PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431729

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431729

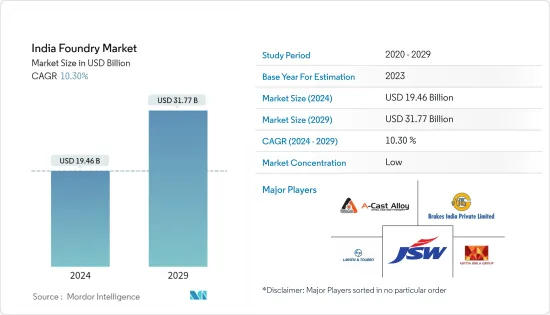

India Foundry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The India Foundry Market size is estimated at USD 19.46 billion in 2024, and is expected to reach USD 31.77 billion by 2029, growing at a CAGR of 10.30% during the forecast period (2024-2029).

During the COVID-19 pandemic in December 2020, more than 400 small foundries in Coimbatore shut their doors due to rising raw material prices. The shutdown affected lakhs of employees working in and with the foundries, as well as in other industries such as pumps, textile machines, automobiles, and other engineering sectors. Moreover, in March 2022, several foundry units in Kolhapur were temporarily closed and declared three to four days of holiday for their employees due to a sharp increase in raw material prices caused by the Russia-Ukraine war.

Key Highlights

- The major foundry clusters in India are located in Batala, Jalandhar, Ludhiana, Agra, Pune, Kolhapur, Sholapur, Rajkot, Mumbai, Ahmedabad, Belgaum, Coimbatore, Chennai, Hyderabad, Howrah, Kolkata, Indore, Faridabad, and Gurgaon. Typically, each foundry cluster is known for catering to some specific end-use markets. For example, the Coimbatore cluster is famous for pump-set castings, the Kolhapur and Belgaum clusters for automotive castings, the Rajkot cluster for diesel engine castings, and the Howrah cluster for sanitary castings. The IIF estimates suggest that there are over 7,000 foundry units in the country, with about 3,000 located in Gujarat. The sector provides direct employment to about five lakh people and indirect employment to 15 lakh people.

- Moreover, the focus on technology upgrades notably drives the growth of the Indian foundry market. For instance, in India, many foundries use cupolas using LAM Coke. However, these are gradually shifting to Induction Melting. There is growing awareness about the environment, and many foundries are switching over to induction furnaces, while some units in Agra are changing over to cokeless cupolas. However, the major challenges faced in India include a lack of skilled manpower, adequate power supply at competitive rates, availability due to mining and environmental issues, and the short-term slowdown in demand, which may hinder medium and longer-term investments.

India Foundry Market Trends

Growing Automobile Sector is Driving the Foundry Market in India

- The Indian foundry market is primarily driven by rapid industrialization and urbanization, which have increased the utilization of the metal casting process across the country. The surge in automobile manufacturing is also a significant factor boosting market growth.

- India stood as one of the world's leading countries in vehicle production. In the financial year 2023, the total vehicle production in India reached around 25.93 million units, marking an increase from the previous year, as reported by the Society of Indian Automobile Manufacturers (SIAM). In 2020, the production value experienced a contraction primarily due to the introduction of the new Bharat Stage VI (BS-VI) emissions standards on April 1, 2020, and an overall scaled-down production due to the lower stock of the old BS-IV vehicles. The coronavirus pandemic in India further exacerbated the subsequent decline in production.

- According to the Society of Indian Automobile Manufacturers (SIAM), in 2022, India produced approximately 22.93 million vehicles, encompassing commercial vehicles, passenger cars, tricycles, and two-wheelers. The automotive industry experienced a 13.63% growth in sales in 2022 compared to 2021. Specifically, motorcycle sales increased by 4.7% in 2022 over the previous year, according to SIAM.

- Another significant driver for the Indian foundry market's growth is the increasing government expenditure on infrastructure expansion, stimulating demand for various machinery and equipment such as pumps, cranes, fans, motors, and conveyor belts. This surge in demand, in turn, amplifies the need for metal castings.

- Consequently, there is an escalated demand for auto parts necessary for automobile manufacturing. To address this growing demand for metal castings in India, foundries are investing in new technology and equipment. The anticipated benefits from these investments include lower power consumption, improved production efficiency, higher utilization rates, and increased profit margins for Indian foundries. Therefore, the burgeoning automobile industry is expected to drive the growth of the Indian foundry market during the forecast period.

