Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693855

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693855

Dairy Desserts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 367 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

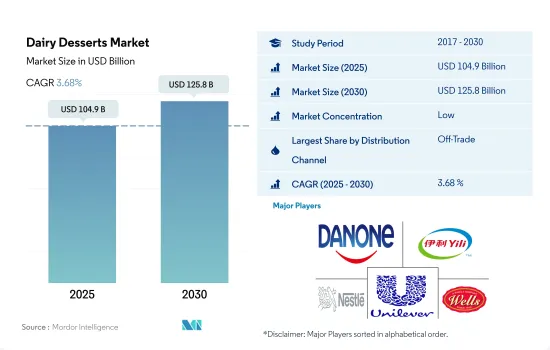

The Dairy Desserts Market size is estimated at 104.9 billion USD in 2025, and is expected to reach 125.8 billion USD by 2030, growing at a CAGR of 3.68% during the forecast period (2025-2030).

The sales through off-trade distribution channels with the presence of wider product range is making the market

- The off-trade segment dominates among distribution channels of the global dairy desserts market. In the off-trade segment, consumers prefer buying dairy desserts majorly from supermarkets and hypermarkets, as this channel often offers competitive prices on dairy desserts, especially when compared to specialty stores or boutique shops. This is because these outlets can purchase dairy desserts in bulk and pass on the savings to consumers. Hypermarkets and supermarkets usually offer a wide range of brands and products of dairy desserts, giving consumers a variety of options to choose from. This allows consumers to compare different brands and products and make informed purchasing decisions.

- Convenience stores account for the second highest share in the sales of dairy desserts, after supermarkets and hypermarkets. In 2022, the sales value of dairy desserts through convenience stores increased by 3.5% over the previous year.

- Dairy desserts are commonly offered through restaurants and food service channels. Foodservice channels offer various dairy desserts, including unique and customized options, which attract customers looking for something different or personalized. The sale of dairy desserts in restaurants and other food service channels is driven by various factors, including menu offerings, variety and customization, convenience and speed, quality and freshness, and presentation and atmosphere. Dairy dessert sales through the on-trade channel are anticipated to grow by 11.4% in 2025 compared to 2022. About 47% of consumers across the globe consumed meals at restaurants, and 31% of consumers ordered from foodservice channels in 2022.

The demand from Europe followed by North America and Asia-Pacific drives the global market

- The Y-o-Y growth rate of the global dairy desserts market was 4.1% in 2022 compared to the previous year. Of all the regions, Europe accounted for most of the share of the global dairy desserts market, i.e., 40.4%. Dairy desserts have gained immense traction across the region due to their various health benefits, easy accessibility, and the availability of premium ice creams.

- Ice cream accounts for most of the sales of dairy desserts in Europe. In 2021, the European Union produced over 3.1 billion liters of ice cream, a 4% increase compared to the previous year. Germany, the United Kingdom, and Italy are the key markets for dairy desserts in Europe, collectively accounting for 41.01% of the overall ice cream consumption in the region.

- North America is the second-largest market for dairy desserts. The sales value of dairy desserts in North America registered a growth rate of 6% from 2019 to 2022. The dairy desserts market in North American countries is expanding due to strong demand for ice cream. The average American consumes approximately 23 pounds of ice cream and other frozen desserts per year. About 73% of people consume ice cream at least once per week, and 2 out of 3 consume ice cream in the evening.

- Asia-Pacific is the fastest-growing region in terms of the sales of dairy desserts globally. The sales value of dairy desserts in Asia-Pacific is anticipated to grow by 12.1% in 2025 compared to 2022. New Zealand leads the world in ice cream consumption, with a per capita consumption of 28.4 liters per year. Increasing demand for sweet treats and increased income are the major factors driving the dairy desserts market in the region.

Global Dairy Desserts Market Trends

The consumption of dairy desserts is boosted by factors such as growing consumer expenditure on food and beverage, the introduction of new flavors, and increasing impulse purchasing

- Dairy dessert is the second most consumed dairy product globally after milk. The industry accounted for a 14.74% share of the overall dairy product consumption in 2022. The rising demand for innovative flavors and formats, supported by the increasing demand to consume such products worldwide, is driving the demand.

