PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639517

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639517

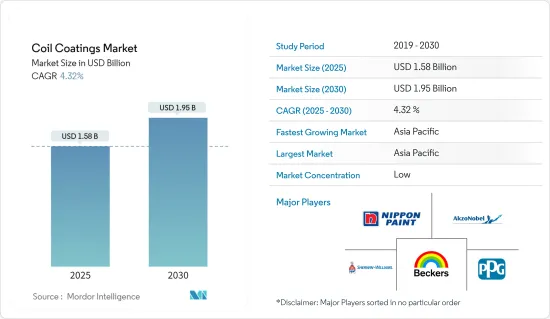

Coil Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Coil Coatings Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 1.95 billion by 2030, at a CAGR of 4.32% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. The pandemic jeopardized building construction and engineering projects worldwide in numerous ways, and many projects were closed or halted, decelerating the growth of the coil coatings market during the pandemic crisis. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, rising demand from the building and construction industry and growing environmental influences, and advancing technology are the major factors driving the market studied.

- Conversely, increasing demand for lightweight materials in the automobile industry is expected to hinder the studied market's growth.

- However, increasing demand for fluoropolymer coatings for architectural applications will likely act as an opportunity.

- Asia-Pacific dominated the market in terms of consumption due to the rise in the production and export of pre-coated metal sheets in the region due to the high production of finished steel and the high manufacturing of end-user products.

Coil Coatings Market Trends

Rising Demand from the Building and Construction Industry

- The building and construction industry is by far the largest consumer of coil coatings. The main resins used extensively in construction are polyester resin, silicone-modified polyester, polyvinylidene fluorides (PVDF), or fluoropolymer. With the rising number of building codes that promote energy-efficient structures, home builders and consumers are gradually moving toward building strategies that deliver performance and energy savings in the long run.

- The rising demand from the construction industry is a key factor driving the coil coatings market. Some of the large ongoing building construction projects worldwide include the Magnolia Mixed-Use Complex project worth USD 1 billion in Texas, which is expected to be completed in Q1 2025. The Minamikoiwa 6-Chome District Type One Urban Redevelopment project in Tokyo, Japan, is another project expected to be completed in 2026. Thus, such construction projects are estimated to use coil products for roofing, steel doors, aluminum panels, rubber, metal lamination bonding, renovation work, and others.

- Furthermore, coil coatings are also widely used for interior and exterior construction applications due to their malleability. Home builders and consumers increasingly shift towards building techniques that impart performance and long-term energy savings. Hence, they are focusing on developing energy-efficient structures.

- Coil coatings provide infrared reflective pigment technology that helps in lowering the indoor temperature of the building. This technique reduces the energy consumed for cooling, making coil coatings energy efficient and the preferred choice for coil products used in building and construction work. It is also utilized to construct gutters and downspouts for waterproof installations.

- The construction industry in North America is growing steadily due to the improving commercial real estate sector and increased federal and state investment in public construction and institutional buildings. Some of North America's major building construction projects include the East River Mixed-Use Development project worth USD 2.5 billion. The project aims to provide better residential and office facilities in Texas, which is expected to be completed in 2040. Therefore, increasing building and construction industry investments are expected to create an upside for coil coatings.

- The major Western European countries, including France, Germany, the United Kingdom, and Italy, are actively contributing to the coil coatings market. With growing building construction activities in the region, the demand for coil coatings increased significantly. For instance, according to Trading Economics, construction output in France increased by 3.1% in December 2022 compared to July 2022.

- Moreover, due to its high-end aesthetics and long-lasting value, coil coatings are used in the building and construction industry in ceiling grids, doors, roofing and siding, windows, etc. Some of the ongoing construction projects include the Eight Office Tower project worth USD 476 million, which involves the construction of a 25-story office tower in Bellevue, Washington, United States. It is expected to be completed in 2024. The Hamamatsucho Shibaura 1 Chome Redevelopment Project, worth USD 3.17 billion in Tokyo, Japan, is another ongoing project.

- The project involves the construction of two buildings and is expected to be finished by 2030. The Elizabeth Quay Lot V and Lot VI Mixed-Use Complex construction project worth USD 841 million in Australia is yet another project likely to be completed in 2025. These projects are expected to increase the demand for pre-coated metals in the construction of residential and commercial buildings in the coming years.