Increasing Government Support for the Indian Foundry market

- The Indian Foundry Industry data indicates approximately 500,000 direct and 15,00,00 indirect employees, making it a significant source of employment, primarily for socially and economically disadvantaged sections. Forecasts suggest the potential creation of an additional 2 million jobs over the next decade due to the industry's labor-intensive nature.

- According to the 56th World Casting Census by Modern Castings USA (January 2023), China, India, and the US lead global casting production, with production ramping up after a COVID-induced two-year hiatus. China reported 54.05 million tonnes of casting, followed by India as the world's second-largest producer, with 12.49 million tonnes.

- India's foundries are actively upgrading their facilities and technologies to enhance productivity and expand capacity, responding to escalating demand. A majority of these foundries fall under the MSME sector, which has demonstrated consistent growth. The Ministry of Micro, Small and Medium Enterprises (India) and the India Brand Equity Foundation reported nearly 13.8 million micro-enterprises, constituting 96 percent of the MSME sector. Small and medium enterprises accounted for three and 0.28 percent, respectively, totaling more than 14 million registered MSMEs.

- In the second financial year of 2023, over two trillion INR (USD 24 billion) was disbursed in the MSME segment in India, as reported by SIDBI. Reinforced implementation of initiatives like the Public Procurement Policy, Pradhan Mantri MUDRA Yojana, Make in India, Startup India, and Skill India are catalysts fostering the growth of the MSME sector. This surge in government support is expected to further propel the foundry market in the foreseeable future.

India Foundry Industry Overview

The report covers major players operating in the India Foundry Market. The market is highly fragmented and competitive, with large companies claiming significant market share.

Some of the strong players in the country include A Cast Foundry, Aditya Birla Management Corp. Pvt. Ltd., JSW STEEL Ltd., Larsen and Toubro Ltd., Brakes India Pvt. Ltd., Ashok Iron Works Pvt. Ltd., Menon and Menod Ltd., Nelcast Ltd., Tata Sons Pvt. Ltd., CALMET, Cooper Corp. Pvt. Ltd., DCM Ltd., Electrosteel Castings Ltd., Fortune Foundries Pvt. Ltd., Gujarat Metal Cast Industries Pvt. Ltd., etc.,

Major players in the market are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to remain competitive in the market. For instance, in June 2022, Brakes India and Volvo Group ventured into producing green iron castings at Brakes India's foundries to reduce their carbon footprint.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Market Definition

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Focus on Technology Upgrades

- 4.2.1.2 Formation of Foundry Clusters

- 4.2.2 Restraints

- 4.2.2.1 Stringent Government Regulations

- 4.2.2.2 Lack of Highly Skilled Manpower

- 4.2.3 Oppurtunities

- 4.2.3.1 Increasing focus on Sustainability

- 4.2.3.2 Growing Government Expenditure

- 4.2.1 Drivers

- 4.3 Technologies Employed in Foundry Industry

- 4.4 Potential foundry Clusters in India

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Industry Attractiveness- Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By End-user

- 5.1.1 Automotive

- 5.1.2 Electrical and Construction

- 5.1.3 Industrial Machinery

- 5.1.4 Other End-Users

- 5.2 By Type

- 5.2.1 Gray Iron Casting

- 5.2.2 Non-ferrous Casting

- 5.2.3 Ductile Iron Casting

- 5.2.4 Steel Casting

- 5.2.5 Malleable Casting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 A Cast Foundry

- 6.2.2 Aditya Birla Management Corp. Pvt. Ltd

- 6.2.3 Brakes India Pvt. Ltd.

- 6.2.4 CALMET

- 6.2.5 JSW STEEL Ltd

- 6.2.6 Larsen and Toubro Ltd.

- 6.2.7 Ashok Iron Works Pvt. Ltd.

- 6.2.8 Gujarat Metal Cast Industries Pvt. Ltd.

- 6.2.9 Electrosteel Castings Ltd.

- 6.2.10 Menon and Menod Ltd.*

7 FUTURE OF THE MARKET

8 APPENDIX