Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693942

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693942

Large Satellites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 193 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

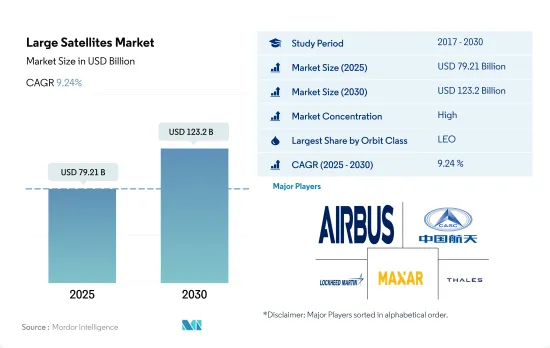

The Large Satellites Market size is estimated at 79.21 billion USD in 2025, and is expected to reach 123.2 billion USD by 2030, growing at a CAGR of 9.24% during the forecast period (2025-2030).

LEO segment leads the market's growth with a market share of 57.9% in 2029

- Over the past decade, large satellites have been launched in GEO. GEO occupied a market share of 79.8% in 2017. These satellites cost more, and their life span is on a higher side. Manufacturers spent large amounts of money to launch and deploy these satellites. However, with the advancements in technology, the cost of launching and developing satellites has been reduced over the past 3 to 4 years. Because of this, the viability of manufacturers to launch a large satellite in LEO also increased at a much larger pace.

- Depending on the type of application or mission, a particular satellite or entire satellite constellation is launched in different types of orbit. Different satellites manufactured and launched across all the regions have different applications. For instance, during 2017-2022, out of the 214 large satellites launched, 123, 71, 13, and 7 were placed in GEO, LEO, MEO, and elliptical orbits.

- With respect to the market shares, LEO is expected to lead the segment; it occupies a share of 50.5% in 2023, which is expected to reach 57.1% by 2029. The high market share is because of its proximity and several other advantages triggered by technological developments. GEO has a share of 44.3% in 2023 and is expected to occupy 36.9% in 2029.

- Therefore, the increasing use of satellites in electronic intelligence, Earth science/meteorology, laser imaging, optical imaging, and meteorology departments is expected to drive the demand for the development of satellites during the forecast period.

The increasing number of satellites with long lifespans helps the Asia-Pacific region maintain a substantial market share

- Large satellites are used for a wide range of applications, including communication, navigation, and Earth observation. As the demand for these applications continues to increase, companies are investing in R&D to develop large satellites to meet these needs.

- Large satellites are designed primarily for operational purposes with a long lifespan (between five and 10 years). These satellites are mainly used to carry larger remote sensing payloads or larger numbers of transponders and larger antennas for communication purposes. These operational satellites have redundancy for all major subsystems to support accidental failures in subsystems and extend lifespan. Larger satellites are typically built with radiation-hardened space-grade electronics. They generate more power with larger deployable solar panels to support all subsystems and larger loads. Since large satellites have large solar panels and bodies, they face greater atmospheric drag, generating the need for high-powered propulsion systems. Large satellites generally carry a chemical propulsion system for orbital elevation and attitude correction.

- During 2017-2022, around 200+ large satellites launched were owned by North American organizations and had applications such as electronic intelligence, Earth science/meteorology, laser imaging, electronic intelligence, optical imaging, and meteorology. Asia-Pacific is expected to dominate the market during the forecast period, with a share of more than 60%.

Global Large Satellites Market Trends

Trend for better fuel and operational efficiency has been witnessed

- The mass of a satellite has a significant impact on the launch of the satellite. This is because the heavier the satellite, the more fuel and energy are required to launch it into space. The launch of a satellite involves accelerating it to a very high speed, typically around 28,000 kilometers per hour, in order to place it in orbit around the Earth. The amount of energy required to achieve this speed is proportional to the mass of the satellite.

- Galaxy 33 and Galaxy 34, local communications satellites developed by Intelsat, were launched in October 2022 in the United States. These were among the world's most notable development and launches of satellites. Similarly, in March 2022, a Geostationary Active Environmental Satellite was launched by Lockheed Martin, which is an advanced weather satellite. In Europe, satellite I-6 F2 is planned to be launched in 2023.

- As a result, a heavier satellite requires a larger rocket and more fuel to launch it into space. This, in turn, increases the cost of the launch and can also limit the types of launch vehicles that can be used. The major classification types according to mass are large satellites that are more than 1,000 kg. These large satellites are majorly designed for operational purposes with a long lifespan. These satellites are being adopted by various countries to carry larger remote sensing payloads, larger numbers of transponders, and larger antennas for communication purposes. These operational satellites have redundancy for all major subsystems to support accidental failures in subsystems. Larger satellites are typically built with radiation-hardened space-grade electronics. During the period 2017-2022, around 200+ large satellites were manufactured and launched globally.

Increasing space expenditures of different space agencies globally is expected to positively impact the large satellites category

- R&D expenditure on large satellites is an important factor in driving innovation and technology development in the satellite industry. In recent years, the global trend in R&D expenditure on large satellites continues to rise, owing to several factors, including rapid advancements in satellite technology, new materials, propulsion systems, and electronics, which are driving the need for R&D investment to design and develop large satellites that can take advantage of these innovations.

- Large satellites are used for a wide range of applications, including communication, navigation, and Earth observation. As the demand for these applications continues to grow, companies are investing in R&D to develop large satellites that can meet these needs. Currently, in the Asia-Pacific region, China, India, and Japan possess a complete end-to-end space capacity and space infrastructure, space technology (communication, Earth observation (EO), and navigation satellites), satellite manufacturing, rockets, and spaceports. Other countries in the region are required to rely on international cooperation to carry out their respective space programs. In June 2022, the Nuri rocket was launched by South Korea, putting six satellites into orbit, making it the seventh country in the world to successfully launch a payload weighing more than one ton onto an air launch vehicle.

- The South Korean government, in its 2022 budget, announced an investment of USD 619 million in the space segment, which includes the development of a spaceport, the construction of a satellite navigation system, and a 6G communications network. The spending on space and research grants is expected to surge in the region, thereby increasing the sector's importance in every domain of the global economy..

Large Satellites Industry Overview

The Large Satellites Market is fairly consolidated, with the top five companies occupying 82.66%. The major players in this market are Airbus SE, China Aerospace Science and Technology Corporation (CASC), Lockheed Martin Corporation, Maxar Technologies Inc. and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001254

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Global

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 France

- 4.3.7 Germany

- 4.3.8 India

- 4.3.9 Iran

- 4.3.10 Japan

- 4.3.11 New Zealand

- 4.3.12 Russia

- 4.3.13 Singapore

- 4.3.14 South Korea

- 4.3.15 United Arab Emirates

- 4.3.16 United Kingdom

- 4.3.17 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 China Aerospace Science and Technology Corporation (CASC)

- 6.4.3 Indian Space Research Organisation (ISRO)

- 6.4.4 Information Satellite Systems Reshetnev

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 Maxar Technologies Inc.

- 6.4.7 Mitsubishi Heavy Industries

- 6.4.8 Thales

- 6.4.9 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.