Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693885

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693885

Oat Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 330 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

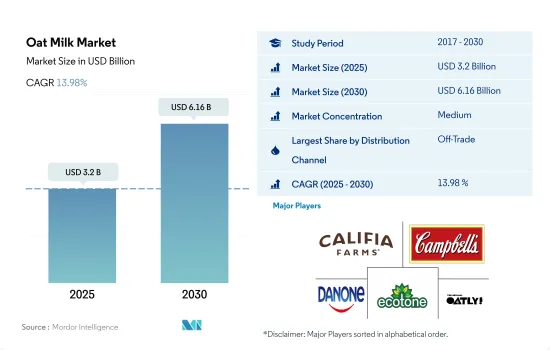

The Oat Milk Market size is estimated at 3.2 billion USD in 2025, and is expected to reach 6.16 billion USD by 2030, growing at a CAGR of 13.98% during the forecast period (2025-2030).

The sales through off-trade distribution channels with the presence of wider product range is making the market

- Among distribution channels, the off-trade channel plays a major role in the sales of oat milk globally. Supermarkets and hypermarkets accounted for most oat milk sales among the off-trade channels. In 2022, supermarkets and hypermarkets accounted for 66% of the value share. These retail chains offer an inviting place for consumers to shop, allowing them to choose from several plant-based milk options provided by various companies, depending on their needs.

- With the growing vegan population and lactose-intolerant consumers, demand for oat milk from the on-trade channel, especially fast-food restaurants and coffee chains, is expected to increase. Top coffee chains, such as Starbucks, Costa Coffee, and Caffe Nero, offer oat milk to consumers. As of 2021, in the United States, restaurants and cafes included oat milk in their menus, a 50% increase compared to 2020. The trend also surged in Canada and increased by 300%.

- The online channel is expected to be the fastest-growing retail channel for oat milk sales. The sales value of oat milk is anticipated to grow by 54.5% in 2025 compared to 2022. As a part of strategic expansion, leading brands of oat milk are teaming up with online retailers to increase their sales. In 2021, Earth's Own partnered with Amazon.ca, and in the same year, Plant Veda Foods Ltd completed an agreement with UniUni.com to sell a range of oat milk flavors to consumers. The major brand, Oatly, partnered with Netalico, a hands-on, merchant-focused e-commerce development agency that collaborates with merchants to build, optimize, maintain, and grow their online stores.

Europe holds prominent share in the consumption of oat milk across globe

- The global oat milk market observed growth of 2.83% in 2022 compared to 2021. The increase was attributed to the rising number of health-conscious consumers across the world. In 2022, the per capita consumption of oat milk was 1.28 kg. Some of the most preferred brands of oat milk are Oatly, Minor Figures, Alpro, and Califia Farms.

- In the Asia-Pacific region, oat milk is majorly used for various purposes. In 2022, consumers preferred oat milk as a substitute for animal-based milk in the region. In the Asia-Pacific region, Australia is considered the fastest-growing country for oat milk. In Australia, 30% of the population was diagnosed with irritable bowel syndrome (IBS) in 2022. Oats are a great source of soluble fiber, and oat milk has fiber that relieves IBS and constipation.

- In the North American region, oat milk is used as a healthy beverage among the population. It is majorly preferred by health-conscious consumers. Since oat milk has lower fat content than animal-based milk, it is consumed by the population following a calorie deficit diet. To mitigate the effects of lactose intolerance, most consumers are majorly drinking oat milk as a replacement for animal milk. The per capita consumption of non-dairy milk in the region was 3.23 kg in 2022.

- During the forecast period (2025-2029), with the growing focus on the benefits of oat-based milk, its demand is expected to rise. In addition, consumers are more likely to prefer innovative flavors in the oat milk segment.

Global Oat Milk Market Trends

The increasing prevalence of milk allergies, growing lactose-intolerant population, and consumer preference for sustainable, low-fat, and allergen-free options drive the consumption of oat milk

- Plant-based milk is the largest consumed category among all dairy alternatives globally. Oat milk, followed by soy milk, is highly popular and accounted for more than a 50% share of the overall plant-based milk consumption in 2022. The increasing prevalence of milk allergies is driving the demand for plant-based milk globally. For example, oat milk is a rich source of vitamins, proteins, and potassium and has a lower calorie content than cow's milk. Due to its high nutrient content, it is considered an ideal substitute for dairy products.

