HVAC market over the forecast period. For instance, the government of the UK has already set a target of installing 600,000 heat pumps per year by 2028 to reduce the UK's reliance on fossil fuels and help fight global warming. Such trends are expected to create demand for HVAC field devices over the forecast period.

- The government of the United Kingdom recently announced plans to stop installing home heating that uses fossil fuels by 2035. The government hosted a meeting to attract billions of dollars in foreign investment for green projects in the country. The Prime Minister of the country told the Global Investment Summit that private-sector investment and consumer pressure were vital to slashing carbon emissions and controlling climate change.

- The UK Government is presently offering contributions to the initial capital outlay on heat pumps, with GBP 5,000 (USD 6311.62) of the cost and installation of an air-source heat pump and GBP 6,000 (USD 7573.95) for ground-source heat pumps. However, the initial installation costs of an electric heat pump are still an off-putting hurdle for many potential users in the country.

- Nonetheless, ahead of the boiler upgrade scheme that took place on April 1, 2022, new polling for the Energy & Climate Intelligence Unit (ECIU) found that a third (33%) of British say they would be more likely to get an electric heat pump to help insulate themselves from Russia interfering in the gas market.

- Vendors need to comply with various regulations set by the government regarding environmental protection, as the coolants and other substances used in HVAC equipment contribute to global emissions. R-32 was chosen for its lower environmental impact, high energy efficiency, wide availability, and ease of use.

Europe HVAC Field Device Industry Overview

The Europe HVAC field device Market is moderately competitive due to the presence of many key players established within national and international boundaries. The market appears to be moderately concentrated, with the key players adopting strategies like product innovation and merger and acquisition.

In March 2023, Carel, an Italy-based manufacturer, launched its E5V electronic expansion valve for CO2 (R744)-based HVAC&R systems at the EuroShop trade show in Germany. The new expansion valve is suitable for high-capacity chillers, air-conditioning systems, and heat pumps up to 700kW (199TR).

In October 2022, Guangzhou Sprsun New Energy Technology Development Co., Ltd., a China-based heat pump provider, developed a monobloc heat pump that was reportedly easier and faster to install. The product featured a 3 kW/220 V electric heater, a water pump, an expansion tank measuring 5 liters, a three-way valve, and an 18 A AC contactor. The company is expected to target the European market to boost sales of its heat pump kit for residential applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Development of the Construction Market

- 5.1.2 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.3 The Emergence of IoT and Product Innovations to Aid Replacements

- 5.2 Market Restraints

- 5.2.1 Dependence on Macro-economic Conditions

- 5.2.2 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Control Valve

- 6.1.2 Balancing Valve

- 6.1.3 PICV

- 6.1.4 Damper HVAC

- 6.1.5 Damper Actuator HVAC

- 6.2 By Sensors

- 6.2.1 Environmental Sensors

- 6.2.2 Multi Sensors

- 6.2.3 Air Quality Sensors

- 6.2.4 Occupancy and Lighting

- 6.3 By End-user Industry

- 6.3.1 Commercial

- 6.3.2 Residential

- 6.3.3 Industrial

- 6.4 By Country

- 6.4.1 United Kingdom

- 6.4.2 Germany

- 6.4.3 France

- 6.4.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Elektronische Bauelemente GmbH (EBG)

- 7.1.2 Ever Ohms Technology Co., Ltd.

- 7.1.3 Panasonic Corporation

- 7.1.4 Ralec Electronics Corporation

- 7.1.5 Rohm Co., Ltd.

- 7.1.6 Samsung Electro-Mechanics

- 7.1.7 Ta-I Technology Co., Ltd.

- 7.1.8 Tateyama Kagaku Industry Co., Ltd.

- 7.1.9 Uniohm Corporation

- 7.1.10 Walsin Technology Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET