Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693956

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693956

Mid-size Satellites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 179 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

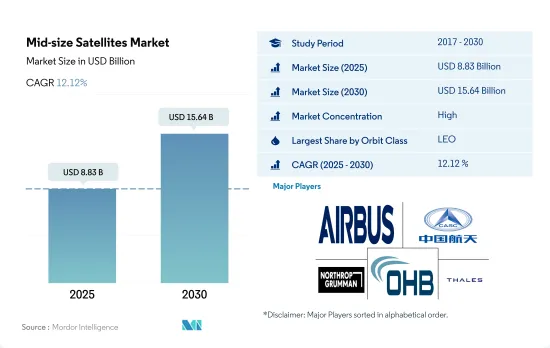

The Mid-size Satellites Market size is estimated at 8.83 billion USD in 2025, and is expected to reach 15.64 billion USD by 2030, growing at a CAGR of 12.12% during the forecast period (2025-2030).

Increased development of small and medium satellites is expected to drive the adoption rate of LEO satellites from 2023 to 2029

- Medium satellites or mid-size satellites weighing 500 to 1,000 kg are being launched in the LEO orbit and are expected to continue the same throughout the forecast period. LEO orbit occupied the majority of the market share of 85.3% in 2017.

- Depending on the type of application or mission, a particular satellite or an entire satellite constellation is launched in various types of orbit. Different satellites manufactured and launched across all the regions have different applications. For instance, during 2017-2022, out of the 167 large satellites launched, 114, 43, 8, and 2 were placed in LEO, MEO, GEO, and elliptical orbits, respectively.

- With respect to the market shares, LEO orbit is expected to lead the market, and it is expected to occupy a share of 84% in 2023 and 83.1% in 2029. The high market share is because of its close proximity and several other advantages triggered by technological developments. GEO orbit is expected to register a share of 9% in 2023, and it is anticipated to occupy a share of 7% in 2029.

- The multi-function capabilities of these satellites, such as the increasing uses of satellites in areas like electronic intelligence, Earth science/meteorology, laser imaging, optical imaging, and meteorology, are expected to drive the demand for the development of these satellites during the forecast period.

- The global mid-size satellite market is expected to grow at a steady pace due to the increasing demand for satellite-based services across various industries, such as telecommunications, government, and defense. North America is the largest market for mid-size satellites, with the United States being the major contributor. The US government is the major customer of mid-size satellites for military and intelligence purposes. The European mid-size satellite market is driven by the increasing demand for satellite-based navigation services, particularly in the automotive and transportation industries. The Asia-Pacific mid-size satellite market is being driven by a growing demand for satellite-based telecommunications and remote sensing services. The mid-size satellite market in the Rest of the World is also experiencing growth due to the increasing demand for satellite-based communications in rural and remote areas.

- The global mid-size satellite market is witnessing several trends, including the development of miniaturized satellite components and more efficient propulsion systems. The miniaturization of satellite components is reducing the cost of manufacturing and launching mid-size satellites. This is expected to increase the demand for mid-size satellites, particularly in developing countries. The market is also driven by the increasing investments by governments and private companies in the space industry. Overall, the market is expected to continue its steady growth in the coming years, driven by increased demand for satellite-based services across various industries and regions. The market is also expected to be fueled by advancements in satellite technology, including the development of miniaturized satellite components.

Global Mid-size Satellites Market Trends

Growing demand for Earth observation, imaging, and connectivity services is expected to surge the research and development expenditure in the mid size satellites category

- Over recent years, there has been a significant increase in the number of mid-size satellite missions launched and in development globally. This is largely due to advances in technology that have made it more affordable and accessible to build and launch these types of satellites. As a result, R&D expenditure in this area has been growing steadily. European countries are recognizing the importance of various investments in the space domain and are increasing their spending in areas such as Earth observation, satellite navigation, connectivity, space research, and innovation to stay competitive and innovative in the global space industry.

- In November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. The European Space Agency (ESA) is requesting its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. Likewise, in September 2022, France announced that it was expecting to increase spending on national and European space programs as the European Space Agency works to secure commitments for its own significant budget increase. The government announced that it planned to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years.

- During 2017-2022, around 320+ satellites were manufactured and launched globally. Overall, the mid-sized satellite market is expected to continue to grow, driven by the growing demand for Earth observation, imaging, and connectivity services.

Mid-size Satellites Industry Overview

The Mid-size Satellites Market is fairly consolidated, with the top five companies occupying 81.92%. The major players in this market are Airbus SE, China Aerospace Science and Technology Corporation (CASC), Northrop Grumman Corporation, OHB SE and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001304

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Global

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 France

- 4.3.7 Germany

- 4.3.8 India

- 4.3.9 Iran

- 4.3.10 Japan

- 4.3.11 New Zealand

- 4.3.12 Russia

- 4.3.13 Singapore

- 4.3.14 South Korea

- 4.3.15 United Arab Emirates

- 4.3.16 United Kingdom

- 4.3.17 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 China Aerospace Science and Technology Corporation (CASC)

- 6.4.3 Indian Space Research Organisation (ISRO)

- 6.4.4 Northrop Grumman Corporation

- 6.4.5 OHB SE

- 6.4.6 ROSCOSMOS

- 6.4.7 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.