PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431739

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431739

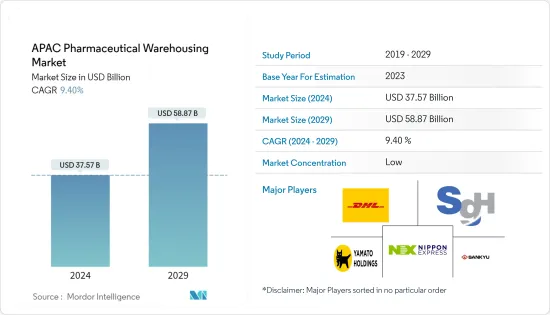

APAC Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The APAC Pharmaceutical Warehousing Market size is estimated at USD 37.57 billion in 2024, and is expected to reach USD 58.87 billion by 2029, growing at a CAGR of 9.40% during the forecast period (2024-2029).

Key Highlights

- The market is seeing the emergence of new technologies such as the Internet of Things (IoT), blockchain, and data analytics to improve visibility, traceability, and overall supply chain performance.

- The pharmaceutical industry has moved into a new phase of rapid integration. As a result of the overall progress of epidemic prevention and control and progressive liberalization, overall pharmaceutical supply chain development has started to recover.

- As we look ahead to 2023, the 100-year transformation and the 100-year pandemic are inextricably linked. Domestic development faces the triple challenge of declining demand, supply shocks, and weakening expectations.

- In China, Total sales of all three major end-of-life drugs increased slightly in 2022, by approximately 1.1%. Public hospitals continue to dominate the market, although their overall market share is decreasing due to the effects of national medical reform policies.

- In China, Public hospitals account for approximately 61.8 percent of drug sales in 2022, while retail pharmacies account for approximately 29.0 percent, and medical and drug sales account for approximately 9.2 percent. Drug consumption started to shift away from the hospital and toward the outside market, with a clear trend of prescription outflow.

- The increase in demand is driven by the increasing cost of healthcare in the region, the increasing prevalence of generic substitutes, and the prevalence of chronic diseases like diabetes, cancer, and cardiovascular diseases like hypertension, all of which result in high treatment costs.

- Cold chain expansion was expected to see a surge in demand as cold chain manufacturers shifted their focus from production to storage to extend the shelf life of their products due to COVID-19's impact on the global healthcare cold chain supply chain, as well as the pandemic's restrictions on commerce.

APAC Pharmaceutical Warehousing Market Trends

Increase in Cold Storage Warehouses is driving the market

- COVID-19 changed the way the supply chain operates. More advanced digital technologies are being adopted to enhance operational performance and address health issues. The evolving logistics industry scenario, the need for significant cost reduction, and optimal inventory management are expected to drive the growth of healthcare cold chain logistics in the Asia-Pacific region.

- In Southeast Asia, Japanese logistics companies are leveraging their decades of experience to build state-of-the-art warehouses equipped with features such as temperature controls to meet the ever-evolving needs of local customers. With rising incomes in Asia, customers expect faster delivery of their online orders. Consequently, warehouses must be automated to save time and equipped with stringent temperature controls to ensure freshness.

- Thailand boasts the most advanced warehouses in Asia. With a population of more than 269 million people, Indonesia holds considerable potential but has lagged in logistics development, partly due to the logistical challenges posed by the country's many islands. Demand from domestically oriented businesses is on the rise.

- Companies are investing millions of dollars in developing efficient, effective, and dependable cold chain processes because cold chain security remains a weak point in the system. Furthermore, the number of cold warehouses in Asia-Pacific is increasing due to rising demands for food and pharmaceutical products in the region. Consequently, an increase in cold warehouses is expected to expand the Asia-Pacific cold chain logistics market.

India will lead the warehouse space creation in the region

- In 2023, India is projected to account for more than one-third of all incremental warehousing space additions in the Asia Pacific. The country is expected to witness the most significant growth in warehouse and logistics supply within the region, projecting a 29 million square foot increase, constituting over one-third of the total projected 85 million square feet of logistics space in the region.

- Not only Bengaluru but also Delhi-NCR and Mumbai will lead the rental growth list in 2023. Mumbai is anticipated to experience a 4-6% increase in warehousing rentals, while Delhi-NCR is poised for the most substantial surge, growing between 5-7% year-on-year. Australia is expected to lead with a 12% increase in rentals.

- India's pharmaceutical industry is rapidly expanding and gaining prominence in the global pharma market. The Indian government has implemented various policies and schemes to promote cold storage in the country. These initiatives include allowing 100% Foreign Direct Investment (FDI), providing a 100% exemption for profit in food processing units for the first five years and 25% to 30% for the subsequent five years, along with a range of subsidies.

APAC Pharmaceutical Warehousing Industry Overview

The pharmaceutical warehousing market in APAC is dynamic and competitive. The pharmaceutical industry in APAC is expanding, and there is a growing need for efficient warehousing and distribution solutions. There are many international and local players operating in the market. From an APAC perspective, Malaysia is emerging as a hub for multinational pharmaceutical companies. Malaysia's low wages, strategic proximity to China, improved infrastructure, and pro-business policy make it an attractive market for both operating and indirect tax purposes. Vietnam, on the other hand, is an emerging hub for pharmaceutical companies. It remains to be seen how developments in Asia unfold. Pharma companies would do well to keep an eye on the situation. As pharmaceutical legislation changes, companies that can quickly adjust to changing compliance requirements are likely to gain a competitive advantage in this expanding market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview (Current Market Scenario of Market and Economy)

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends

- 4.4 Impact of Covid-19 on the market

- 4.5 Market Dynamics

- 4.5.1 Market Drivers

- 4.5.1.1 Rapidly Expanding Pharmaceutical Industry

- 4.5.1.2 Government Regulations and Intiatives

- 4.5.2 Market Restraints/ Challenges

- 4.5.2.1 Supply Chain Disruptions

- 4.5.2.2 Temperature Controlled and Cold Chain Management

- 4.5.3 Market Opportunities

- 4.5.3.1 Technological Innovations

- 4.5.1 Market Drivers

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Powers of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 BY Type

- 5.1.1 Cold Chain Warehouse

- 5.1.2 Non-Cold Chain Warehouse

- 5.2 By Application

- 5.2.1 Pharmaceutical Factory

- 5.2.2 Pharmacy

- 5.2.3 Hospital

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Vietnam

- 5.3.1.8 Thailand

- 5.3.1.9 Rest-of-APAC

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

7 Overview (Market Concentration and Major Players)

8 Company Profiles

- 8.1 Nippon Express

- 8.2 Sankyu

- 8.3 DHL

- 8.4 DSV

- 8.5 Goke Hengtai (Beijing) Medical Technology Co., Ltd.

- 8.6 SG Holdings

- 8.7 Yamato Holdings

- 8.8 Mitsui - Soko Group

- 8.9 Sinopharm Logistics

- 8.10 Yunda Holding

- 8.11 CJ Rokin Logistics

- 8.12 SF Express

- 8.13 JD Logistics

- 8.14 Kerry Logistics*

9 *List Not Exhaustive

10 MARKET OPPORTUNITIES AND FUTURE OF THE MARKET

11 APPENDIX

12 DISCLAIMER