- One of the highest obesity rates in the world is held by the United States. As of November 2021, the adult obesity prevalence in the United States was 30% or higher, with 19 states having 35% or higher obesity prevalence. The growing volume of lactose-intolerant consumers in the country is another important aspect boosting the market's growth. In 2022, 30-50 million US consumers were found to be lactose-intolerant. People are exploring ways to stay fit and opt for healthy lifestyles to counter these aspects. Oat milk is the second most consumed type of plant milk by people trying to lose weight or suffering from lactose intolerance.

- There is a constant rise in the per capita consumption of oat milk due to consumer preference toward sustainable ingredient sourcing, which is concerned with hormones (plant estrogen or isoflavones) also found in soy milk. Oat milk also comes with GMO-free, low-fat, and allergen-free claims, giving consumers more plant-based options to diversify their diets. The global per capita consumption of oat milk is expected to increase by 11.24% from 2023 to 2024.

Oat Milk Industry Overview

The Oat Milk Market is moderately consolidated, with the top five companies occupying 44.46%. The major players in this market are Califia Farms LLC, Campbell Soup Company, Danone SA, Ecotone and Oatly Group AB (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50000756

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Oats

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Canada

- 4.3.3 China

- 4.3.4 India

- 4.3.5 Japan

- 4.3.6 Mexico

- 4.3.7 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Distribution Channel

- 5.1.1 Off-Trade

- 5.1.1.1 Convenience Stores

- 5.1.1.2 Online Retail

- 5.1.1.3 Specialist Retailers

- 5.1.1.4 Supermarkets and Hypermarkets

- 5.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.1.2 On-Trade

- 5.1.1 Off-Trade

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Distribution Channel

- 5.2.1.2 Egypt

- 5.2.1.3 Nigeria

- 5.2.1.4 South Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Distribution Channel

- 5.2.2.2 Australia

- 5.2.2.3 China

- 5.2.2.4 India

- 5.2.2.5 Indonesia

- 5.2.2.6 Japan

- 5.2.2.7 Malaysia

- 5.2.2.8 New Zealand

- 5.2.2.9 Pakistan

- 5.2.2.10 South Korea

- 5.2.2.11 Rest of Asia Pacific

- 5.2.3 Europe

- 5.2.3.1 By Distribution Channel

- 5.2.3.2 Belgium

- 5.2.3.3 France

- 5.2.3.4 Germany

- 5.2.3.5 Italy

- 5.2.3.6 Netherlands

- 5.2.3.7 Russia

- 5.2.3.8 Spain

- 5.2.3.9 Turkey

- 5.2.3.10 United Kingdom

- 5.2.3.11 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Distribution Channel

- 5.2.4.2 Bahrain

- 5.2.4.3 Kuwait

- 5.2.4.4 Oman

- 5.2.4.5 Saudi Arabia

- 5.2.4.6 United Arab Emirates

- 5.2.4.7 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Distribution Channel

- 5.2.5.2 Canada

- 5.2.5.3 Mexico

- 5.2.5.4 United States

- 5.2.5.5 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Distribution Channel

- 5.2.6.2 Argentina

- 5.2.6.3 Brazil

- 5.2.6.4 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Agrifoods International Cooperative Ltd

- 6.4.2 Betterbody Foods & Nutrition LLC

- 6.4.3 Califia Farms LLC

- 6.4.4 Campbell Soup Company

- 6.4.5 Danone SA

- 6.4.6 Ecotone

- 6.4.7 Elmhurst Milked LLC

- 6.4.8 Green Grass Foods Inc. (Nutpods)

- 6.4.9 Oatly Group AB

- 6.4.10 Ripple Foods PBC

- 6.4.11 SunOpta Inc.

- 6.4.12 The Hain Celestial Group Inc.

- 6.4.13 The Rise Brewing Co.

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.