- Frozen desserts in the United States observed a Y-o-Y growth of 2% in 2022. Developed markets like the United States, the United Kingdom, Germany, and Australia, have witnessed rising health concerns among the population. As a result, consumers across the region increasingly prefer ice cream products that are GMO-free, preservative-free, dairy-free, low in calories, and organic and fat-free in nature.

- The ice cream market in Asia is growing, with brands tapping into this trend to cater to indulgence and health preferences. For example, the per capita consumption of ice cream in India grew by 5.90% during 2023-2024. Growing consumer expenditure on food and beverage, the introduction of new flavors, increasing impulse purchasing, and strong demand for healthy ice cream products among consumers are some of the primary factors driving the consumption of ice cream. About 75% of consumers in the region often or even sometimes try new or different varieties while purchasing ice cream products.

- The increased consumer preference for gelato is one of the major factors driving its consumption in European countries. Due to the consumer demand for new and innovative flavors, there has been a rise in the preference for gelato in recent years. Gelato is considered a healthy dessert for a variety of reasons and is highly popular in countries like Italy, Germany, and Spain.

Dairy Desserts Industry Overview

The Dairy Desserts Market is fragmented, with the top five companies occupying 25.48%. The major players in this market are Danone SA, Inner Mongolia Yili Industrial Group Co. Ltd, Nestle SA, Unilever Plc and Wells Enterprises Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 5000330

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Milk

- 4.3 Regulatory Framework

- 4.3.1 Belgium

- 4.3.2 Canada

- 4.3.3 China

- 4.3.4 Mexico

- 4.3.5 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Cheesecakes

- 5.1.2 Frozen Desserts

- 5.1.3 Ice Cream

- 5.1.4 Mousses

- 5.1.5 Others

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Product Type

- 5.3.1.2 By Distribution Channel

- 5.3.1.3 Egypt

- 5.3.1.4 Nigeria

- 5.3.1.5 South Africa

- 5.3.1.6 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Product Type

- 5.3.2.2 By Distribution Channel

- 5.3.2.3 Australia

- 5.3.2.4 China

- 5.3.2.5 India

- 5.3.2.6 Indonesia

- 5.3.2.7 Japan

- 5.3.2.8 Malaysia

- 5.3.2.9 New Zealand

- 5.3.2.10 Pakistan

- 5.3.2.11 South Korea

- 5.3.2.12 Rest of Asia Pacific

- 5.3.3 Europe

- 5.3.3.1 By Product Type

- 5.3.3.2 By Distribution Channel

- 5.3.3.3 Belgium

- 5.3.3.4 France

- 5.3.3.5 Germany

- 5.3.3.6 Italy

- 5.3.3.7 Netherlands

- 5.3.3.8 Russia

- 5.3.3.9 Spain

- 5.3.3.10 Turkey

- 5.3.3.11 United Kingdom

- 5.3.3.12 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Product Type

- 5.3.4.2 By Distribution Channel

- 5.3.4.3 Bahrain

- 5.3.4.4 Iran

- 5.3.4.5 Kuwait

- 5.3.4.6 Oman

- 5.3.4.7 Qatar

- 5.3.4.8 Saudi Arabia

- 5.3.4.9 United Arab Emirates

- 5.3.4.10 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Product Type

- 5.3.5.2 By Distribution Channel

- 5.3.5.3 Canada

- 5.3.5.4 Mexico

- 5.3.5.5 United States

- 5.3.5.6 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Product Type

- 5.3.6.2 By Distribution Channel

- 5.3.6.3 Argentina

- 5.3.6.4 Brazil

- 5.3.6.5 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Cedar Crest Specialties Inc.

- 6.4.2 Danone SA

- 6.4.3 Groupe Lactalis

- 6.4.4 Gujarat Co-operative Milk Marketing Federation Ltd

- 6.4.5 HP Hood LLC

- 6.4.6 Inner Mongolia Yili Industrial Group Co. Ltd

- 6.4.7 Mother Dairy Fruit & Vegetable Pvt. Ltd

- 6.4.8 Nestle SA

- 6.4.9 Unilever Plc

- 6.4.10 Wells Enterprises Inc.

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.