- Due to all such factors, the building and construction industry's coil coatings market is expected to grow steadily during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market share. Due to their high-end aesthetics and long-lasting value, coil coatings are used in the building and construction industry in ceiling grids, doors, roofing and siding, windows, etc.

- The Asia-Pacific coil coatings market is anticipated to grow significantly during the forecast period, with China leading the market owing to expanding construction and rapid industrial development. The growing building construction and renovation activities in the region are expected to surge the consumption of coil coatings.

- For instance, some of the ongoing building construction projects in the Asia-Pacific include the Hamamatsucho Shibaura 1 Chome Redevelopment project worth USD 3.17 billion, expected to be completed in 2030 in Tokyo, Japan. Another such project is the Wuhan Fosun Bund Center T1 project, which involves the construction of the Fosun Bund Center T1 in Wuhan, China. Therefore, increasing building construction projects are expected to drive the growth of coil coatings in the region.

- Furthermore, the growing demand for transport vehicles is driving the coil coatings market. In 2023, India's automotive sector is predicted to be the strongest in the Asia-Pacific region, owing to strong demand and consumers' preference for personal vehicles over public transportation. For instance, according to OICA, in 2022, automobile production in the country amounted to 5,456,857 units, which showed an increase of 24% compared to 2020. Therefore, the region's coil coatings industry will likely expand due to the rise in overall automobile manufacturing.

- All such factors are expected to increase the demand for coil coatings in the region.

Coil Coatings Industry Overview

The coil coatings market is fragmented in nature. The major players in this market (not in a particular order) include Akzo Nobel N.V., Beckers Group, PPG Industries, Inc., The Sherwin-Williams Company, and Nippon Paint Holdings Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Building and Construction Industry

- 4.1.2 Growing Environmental Influences and Advancing Technology

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Demand for Lightweight Materials in Automotive Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Polyester

- 5.1.2 Polyvinylidene Fluorides (PVDF)

- 5.1.3 Polyurethane(PU)

- 5.1.4 Plastisols

- 5.1.5 Other Resin Types

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Industrial and Domestic Appliances

- 5.2.3 Transportation

- 5.2.4 Furniture

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Coil Coaters

- 6.4.1.1 ArcelorMittal

- 6.4.1.2 Arconic

- 6.4.1.3 BDM Coil Coaters

- 6.4.1.4 CENTRIA

- 6.4.1.5 Chemcoaters

- 6.4.1.6 Dura Coat Products

- 6.4.1.7 Goldin Metals Inc.

- 6.4.1.8 Jupiter Aluminum Corporation

- 6.4.1.9 Norsk Hydro ASA

- 6.4.1.10 Novelis

- 6.4.1.11 Ralco Steels

- 6.4.1.12 Rautaruukki Corporation

- 6.4.1.13 Salzgitter Flachstahl GmbH

- 6.4.1.14 Tata Steel

- 6.4.1.15 Tekno Kroma

- 6.4.1.16 thyssenkrupp AG

- 6.4.1.17 UNICOIL

- 6.4.1.18 United States Steel Corporation

- 6.4.2 Paint Suppliers

- 6.4.2.1 Akzo Nobel N.V.

- 6.4.2.2 Axalta Coatings System LLC

- 6.4.2.3 Beckers Group

- 6.4.2.4 Brillux GmbH & Co. KG

- 6.4.2.5 Hempel A/S

- 6.4.2.6 Kansai Paint Co.,Ltd.

- 6.4.2.7 Nippon Paint Holdings Co., Ltd

- 6.4.2.8 NOROO Coil Coatings Co., Ltd.

- 6.4.2.9 PPG Industries, Inc.

- 6.4.2.10 The Sherwin-Williams Company

- 6.4.2.11 Yung Chi Paint & Varnish Mfg Co. Ltd

- 6.4.3 Pretreatment, Resins, Pigments, Equipment

- 6.4.3.1 Arkema

- 6.4.3.2 Bayer AG

- 6.4.3.3 Covestro AG

- 6.4.3.4 Evonik Industries AG

- 6.4.3.5 Henkel AG & Co. KgaA

- 6.4.3.6 Solvay

- 6.4.3.7 Wacker Chemie AG

- 6.4.1 Coil Coaters

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Fluoropolymer Coatings for Architectural Applications

- 7.2 Other Opportunities